BANK TREASURERS OUT OF AFRICA

The President nominated former Fed Governor Kevin Warsh to become the 17th chair of the Federal Reserve. Republican Senator Tom Tillis, who chairs the Senate Banking Committee, agreed to begin the confirmation process but vowed to withhold a vote on his nomination until the Department of Justice ends its criminal investigation of Chair Powell and the makeover of the Eccles Building. Powell's term as Fed chair ends in May, and if the Senate does not confirm Kevin Warsh by then, Vice Chair Philip Jefferson will serve as interim chair. While his term as current chair of the Federal Reserve ends in May, Chair Powell's term as a governor of the Federal Reserve Board does not end until January 2028, and he may continue to serve and vote in Federal Open Market Committee meetings until then.

According to the nominee, he remains a steadfast believer in Fed independence and a hawk in the fight against inflation. However, he supports the Treasury Secretary and President's position that the Fed funds rate is too high and justifies the inflationary risks of cutting rates when inflation today remains above the Fed's 2% target, arguing that Artificial Intelligence (AI) productivity gains will be disinflationary, that AI will power economic growth, and that AI will increase wages for consumers to spend. Notably, Michael Barr, Fed Governor and former Vice Chair of Supervision, said this month that AI will likely disrupt the job market, at least in the short term.

While he was an initial supporter of quantitative easing in 2008 during the Global Financial Crisis (GFC) when he was a Fed governor, he was concerned by 2010, before he resigned, that the Fed was going too far and to this day blames the Fed's "bloated" balance sheet for holding back economic growth. Famously, in the last year, he has spoken about a new Treasury Accord that would improve coordination between the Treasury and the Fed on the conduct of monetary and fiscal policy and also lead to a smaller balance sheet. But since the original Treasury accord in 1951 was about freeing the Fed to conduct monetary policy independent of the Treasury and raise rates if needed, exactly what a new Treasury accord would mean remains unclear. Indeed, even if the Fed under the nominee did end up cutting the Fed funds rate this year (even though markets see less chance for a rate cut this year than they did at the end of last year) it does not control long term interest rates unless the Fed began using its balance sheet and targeting specific maturities on the yield curve as it tried to do during Operation Twist.

