BANK TREASURERS WORRY A LOT

The bank supervisory agencies are undergoing a significant reorganization involving massive layoffs across the Fed, Office of the Comptroller of the Currency (OCC), the Federal Deposit Insurance Corporation (FDIC), the Securities and Exchange Commission, and the U.S. Treasury, involving bank examiners and economists. Chair Powell, for example, said that the Fed plans to reduce its 21,000 workforce by 10% in the next couple of years, while the OCC announced last month that it was consolidating its bank supervisory groups, merging supervision of small, medium, and large banks into one team as opposed to separate teams covering small and medium size banks separately from large banks.

The FDIC also announced plans to pare back its workforce even though a report it published last March identified understaffing in its examination force as a mission-critical challenge. Bank management expects a significant rollback of bank regulations enacted or proposed by the end of the year. Yet, ironically, there is a chance that bank supervisors will not even have the experienced staff necessary to redraft proposals and see them through to final drafting.

Interest rate volatility is up. For example, the implied volatility on 10-year swap spreads spiked this year to its highest level in over a year. Despite market volatility, rates and the yield curve are roughly where they have been all year to date, with the 10-year Treasury holding at 4.5% and the Fed holding the Fed funds rate between 4.25% and 4.50%. Fed officials downplay the prospect of multiple rate cuts this year, but consensus still seems strong that it would cut them at least once before its December meeting. The CME Fed Monitor still pegs chances of at least two rate cuts of 25 basis points each as likely.

Bank treasurers continue to sit on significant reserve deposits, which have held stable at $3.3 trillion since the Fed began Quantitative Tightening (QT) three years ago. They also hold shorter-duration assets in their bond portfolios than they might have held before the regional bank failures two years ago. Even though they also model their deposit funding much shorter than they would have two years ago, they are still concerned about their exposure to a sudden downrate scenario and are looking for ways to protect from it.

Interest rate hedging activity is increasing, as call report data from Q1 2025 show that the notional principal of interest rate derivative contracts not held for trading grew to $5.4 trillion at the end of the quarter, up from $4.9 trillion at the end of 2024. According to Eris Innovations, one of the newsletter’s corporate sponsors, there was a surge in open interest in Eris SOFR Swap futures contracts this month, mostly replicating a receive-fixed interest rate swap at a fraction of the cost of a swap and without the hassle of an ISDA agreement.

The general takeaway from Q1 2025 bank results is that net interest margins (NIM) continued to improve. FFIEC data shows that the NIM for the national bank average widened from 3.35% in Q1 2024 to 3.54% in Q1 2025. Deposit costs have also stabilized, and bank treasurers have not seen significant changes in the mix between interest and noninterest-bearing deposits since last summer. The ratio of demand deposits to total deposits based on the national FFIEC average equaled 21% in Q1 2025, which has been stable since Q1 2024, after peaking in Q4 2022 at 23%.

Meanwhile, loan growth picked up last month, according to the latest H.8 data, especially in the commercial and industrial loan categories, most likely reflecting opportunistic business borrowing in the early days after Liberation Day when the 10-year Treasury yield briefly dipped below 4%. Bank lending to nonbank lenders continues to increase, reaching $1.2 trillion this month. Branches and agencies of foreign banks account for a growing percentage of total loans in the system, with 9% of total loans and a quarter of the loans made to nonbank financial institutions.

However, the general message bank management continues to deliver to the analyst community is that borrowers are generally conservative about drawing on credit lines and are waiting for more economic clarity. In its April 2025 Senior Loan Officer Opinion Survey, the Fed reported that banks tightened credit underwriting standards and that the demand for credit weakened. The public also remains cautious, which is not only reflected in the surging price of gold this year as the public turns to precious metals for security, but also in the fact that currency in circulation is growing again this year, reaching $2.4 trillion this month

The Bank Treasury Newsletter

Dear Bank Treasury Subscribers,

Bank treasurers worry a lot. It’s a condition that comes with the job and the territory. It might even be wired somehow into their seat. Some of our bank treasury subscribers even blame their chairs for their worries, claiming their chairs cause them to break out into “the worries,” much like hives, every time they sit in them. They worry so much that every morning, they come to work prepared with a long list of worries that kept them up the night before, worrying that they do not already have enough to worry about during the day.

They are worryworts. They worry about the economy (of course), worry about the direction of interest rates (naturally), worry about bank regulations and accounting (no doubt), and they worry about deposit pricing, loan pricing, and maintaining stable NIMs and net interest income because that literally is their job. And they worry about uncertainty and market volatility because these conditions make their job harder to run their bank’s balance sheet, analyze and try to navigate across multiple-risk paths, and, most importantly, not screw up.

Rule number one in the bank treasury business: do not screw up. You don’t want to do that. However, when the economic data is regularly a surprise, beating or missing expectations, and when the price of assets moves around so much that it is hard to fix and trade a value, the financial markets get challenging to navigate, the banking environment worsens, and mistakes happen.

And decisions cannot always wait for more data and clarity. Sometimes, sitting in the bunker, staying indoors, and waiting out the storm is not enough. Sometimes, cash needs to go somewhere today, and there are no great choices, just decisions with uncertain outcomes that cannot wait anymore.

