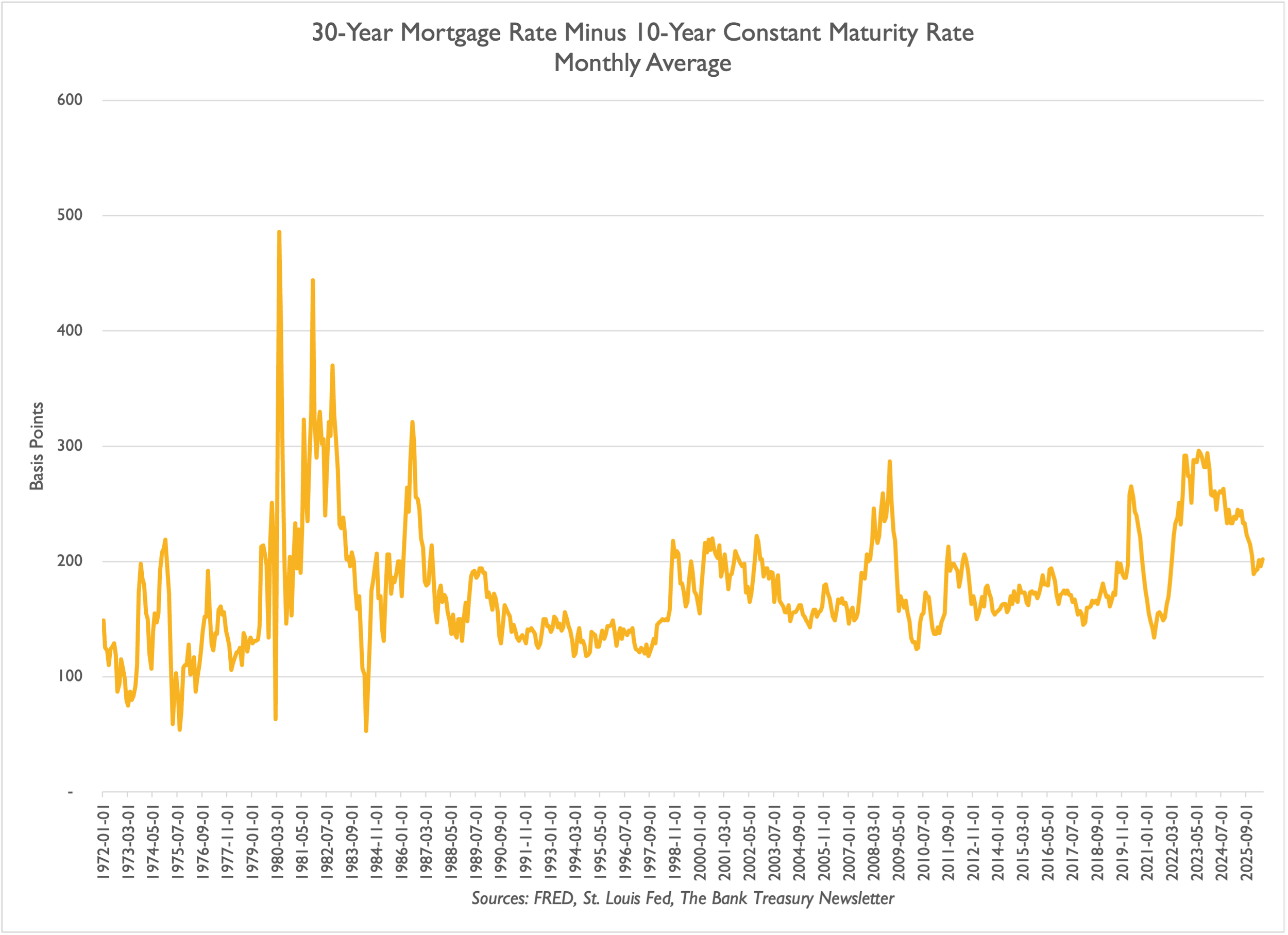

Research from the Richmond Fed shows that the spread between a residential mortgage and the 10-year Treasury is influenced by how lenders view the prepayment option, anticipated interest rates, and the shape of the yield curve. When the yield curve inverts and recession fears grow, the difference between a 30-year mortgage and the 10-year Treasury widens, as lenders expect rates to drop and borrowers to prepay, requiring higher compensation for prepayment risk. Currently, with a positively sloped yield curve and market expectations of rising long-term rates, borrowers are less likely to prepay, reducing the value of the prepayment option, as shown in Slide 1.