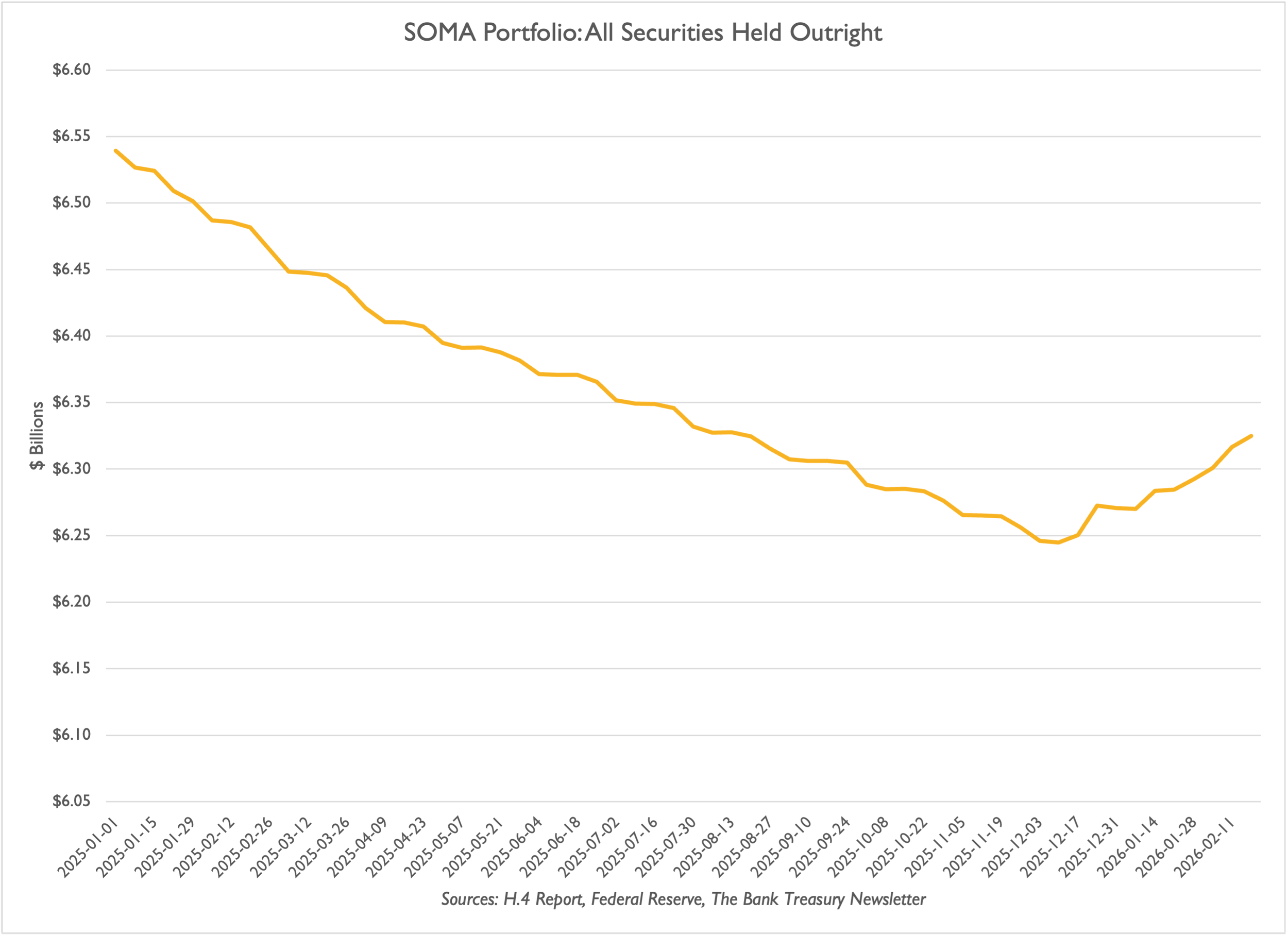

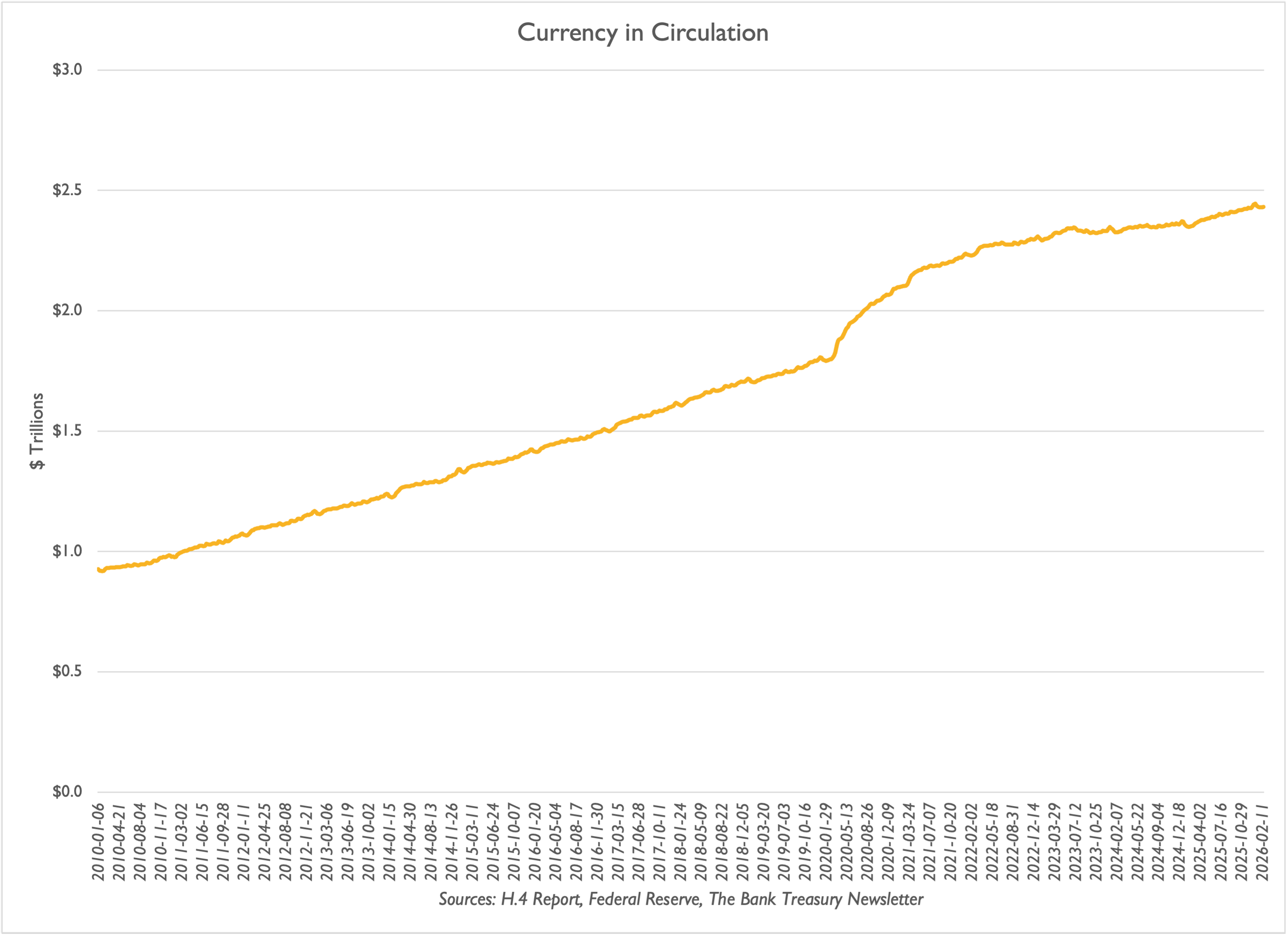

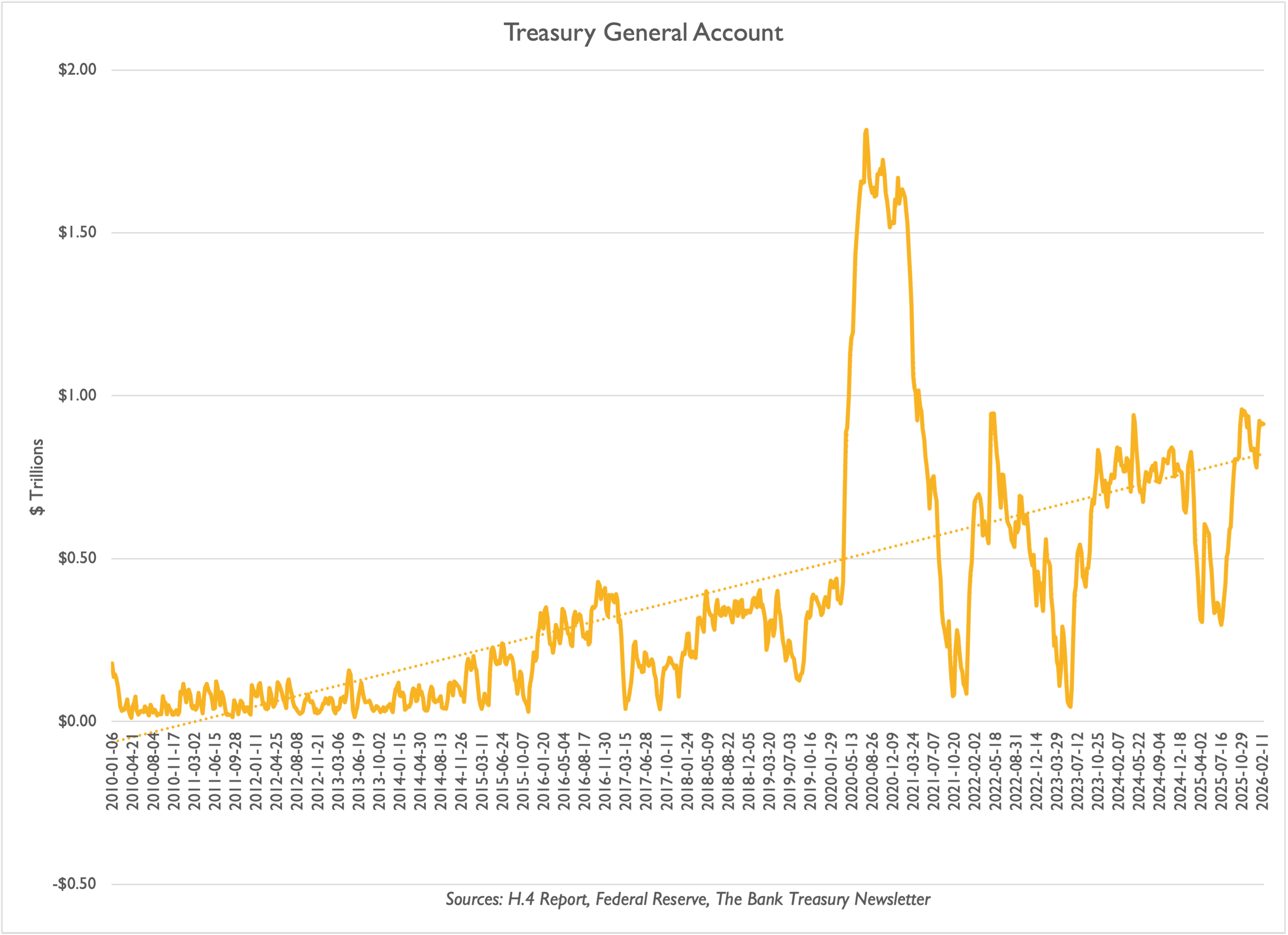

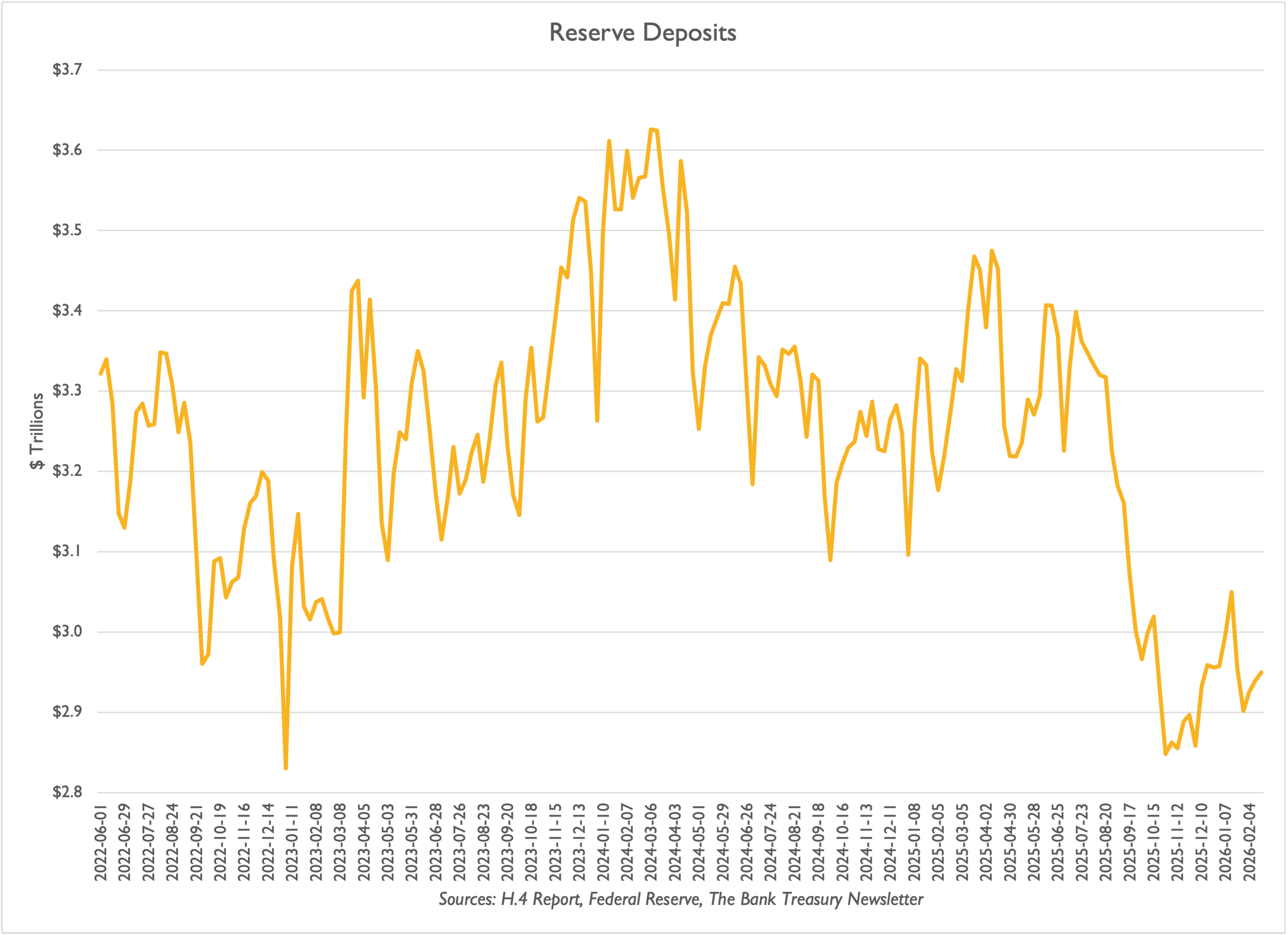

Critically, the Fed's balance sheet has little room, if any, to shrink as detailed in this month’s chart deck. Its System Open Market Account (SOMA) portfolio equals $6.3 trillion, including $4.3 trillion Treasurys and $2.0 trillion Agency Mortgage-Backed Securities. At $2.4 trillion, the supply of paper money printed by the Fed and one of the largest liabilities on its balance sheet compares to the $1.0 trillion in circulation when Kevin Warsh was governor. In addition, the Treasury's checking account is $0.9 trillion, leaving the Fed with a $3.0 trillion reserve deposit balance, which is three times the balance that existed when he resigned in 2011 to return to the private sector. Nevertheless, reserve demand elasticity, a measure the Fed calculates to describe the supply of reserves in the financial system, suggests there is little room to shrink reserves. Add to this, Fed economists, by their own analysis, believe that the Securities and Exchange Commission (SEC) 's mandate, going into effect next year, which will require dealers to centrally clear all Treasury and repo trading, will increase demand for reserves and thus leave the Fed with no room to shrink its balance sheet at all.

Unlike his stated position on Fed independence, with respect to its conduct of supervision, the nominee is a critic of its approach, which he believes is focused on form over substance and saddles community banks with burdensome regulations unrelated to the business of safe and sound banking. Miki Bowman, the Fed's Vice Chair of Supervision, is another strong proponent of shifting bank exams back to the material risks banks face and reducing the subjectivity in supervisory ratings. This month, she proposed changing the risk-based capital calculations for mortgage loans and mortgage servicing rights assets to help banks return to mortgage lending.