Making decisions is why bank treasurers have a desk chair in the first place. They can use artificial intelligence software to help them make those decisions. Straterix, one of the newsletter’s corporate sponsors, has machine learning software that they can use to calculate risk probabilities over thousands of different scenarios in a blink, all uniquely chosen for each bank’s unique risk exposure. But even with that new technology, bank treasurers are responsible, not the machine. It is their call to make.

Decisions, Decisions

Bank treasurers are the ones who need to decide whether to reinvest cash flows from the bond portfolio into their overnight reserve account at the Fed or reinvest proceeds back into bonds with the same or shorter maturity. They get paid to decide whether to take the risk that, with their excess deposits invested overnight, the Fed suddenly slashes the rate back to 0% or take the risk that excess deposits locked up in bonds take a fair value hit if the Fed suddenly raises rates because inflation spikes up from the tariffs. Based on all the data they know today, there is no way to tell what to do, nor any clarity on whether the returns on investment will be enough to compensate for the risk taken.

Should they stick with their current deposit pricing strategy and run a short-CD promotion in the branches for a while longer, or should they try a different approach to attract more consumer deposits through the brokered route? Whether or not to hedge interest rate risk to protect NIMs and net interest income, which, given heightened price volatility, does not come cheap to put on or take the chance that the Fed does nothing over the foreseeable future.

Not every decision is an easy call, and most are impossible. When you are dealing, as bank treasurers do every day, with multiple dimensions of interest rate and liquidity risk, they rarely are no-brainers, hence why they are so worried.

Who isn’t Uncertain and When Aren’t Markets Volatile?

Market volatility and uncertainty make them uneasy. But for all the teeth gnashing that goes on in bank treasury departments across this fair land about the market's ups and downs, for all the uncertainty and risk-off mentality the financial news media serves up, there is not much one can point to about either the economic or market narratives today that seems all that different from before Liberation Day. Maybe there is nothing to worry about.

Think about it. How is today's banking landscape different from what bank treasurers have seen since Covid? Maybe even since the Global Financial Crisis (GFC)? The terms "market volatility" and "economic uncertainty" are nothing new in the financial world. Bank treasurers have mentioned them in their daily updates well before the new year began.

They were flung around in bank treasury circles when the new Administration came in last January when tariff talk was just talk. Before the Fed started cutting rates in the previous fall, markets were moving around. The leading excuse bank executives gave for why 100 basis points of rate cuts were not getting their borrowers to get out of bed and start borrowing was uncertainty about the elections, further rate cuts and their timing, and the timing and potential severity of a recession because they were uncertain whether maybe the Fed had waited too long to cut rates last fall. They did not know whether to assume the brace position for the hard landing that was sure to come and never came or go all risk on and get to the party.

Even the Fed today wonders if it was as late to cutting rates last fall as it was late hiking them three years ago, as Chair Powell conceded during his press conference this month discussing last fall's rate cuts,

"I wouldn't say that what we did last fall was preemptive. If anything, it was a little late."

Bank treasurers are always uncertain about the interest rate picture, which is precisely why they instinctively want to be neutral on interest rates. Who can blame them? The rate picture can go in any direction all the time. There was debate at the Fed whether its 25 basis point rate hike in July 2023 was its last, just as there is debate today whether the 25 basis point rate cut it made in December 2024 was its last.

Why would any bank treasurer willingly make a call about the direction of the Fed's monetary policy today when even the Fed is uncertain what that will be? Given every piece of economic data it knows today, it may need to simultaneously raise rates to fight inflation and lower them to fight unemployment. As the CFO of a regional bank told analysts earlier this month,

"I think your guess is probably as good as mine as where we'll be in 60 or 90 days.”

No Fundamental Change in the Noisy Turbulent Data

Borrowers have always been uncertain about the economy, but that is not the main reason why borrowers hold off from borrowing. The chairman and CEO of a regional bank based in the southwest explained to an analyst during his bank’s earning call earlier this month that, yes, it was true that borrowers are anxious about the tariffs, but no one is really that worried about their businesses or the economy,

“I would say some are waiting. What they're really looking for in most cases is clarity…I would say…that there’s a level of confidence from a lot of people that they can pass along the cost…I don't think there's a lot of pessimism. I think there's some concern because they don't have clarity on what the answer is right now…that's what I've heard from customers.”

The consumer is not any different from a typical business owner. The consumer might be more worried about getting fired since the new Administration took office last January. According to the New York Fed’s Jobs Separation Expectation survey, household concerns about losing a job in the next year are up by 50% since the new year but well shy of the worries they had during Covid and not too off from the index average since the GFC. And expectations aside, consumers are just fine because they are employed today. And as long as consumers are employed consumers, they will be happy consumers, and happy consumers spend money, as the above-quoted bank executive went on to say,

“We continue to see the consumer spending money…on the home equity side, our mortgage numbers have been good…there's, on the margin, a little bit of slowing because there's some uncertainty, but it's interesting to me that some of the confidence numbers that I see published don't really seem to match up exactly with the spending numbers or what you're seeing in other areas. So, I don't think we've seen a big slowdown in the consumer at this point. I think the big reason is because people have jobs and jobs are growing…As long as they have jobs, I think they're going to continue to be reasonably stable.”