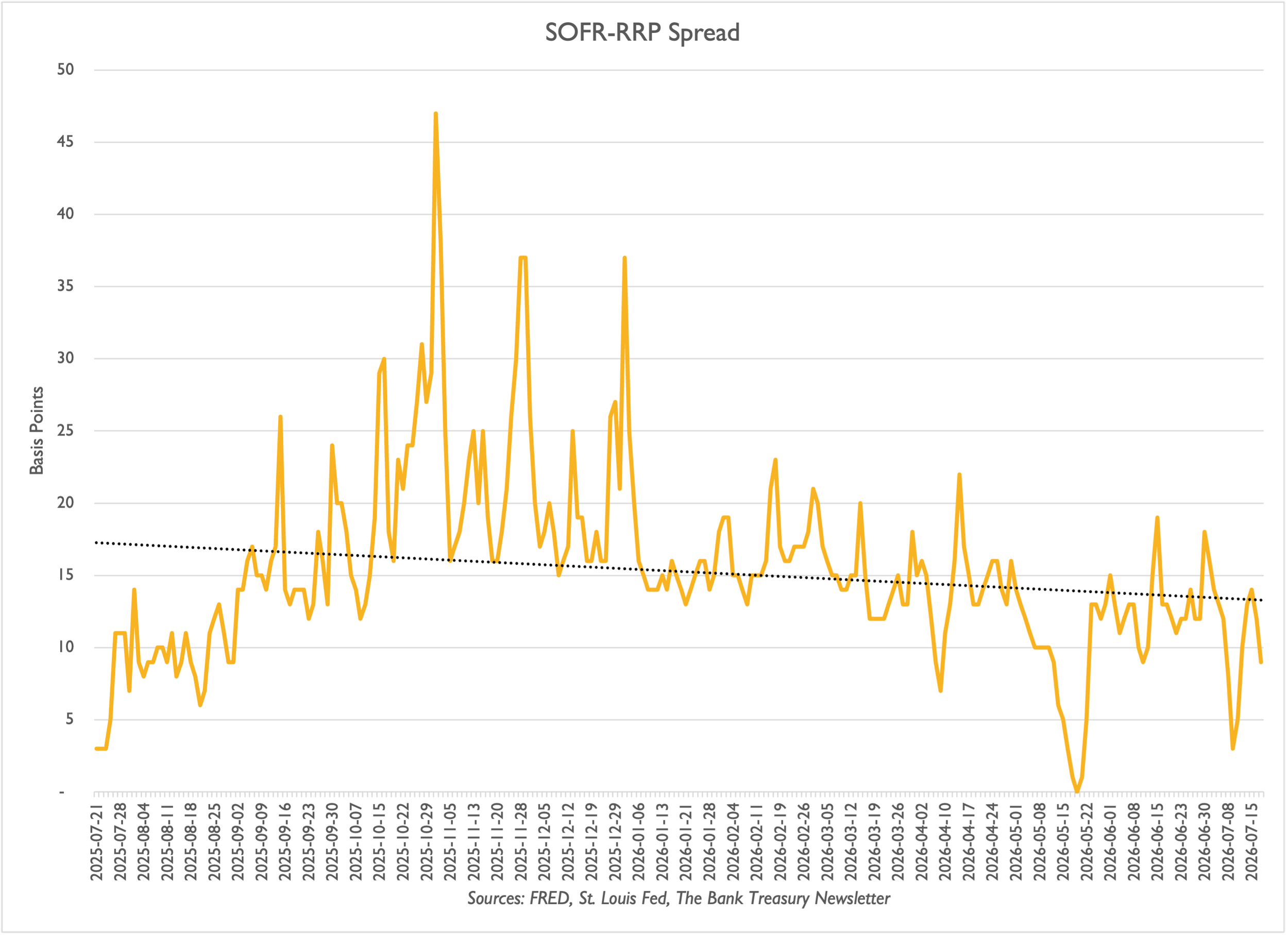

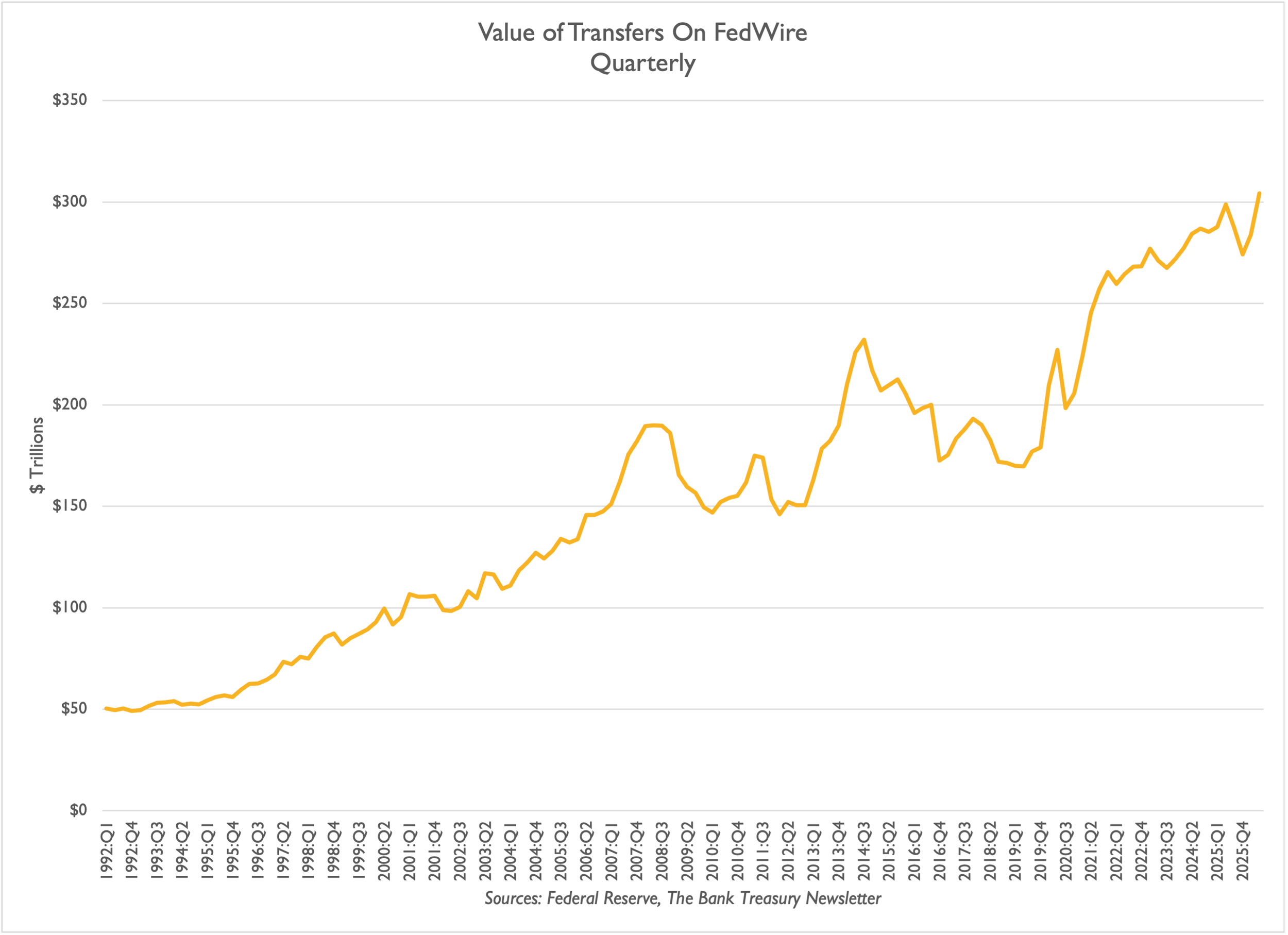

The spread on Slide 2 between the Secured Overnight Financing Rate (SOFR) and the rate paid by the Fed to cash providers using its Reverse Repo Facility (which uses securities in the System Open Market Account as collateral and receives cash) reflects the level of reserve deposits in the system. This is because the repo market operates over FedWire using these reserves. The narrowing spread since the start of the year shows the Fed’s effective management of reserves after ending Quantitative Tightening, mainly through buying Treasury Bills as part of its Reserve Management Program (RMP). A year ago, the Fed held just under $200 billion in T-Bills, and now that amount has increased to $550 billion. Although Chairman Warsh is exploring options to shrink the Fed’s balance sheet, any plan would likely involve reducing reserve deposits. Transfers over FedWire, which depend on reserves, continue to increase (Slide 3).