The employment picture is still basically the "same old same old," doing just fine, as it has been since the Fed began to tighten in March 2022. The JOLTS and Quits data suggest that hiring and quitting rates are unchanged for all the well-publicized Federal worker layoffs and tech layoffs this year.

Yes, bank treasurers are still complaining that they cannot hire good people and that even after they find good people, hire them, and train them, they find themselves right back where they were two years later, having to hire again to fill the same role because the hires from two years ago just quit. Employee tenure rates are falling according to the BLS, especially in the 25-34-year age group where it is under three years.

A case in point that bank treasurers know is what happens with their bank’s examiners. Bank treasurers are forever meeting new ones, because hiring and retention problems are as pervasive at the Fed, FDIC, and OCC as they are in the bank treasury space and the rest of the private sector. No one wants to stay in their jobs there. Meanwhile seasoned examiners move on to retirement and the brain drain has been telling.

But leaving aside worries of what might be happening to this country and its labor force’s work ethic, the good news remains that consumers are still spending and employed. The way economists sometimes talk, you would think the sky would have fallen by now. But no. OpenTable data suggests that diners might have canceled some dinner reservations in the first couple of weeks of April last month, but as of this month, diners are right back at it and cannot stop ordering steak for dinner. Business is booming at Steakhouse chains.

Good times! And uncertain times.

But to put today’s uncertainty into perspective, there was uncertainty yesterday, too. Before people were talking about the tariffs, before they were uncertain about the economy last summer, whether it might slow or even go into recession, there was uncertainty about the aftermath of the Silicon Valley Bank (SVB), Signature Bank, and First Republic failures and what they meant for the stability of the banking system's deposits. There has always been uncertainty.

Nor are bank treasurers only uncertain about the economy and the path of interest rates. Sometimes, they lie awake at night and contemplate existential uncertainties just like those who do not work in the financial industry may have, as in geo-political conflicts like the one that erupted just now between Pakistan and India or the ongoing conflict between Russia and Ukraine.

The prospect of a U.S. government default is just as existential, fears of which Moody's downgrade of the U.S. debt rating below AAA this month stoked. The many times the U.S. Treasury has had to resort to extraordinary measures to keep the U.S. government out of default because it could not resolve the debt ceiling, does not help calm investors fears, however improbable, for the credit safety of U.S. debt.

And where does all the worrying get bank treasurers? Nowhere because nothing ever really changes. The world has never ended, no matter how many times the doomsday clock is seconds before midnight. No asteroids have hit us yet. Meanwhile, back on Earth, the employment picture looks solid. The U.S. still pays its debts on time and in full. For all the worries last year about multi-family commercial real estate, the banking system is solid regarding its asset quality. Sure, there was some weakening in some portfolios (student loans, for example) last year.

But as the Fed's latest financial stability report found, echoing comments by the FDIC in its latest report on the banks, weakening trends are already stabilizing and and even at their modestly elevated state relative to a few years ago, credit issues in the banking system are still low. Banks may even lower their reserve for loan losses this year, in line with Current Expected Credit Loss accounting requirements.

The inflation picture continues to brighten even if tariff policy could derail the Fed's goals, the unknown effects of which are not in the data yet. Bank treasurers and their customers can worry about tariffs, but they still do not know what to worry about. You need data, and there is none, at least not yet. Even if the Fed wanted to act preemptively today, the way it did back in 2019 when it cut rates three times, it could not because it does not have the data to support the action, and data is all you have when your monetary policy runs on it. As Chair Powell explained during his press conference this month,

“In 2019 we cut three times. But the situation was that you had a weakening economy, and you had inflation at 1.6 percent. So that's a situation where you can move preemptively. Now we have inflation running above target…for four years…If you look at where forecasters are, they're all forecasting an increase in inflation…and then we've also got forecasts of weakening in the economy and some have recession forecast…We don't publish a forecast that assesses how likely a recession is; but in any case, it's not a situation where we can be preemptive, because we actually don't know what the right response to the data will be until we see more data.”

Data-dependent decision-making is all about uncertainty. The Fed is data-dependent, which is nothing new. Chair Ben Bernanke coined the term way back in December 2013 to explain his plans for winding down Quantitative Easing when he met with the press after the meeting of the Federal Open Market Committee (FOMC). Data dependence is a long tradition at the Fed. Chair Powell suggested that the Fed has been data-dependent since its establishment in 1914.

The Fed’s adherence to data dependence makes total sense. There is no sense in Chair Powell cutting interest rates if inflation and employment data are going up and down from one month to the next. One month’s data does not a trend make, and trends in the data are what the Fed needs to see to cut or hike.

Market Volatility, Prices Unchanged

Bank treasurers can say the same about market volatility. It is hard to read much of a buy or sell signal with trends in any market, fixed or equity. Like the traders they are, they know all about how to lose money trading momentum when markets are whipsawing the way they have been doing. Much has happened, but not much has changed, means stay put if you can.

The yield on the benchmark 10-year Treasury was 4.4% last July, with the Fed’s target range for the Fed funds rate stuck at 5.25%-5.500%. But then it plunged to 3.6% in early September last year before the Fed went on later that month to cut the rate by 50 basis points. It then climbed back up to 4.5% by mid-November after the elections, peaked at 4.8%, and then dropped to 3.9% at the beginning of April after the tariff announcement on April 2nd. Today, it is back to 4.5%. Measured by the implied volatility of the 10-year swap rate (Figure 1), rates have been volatile like this ever since the Fed began to raise rates in March 2022.

Figure 1: Implied Volatility of 10-Year Swap Rates

The equity markets were equally volatile but are also unchanged. The Dow Jones Industrial Average index was over 42,000 last July, rallied to 45,000 by the beginning of December, fell back to 42,000 by the beginning of the new year but ended the month back at 45,000 where it basically held until Liberation day, when it crashed at 37,000. Today it is back up at 42,000. The S&P 500 index is not quite as recovered, having traded over 6000 in the beginning of the year and now trading just under, but after first rallying back from the brink of correction when it fell below 5000 in the first week of April. The latest presidential tweets kicked the markets going into the Memorial Day weekend but the way markets are trading could recover or crash further in an instant with the next tweet.

Treasury Yield Curves Volatile But Unchanged

A lot has happened, but not much has changed. Yield curves, as usual, remain unreliable economic forecasters. As measured by the 2s-10s spread, for example, the yield curve averaged 50 basis points last month, and a positive sloped yield curve is supposed to signal a bright future for economic growth. According to the St. Louis Fed, the previous time this curve averaged 50 basis points was in February 2022, one month before the Fed’s first rate hike, which was supposed to darken economic growth prospects but ended up doing no such thing as the U.S. economic picture continued to sail on through the most dramatic rate hikes any bank treasurer had ever seen even if they started their career back in the 1980s. In July 2023, when the Fed again made history and ended its rate hiking cycle, the spread averaged minus 93 basis points, which every economist in the land said was as sure a signal as ever that a recession was, most probably, coming. Which bank treasurers know now never came.

Bank treasurers find the signal coming from the 3-month and 10-year Treasury spread just as difficult to intepret and which in recent years has been just as volatile as the 2-year-10-year spread. This month, the average spread was less than five basis points, and the last time this curve was as flat was in October 2022, the month when the Fed hiked Fed funds by 75 basis points rate for the third consecutive time, and the Fed's own dot plot projections had the economy falling into recession by 2023. Less than six months later, the 3-month-10-year spread inverted to minus 173 basis points and here we are this month back at 10 basis points. As for the 3-month-5-year curve’s gyrations, whatever noisy signal bank treasurers are picking up they would describe as uncertain.

Crypto Volatility

Crypto prices are also roughly back where they were when the year began, when the Administration published an executive order for the country to stockpile it, maybe even a little higher. Whatever bank treasurers are supposed to learn from following their trends is uncertain and subject to change on any given day. Thus, Bitcoin, the leading cryptocurrency that started the new year at over $100,000 per coin, fell to $83,000 in the first week of April, and now, once again this month, is back over $100,000 and rallied toward the end of the month to peak at $110,000.

Typically, when market prices crash the way they did last month on fundamental concerns, there could be a rebound of sorts, what rate strategists might call a bear market rally, sometimes also known as a dead cat bounce. The idea is that markets overcorrect and perhaps just overreact to bad news. But generally, dead cats do not return to where they were when they fell off a ledge, which is how fixed income and equity markets fell last month and then recovered.

Which forces specifically drove the unprecedented rebound remains uncertain but demonstrates the strong, resilient bid for financial assets despite economic and interest rate uncertainty, even financial assets of dubious value such as crypto, which relies on the great fool for its last bid. This bid is not scared off by market volatility. Not like bank treasurers who remain rate neutral and risk averse. Banks tightened credit underwriting standards last year, according to the Fed's latest senior loan officer survey.

Still, large private equity and credit investors are stepping up fast, becoming a key credit provider to consumers, edging out bank lenders. The banking industry finances the nonbank lenders, and the H.8 data shows that bank loans to nonbank financial institutions grew fourfold over the last decade to $1.2 trillion this month.

According to research by the New York Fed, foreign banks are growing as marginal lenders in the financial system. According to Fed's H.8 data (Figure 2), foreign branches and agencies' loans increased this month to over 9% of total bank loans, and 18% of commercial and industrial loans. Foreign branches and agencies also account for a quarter of all loans to nonbank financial institutions.

Figure 2: Total Loans Held By Foreign Branches and Agencies, Percent of Total Loans

Uncertainty is an Enduring Feature of Modern Monetary Policy

Uncertainty and volatility are part of the banking landscape and have been for a long time. New York Fed president John Williams, speaking at an economic conference this month, observed that,

“After 30 years in central banking, I can unequivocally say: “Uncertainty is the only certainty in monetary policy.” Or, in the words of Alan Greenspan, former Chair of the Federal Reserve: “Uncertainty is not just an important feature of the monetary policy landscape; it is the defining characteristic of that landscape.”