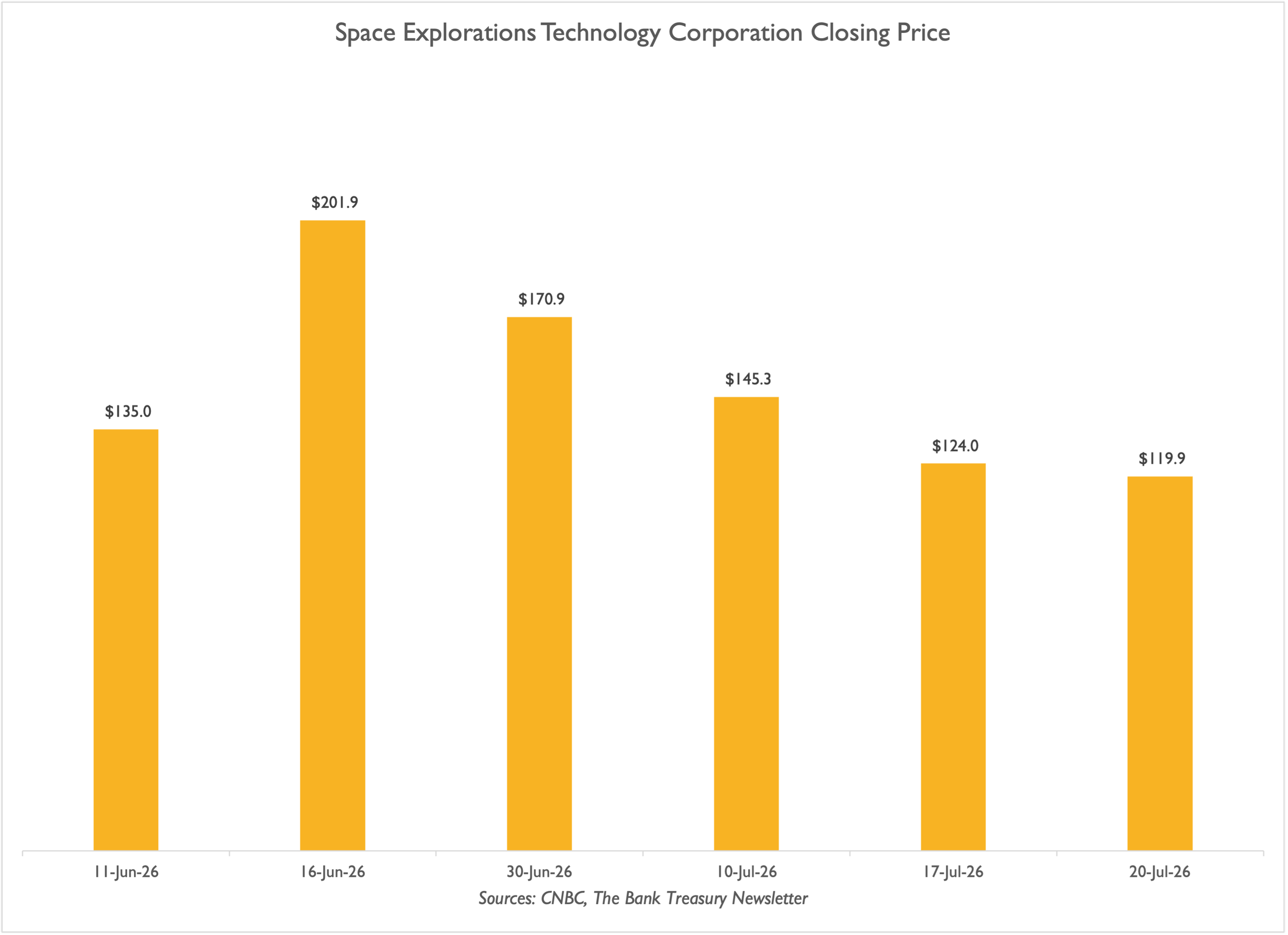

The AI boom reflects broader optimism in financial markets about the economy, which is driving up stock prices and attracting new offerings. The market's excitement was evident when SpaceX launched its IPO last month: the stock rose from $135 to over $200 shortly after but has fallen below $135 again (Slide 4). SpaceX also announced it will release its first earnings report on August 4.