A central message that bank management delivered to investors in this earning cycle is that the future is too uncertain, and outcomes can go either way. On the other hand, they remained optimistic that today’s clouds would disappear by the summer when the Fed most likely begins to cut interest rates, which is uncertain.

According to the CME’s FedWatch monitor which is based on the Fed funds futures market and which like every other market these days is volatile and uncertain; with five FOMC meetings left in the calendar year, there is almost no chance of a rate cut before the July meeting. If the Fed does not cut by July, then it most likely will have cut at least one time by its September meeting. There is also virtually no chance that the Fed has not cut Fed funds by 25 basis points to 4.00%-4.25% by the FOMC’s October meeting. By its December meeting, there is only a 25% chance that the Fed will cut rates only once in 2025 and no chance whatsoever that it will hike rates this year because of tariffs.

Those are the odds, but our subscribers’ guesses are as good as the FOMC’s what happens. Atlanta Fed president Bostic told reporters this month he still held out the hope for one cut this year,

“For me right now, I’m expecting it’s going to take a bit longer for that to sort out. ... I’m leaning much more into one cut this year, because I think it will take time, and then we’ll sort of have to see.”

According to New York Fed president John Williams, uncertainty is not going away any time soon, at least not as far as monetary policy is concerned,

“And there’s no doubt that uncertainty will continue to be the defining characteristic of the monetary policy landscape for the foreseeable future. This is a direct result of structural changes in the global economic environment such as those posed by artificial intelligence, deglobalization, and innovations in the financial system—not to mention the perennial challenges of measuring the so-called star variables such as r-star.”

Economic uncertainty is compounded by growing challenges economists face using standard economic measures to describe the economy. Measuring u*, the natural unemployment rate, and y*, the natural GDP rate, for example, are getting harder to estimate. Fed Governor and former Vice-Chair of Supervision Michael Barr noted in a speech this month that AI applications could impact labor markets and challenge long-standing assumptions built into standard econometric models used today,

“If AI shifts the workforce toward groups that have higher labor force attachment but lower unemployment rates (such as college graduates), the result could be downward pressure on u*. It should be stressed that u* is never directly observed and is difficult to discern in real time.”

QT and Uncertainty

The Fed’s conduct of QT also contributes to the general uncertainty that colors the financial landscape. Its goal has been to reduce the size of its balance sheet while maintaining reserve deposits at a level that well exceeds demand for reserves—what the Fed describes as abundant. Banks demand reserves because they need them as an overnight, risk-free investment, a store of liquidity for the balance sheet, and for payments over FedWire.

To confirm that the level of reserves is abundant relative to their needs, the Fed refers to “reserve demand elasticity” (RDE). RDE measures the sensitivity of the Fed funds rate to changes in the supply of reserves. When demand exceeds the supply of reserves, any change in supply will cause a significantly greater change in the Fed funds rate than today, when reserves are abundant relative to demand, and changes in the supply of reserves have little to no effect on the Fed Funds rate. Indeed, based on RDE, the Fed continues to be confident that the level of reserves is sufficiently abundant even after it reduced its System Open Market Account (SOMA) portfolio by $2.5 trillion to $6.3 trillion and plans to continue to reduce it by roughly $20 billion a month. (See this month’s chart deck, Slide 8 for more detail on the RDE metric.)

But there is a fundamental problem with its plans for QT and trying to avoid an accident like what happened in the Treasury repo market in September 2019 when a sudden shortfall in reserve supply caused SOFR to jump from 1.5% to 5.2% overnight.The dividing line between abundant and less than abundant (say, “ample”) moves around, and like the stars (r, u, and y), is difficult for the Fed economists to pinpoint. And probably because the Fed does not know precisely where to draw lines, it has left the level of reserves unchanged since it began QT.

So, maybe there is a lower level of reserves that would be sufficiently abundant for the banking industry so as not to cause an accident. But the Fed has no confidence or willingness after three years since it began QT to find out where that line is. QT to date has been less about shrinking reserves and more about demonstrating that the Fed can cut interest rates and tighten monetary policy by shrinking SOMA at the same time.

The second problem is that there are many more moving parts on the Fed’s balance sheet than just the SOMA portfolio. There is the Treasury General Account, the Reverse Repo Facility to think about that also absorb reserves. Currency in circulation is another moving part which absorbs reserves and also increase on demand by the public for physical cash. Indeed, in these uncertain times, cash is king everywhere and everyone wants it. The public’s cash stash is up these days (see Slide 9 in this month’s chart deck).

Stockpiling Cash, Gold, and Hedging Risk

Bank treasurers are understandably cautious about leaving too much of their earning assets in overnight reserves, given the risk that the bottom falls out of the economy because of tariffs and the Fed has to cut rates overnight. But they still want reserves as a store of liquidity, and the last two years since the SVB failure drove home the point that cash is king. It pays to sit on more cash than might have been the case before. Notably, regional and community banks learned this lesson well. Large banks account for 11% of total reserves held by domestic banks. But in the last year, small banks with total assets under $100 billion grew their reserve deposits while reserves held by their larger peers edged down (Figure 3).

Figure 3: Reserve Deposits

Bank treasurers are not only turning to holding more overnight reserve deposits as a source of liquidity and safety. According to recent call reports, they are hedging more of their interest rate risk exposure with derivative contracts (Figure 4). The notional principal of interest rate contracts not held for trading surged right after the regional bank failures in Q2 2023 and then fell back as the Fed paused further rate hikes in the second half of 2023. But since Q3 2024, hedging activity again appears to be on the rise.

Figure 4: Interest Rate Products Not Used For Trading, Notional Principal

Eris Innovations, a corporate sponsor of the newsletter and inventor of the Eris SOFR Swap Futures contract, traded on the CME which is also a corporate sponsor for the newsletter, noted a surge in trading volume and open interest in the contract this month. The surge was driven by large block trades. Eris believes the trend this month could be a sign that financial institutions are adding interest rate risk hedges through futures contracts rather than swaps, given the cost advantages of using former instead of the latter. Hedge funds, bank ALM managers, REITs, and other mortgage traders make up most of the trading volume in these contracts, which are traded anonymously through a futures commission broker, such as R.J.O’Brien, another one of the newsletter’s corporate sponsors.

Investors reflexively turn to gold as an inflation hedge, but more so in times of uncertainty when they want the sense of a tangible asset and reliable store of wealth. As inflation continues to cool, gold’s appeal as a store of wealth and security would seem to explain its sudden surge this year to top out over $3,400 this month. (Figure 5). As prices have soared, jewelry stores and pawn shops are seeing a veritable gold rush as people rush to turn their valuables into cash.

Figure 5: Gold Bullion ($s per Contract)

Uncertainty driven demand for cash probably explains why the growth rate of currency in circulation on the Fed’s balance sheet rebounded to 5% in the last year (Figure 6) after falling to 0% in the years after Covid. When there is uncertainty and volatility, financial market participants will always turn to cash. They are sitting on trillions and trillion as the chief executive as a major asset management firm told attendees at a forum this month,

Figure 6: Currency in Circulation

"There is 12 trillion Euros sitting in bank accounts in Europe. In the United States, there's $11 trillion sitting in money markets funds. When there is uncertainty, you are going to keep more and more money in cash and that is what we witnessed."

Bank Treasurers Want Good Rules, Not No Rules

Regulatory relief brings its own set of uncertainties to the bank treasury landscape because, so far, there are promises and headlines. Still, regulators have not drafted, much less finalized, any new rules to replace the ones that the banking industry does not like. Bank treasurers find it hard to plan, much like with the tariffs, when the new landscape for rules is still hazy and uncertain. Pulling the draft proposal for the Basel 3 Endgame is one thing. Writing a new proposal and finalizing it so the banking industry can move and make decisions based on the new rules is another.

Bank treasurers are happy about this year's new banking sheriff in Washington. A new vice-chair of supervision is coming as soon as the Senate votes to confirm Michelle "Micky" Bowman. Sympathetic to the argument that bank supervision is overreaching and believing in sensible and reasonable regulation, in tailoring rules to fit an institution's size and complexity, as she testified at her confirmation hearing last month, bank treasurers expect her to be a friend, not an enemy. They were understandably cheered when she testified at her confirmation hearing last month,

“I will continue to rely on a tailored approach, especially for community and regional banks. Tailoring is fundamental to ensuring we maintain and enhance the diversity of the U.S. banking system, which must include and support banks of all sizes. The U.S. regulatory framework has grown expansively to become overly complicated and redundant, with conflicting and overlapping requirements. This growth has imposed unnecessary and significant costs on banks and their customers.”

Each crisis brought new rules to prevent the same crisis from happening again next time, and so today, there are so many rules layered on older rules that maybe even AI could not figure out what bank treasurers are supposed to do. This year, the FDIC repealed, rescinded, and pulled back regulations and guidance on mergers and acquisitions, board governance, brokered deposits, and cryptocurrencies, which it adopted over the past two years after the regional bank failures. Examination staff are getting fired in droves.

The Administration decimated staffing at the CFPB, an agency created under the Dodd-Frank Act in response to abuses in consumer lending leading up to the GFC. It pushed to merge into the Treasury. Partisans in Congress want to eliminate the Public Company Accounting Oversight Board (PCAOB), which Congress created in 2002 in the wake of the Enron and WorldCom financial scandals) and merge it with the SEC.

However, exactly how the new era of good feeling will work remains to be seen. Maybe the era of skepticism and mistrust after the failure of SVB is over. But the replacement with an era of confidence and trust that bank management knows what it is doing. It will not screw up like it has done time and time again over the past decades of bank crises, from the S&L crisis in the early 1980s to the bank crisis in the late 1980s and early 1990s, from the GFC to the regional bank crisis, inspires no confidence that it will last very long.

Bank treasurers know that, guaranteed, after the following big bank screws up big time, there will be no bank supervisors talking warmly about tailoring and supporting banks of all sizes. Congress will have no partisan supporters for the industry and the suffering it goes through because of too many rules. There will just be more rules.