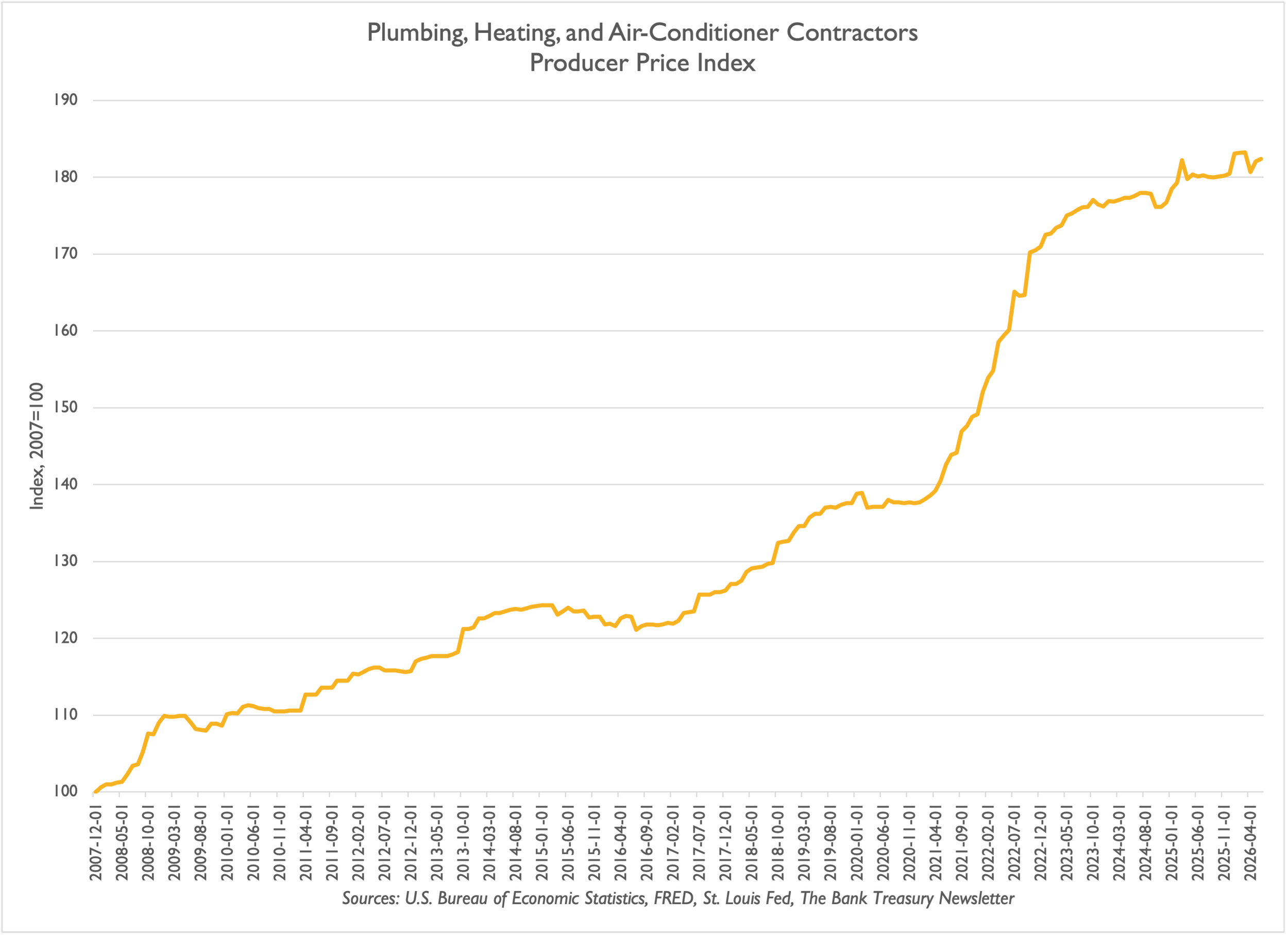

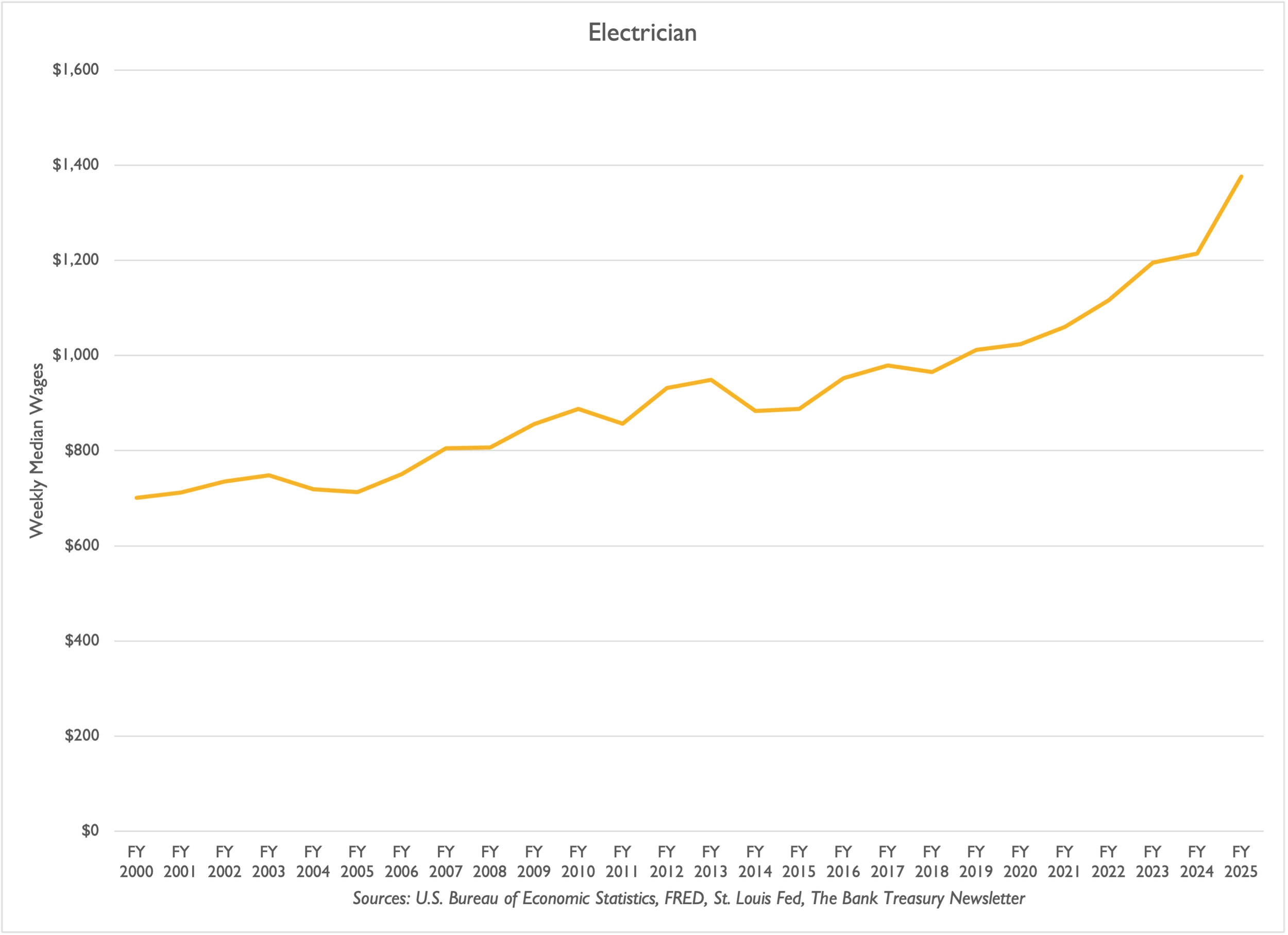

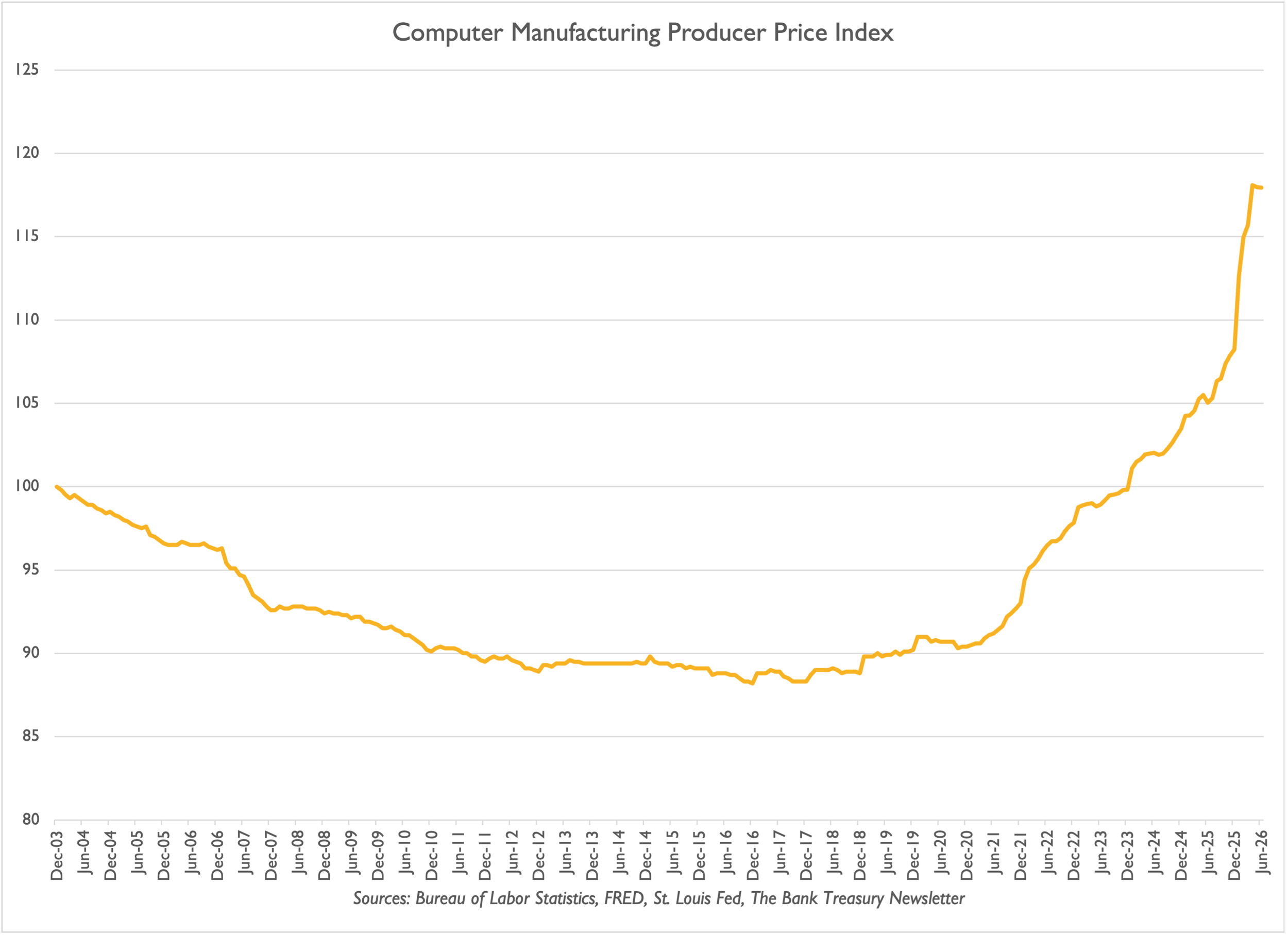

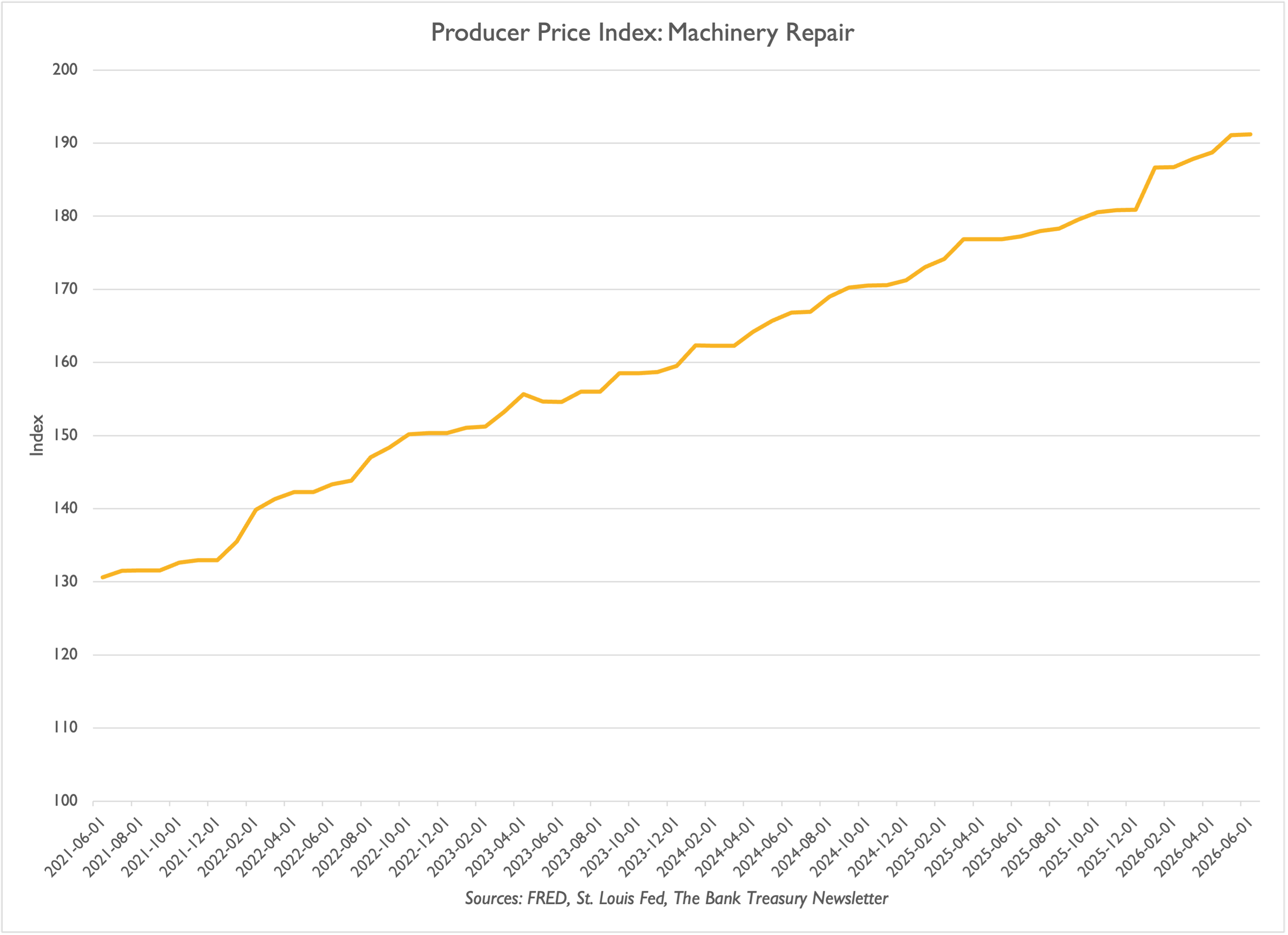

Although economists are concerned about AI's