Perhaps the financial system does not need a specific agency for the CFPB and the PCAOB. There is a good argument to make that when you give someone one job to do, they will do it very well, and maybe more than necessary. However, consolidating, simplifying, and updating complicated rules cannot be accomplished by just ripping them up. Ripping rules up is not a public policy. Writing rules are.

Maybe the new rules, whenever rule makers get around to writing them, will spell relief, but it depends on how they write them, and even then, their effect will be uncertain. The Fed might push through changes to relax the Systemic Supplementary Leverage Ratio (SLR) for the largest banks to help them hold more Treasurys, which Chair Powell and Governor Bowman both support. Nevertheless, how the SLR will be revised, whether changes will be permanent or temporary, and whether Treasurys will be exempt 100% or less need decision-making.

However, uncertainty pervades decisions about the SLR and whether relief would be enough to get the largest banks to buy and hold more Treasurys. Most of the rules pushed by regulators last year, including the charges for operational risk and trading and the push for a 10-day LCR, are probably gone. However, it is still sound public policy that banks should adjust their liquidity planning as the potential for another SVB-style bank run can happen again.

The rules are complicated and detailed because the industry is complex and detailed. Some rules are obscure to the public, such as Reg O, which governs insider lending, which the Fed last updated in 2021. Some rules address problems that are no longer relevant. Congress intended the Glass-Steagall Act for a banking system that no longer existed when it was finally replaced in 1999 by the Gramm-Leach-Bliley Act. Sometimes the rules are duplicative. Sometimes, the rules are not even rules; they are guidance provided by one supervisory agency, such as the Fed, which conflicts with advice from the FDIC or the OCC.

But like everything else in the financial industry, bank regulation is cyclical. Sometimes, regulators over-tighten the rules, and sometimes, they over-ease; there are risks to the industry's health, safety, and soundness when they ease regulations and tighten them. The financial sector wants less complicated, conflicting, and counterproductive regulations but still wants rules of the road. It wants sensible, reasonable rules, as Governor Bowman said last month,

“Supervision cannot eliminate risk from the banking system, but it can and should promote sensible risk management that enables the banking system to support economic growth and serve the financial needs of all Americans.”

Promoting sensible risk management, replacing conflicting rules with coherent instructions and guidance, and creating an environment where the financial industry can serve the needs of the public requires thoughtful leadership and experienced hands, both of which might be in short supply as the current administration keeps firing everyone.

Which is why bank treasurers worry so much. When there is a problem, bank treasurers always want to know who to call, and now there may be no one on the other end of the phone to pick up and answer when they do. Bank treasurers worry about this and everything else all the time, which is not healthy, and something else they worry about.

The Bank Treasury Newsletter is an independent publication that welcomes comments, suggestions, and constructive criticisms from our readers in lieu of payment. Please refer this letter to members of your staff or your peers who would benefit from receiving it, and if you haven’t yet, subscribe here.

Copyright 2025, The Bank Treasury Newsletter, All Rights Reserved.

Ethan M. Heisler, CFA

Editor-in-Chief

This Month’s Chart Deck

Key takeaways from Q1 2025 bank earnings results that would describe the situation in which almost every bank treasurers find themselves today include good news on the net interest margin (NIMs) front (Slide 1). While NIMs at the largest banks stabilized as deposit funding cost pressures leveled off, NIMs at smaller regional banks increased. The bad news is that negative fair value impairment on bank investment portfolios, including both available-for-sale (AFS) and held-to-maturity (HTM), deteriorated in Q1 2025 as bond yields climbed in response to inflation worries and tariff uncertainty (Slide 2). Uncertain which way interest rates and the economy are going, bank treasurers are increasing the hedging of the balance sheet, primarily through receive fixed derivatives. Bank treasurers, and other managers at REITs, mortgage-Servicing, and hedge funds drove a surge in open contracts of the Eris SOFR Swap futures (Slide 3) this month as risk managers seek interest rate protection and maintain their interest rate sensitivity.

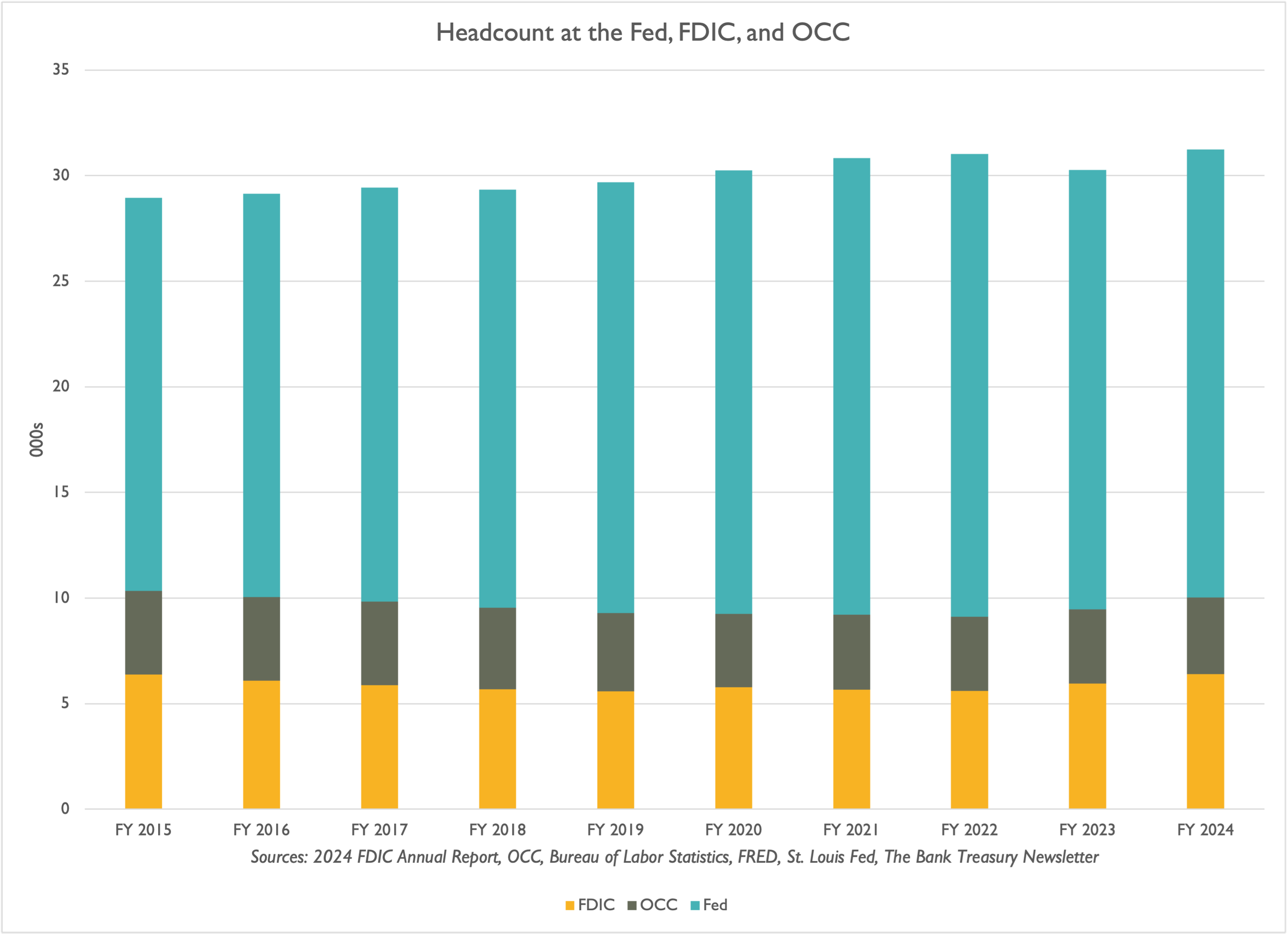

Meanwhile, credit risk in bank loan portfolios continue to rise but remains low historically (Slide 4). In addition, home prices continued to increase this year, a sign of financial health for homeowners (Slide 5). Two banks failed in 2024, which cost the FDIC insurance fund less than $1 million, compared to five banks that failed in 2023 (including Silicon Valley Bank, Signature Bank, and First Republic), which cost it $19 billion (Slide 6). The FDIC, along with the Fed and the OCC, plan to pare back headcount by 10% in the next couple of years, in line with the new Administration’s push on government efficiency and despite concerns that exam functions are already understaffed and challenged to hire to fill empty positions. Combined, the headcount at the three agencies equaled more than 30,000 last year, two-thirds of which is staffing at the Fed (Slide 7).

Three years after the Fed began to shrink its System Open Market Account portfolio under Quantitative Tightening, its balance sheet is down by $2.2 trillion, to $6.7 trillion. Its monthly average balance of reserve deposits remains unchanged at $3.3 trillion. Based on the Fed’s study of reserve demand elasticity, the sensitivity of the Fed funds rate to changes in the level of reserves, sensitivity is virtually zero, which the Fed interprets to mean that reserves remain abundant in the system and that the risk of a sudden shortfall as happened in September 2019 in SOFR is negligible (Slide 8).

Cash is king, and everyone wants it to have and hold in times of uncertainty. Bank treasurers are not the only ones flocking to cash as a source of liquidity and safety against unforeseen circumstances; The average consumer still holds more cash on hand today than held before Covid (Slide 9), even though credit cards continue to dominate payments because more and more commerce occurs over an app than in-store. Of course, to have a credit card means having a checking account. According to the Atlanta Fed’s survey of consumer payment preferences, the number one reason why someone would not have a checking account is because they do not like dealing with banks (Slide 10), more so than complaints about fees or that the bank card issuer does not have branches conveniently located.

Bank NIMs Recover

Bond Portfolio Fair Value Impairment Worsens

Hedging Soars With Eris SOFR Swap Futures

Credit Continues Climbing Back To Norm

Home Values Reach Higher

Banks Back to Safe and Sound

Bank Supervisors To Get Chopped

Fed Funds Inelasticity Remains Unchanged

What’s In Your Wallet?

Cash Users Hate Dealing With Banks