potential impact on employment, blue-collar workers such as plumbers (Slide 5) and electricians (Slide 6) are experiencing increased demand and earning higher wages. The rising demand for computers, driven by data centers (Slide 7), has also boosted the job security of computer repair specialists (Slide 8).

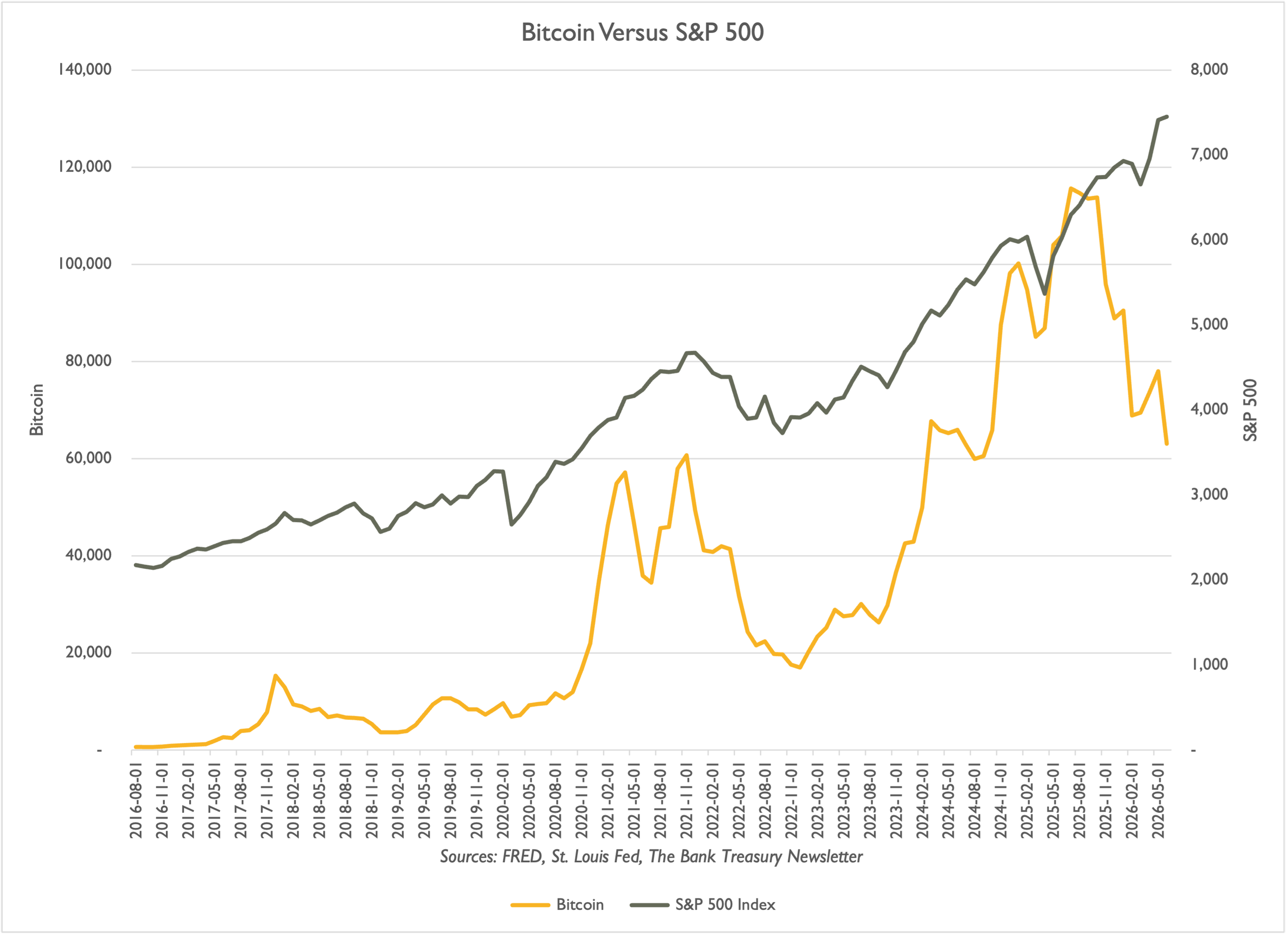

While Congress and bank supervisors work to support the cryptocurrency market, investors seem to be losing enthusiasm for Bitcoin (Slide 9). Meanwhile, bank treasurers show more optimism about developing tokenized deposits than about providing stablecoins to their customers for payments.

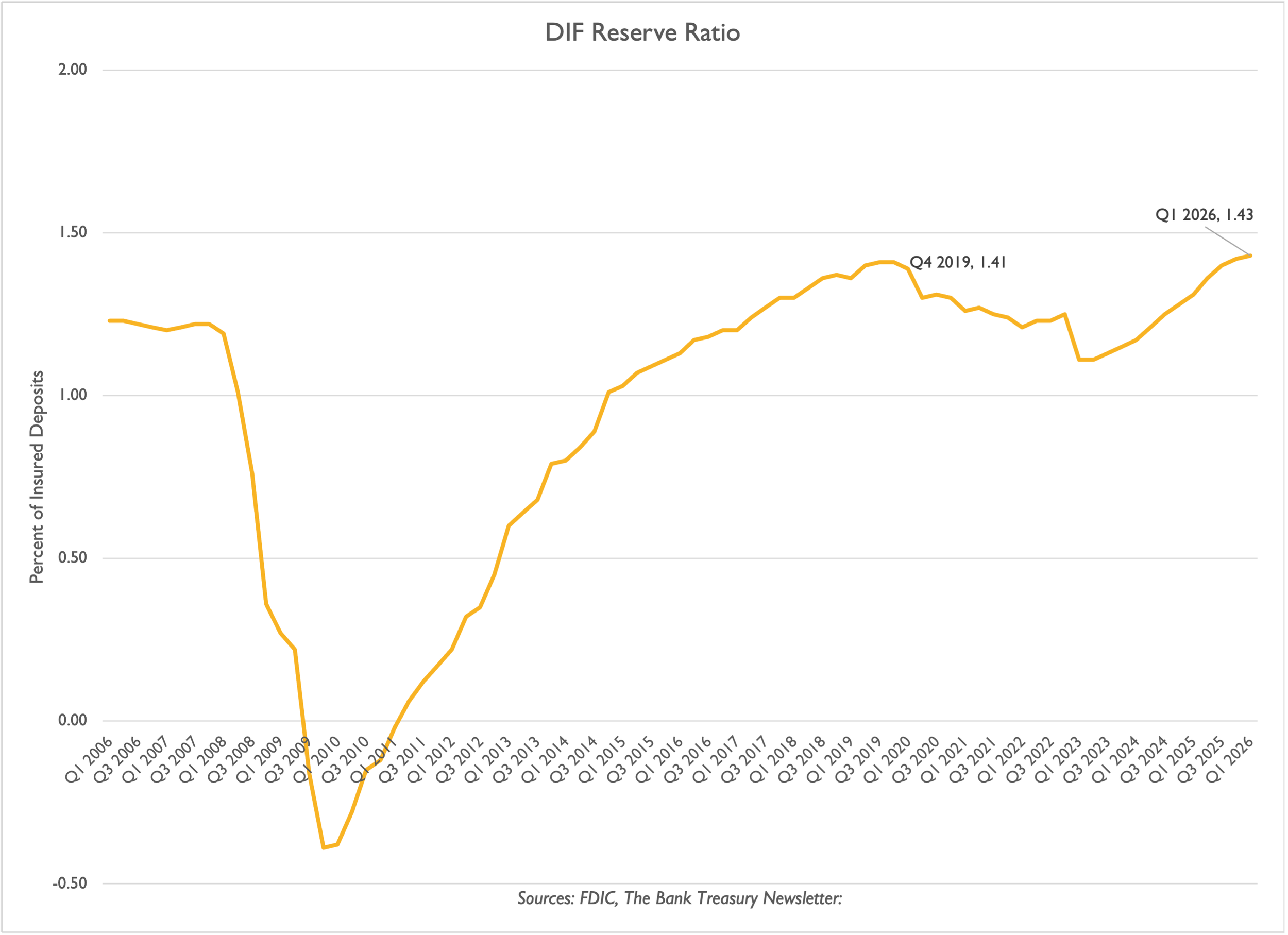

This month, the Deposit Insurance Fund (DIF) reached a record 1.43% of insured deposits, prompting the Federal Deposit Insurance Corporation (FDIC) to announce a reduction in insurance assessment costs. The agency is increasing the threshold for a bank to be classified as “Large” from $10 billion to $30 billion. Additionally, it is lowering the initial base assessments by 2 basis points for banks with total assets under $30 billion (“Small” banks) and by 1 basis point for “Large” and “Complex” banks. These initial assessments can be as low as 5 basis points for “Small” banks that are rated as “satisfactory” or “strong” by bank examiners.

Mortgage Prepayment Option Value Declines

RMP Keeps SOFR-RRP Spread Positive

Payments Put A Floor Under Supply Of Reserves

Irrational Exuberance Fades On SpaceX

HVAC Specialists in Demand

Electricians in Demand

Computer Prices Soar

Computer Repair Costs Soar, Too

Investors Still Backing Away From Crypto

Record DIF Leads FDIC To Cut Assessment Rates

The Bank Treasury Newsletter is an independent publication that welcomes comments, suggestions, and constructive criticisms from our readers in lieu of payment. Please refer this letter to members of your staff or your peers who would benefit from receiving it, and if you haven’t yet, subscribe here.

Copyright 2026, The Bank Treasury Newsletter, All Rights Reserved.

Ethan M. Heisler, CFA

Editor-in-Chief