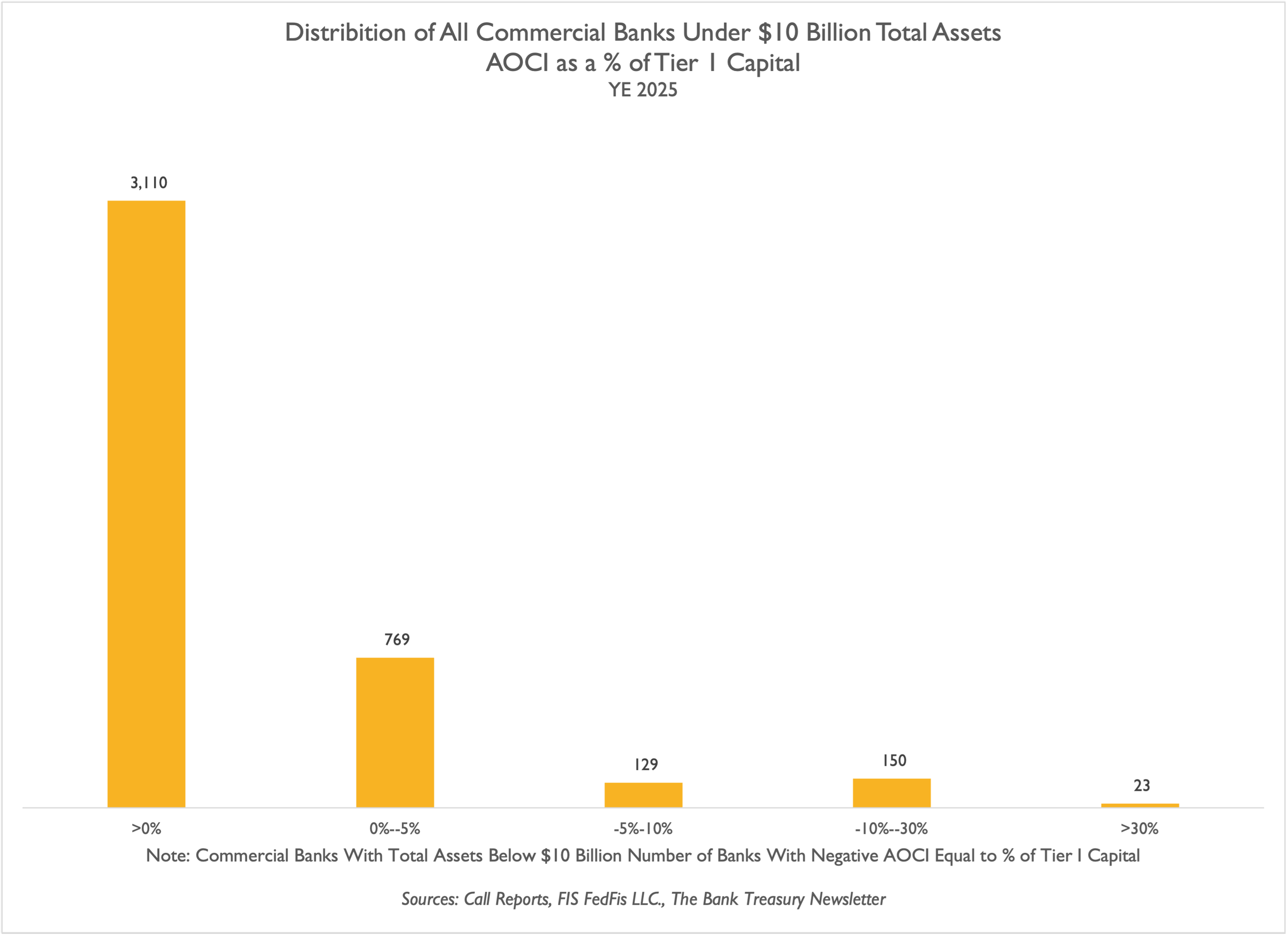

Metropolitan Bank and Trust, a $261 million-asset bank in Chicago, Illinois, became the first bank to fail this year. Only two banks failed last year. The bank held its bonds entirely in available-for-sale (AFS), and according to its final call report, its unrealized losses in the portfolio totaled $14 million, compared with its Tier 1 capital, which was less than $8 million. There are 23 banks in the U.S. as of YE 2025 with assets under $10 billion and with unrealized losses exceeding 30% of their regulatory capital, which bank supervisors allow them to exclude from their capital calculations.

The Small Business Administration (SBA) announced that it was relaxing rules for forming Small Business Investment Companies (SBICs). First launched in 1958, Congress intended the program to promote small business investment. Kelly Loeffler, the SBA head, expects the new rules to promote investment in technology. SBICs are on the radar of bank treasurers seeking bank-elegible investment returns that earn credit under the Community Reinvestment Act (CRA).

It is a good time to apply for an industrial loan company (ILC) charter, as the FDIC approved applications from Ford and GM late last month. ILCs technically are not banks, but they can accept deposits and expand across state lines. There is a long line of industrial companies that have applied for ILCs to let them get around the long-standing prohibition in banking law against mixing commerce and banking, as ILCs are not subject to the Bank Holding Company Act. The last charter the FDIC approved was in 2020, and before that, it had not approved a charter since 2006. Most of the ILCs in operation are headquartered and supervised by the Utah Department of Financial Institutions.

The banking industry lobby is fiercely opposed to ILCs. Still, it is even more worried about the Office of the Comptroller of the Currency (OCC) push to introduce cryptocurrencies and foster the growth of stablecoin issuers. Towards that end, ithas approved six trust bank charters so far this year, five of which will perform only safekeeping and custody services to support stablecoin issuers, and a sixth, which the OCC will also allow to issue stablecoins. The National Credit Union Administration (NCUA) proposed to let credit unions become stablecoin issuers, provided they abide by the same regulations that apply to commercial bank issuers; however, bank supervisors have not even finished writing the rules for banks to issue stablecoins, which are due under the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS Act) by July 18ththis year.

The Bank Treasury Newsletter

Dear Bank Treasury Subscribers,

Jombo fellow bank treasury enthusiasts, and greetings from the Serengeti in East Africa, where your intrepid editor in chief has been on a safari vacation. Everything you heard about the place is true. It is amazing, beautiful, stunning, its views sublime and worth the cost, if not the schlep to get here from New York. As far as trips go, it is a worthy addition to the proverbial bucket list if ever there was one.

Serengeti, meaning endless horizon in Swahili, should be the perfect place for bank treasurers to take their minds off their endless headaches at work and get lost in another type of complex ecosystem for a change. Countless species of reptiles, mammals, birds, and fish, not to mention an infinite and assorted array of grasses, plants, and trees, all live here to distract bank treasurers from their daily distractions in next-level glamping style, where your every wish, including indoor plumbing and nightime turndown service, is included in your tour package. You’ve got everything here to keep you happily engaged, and with the iPhone camera in hand, memories to last a lifetime.

You have the periodic microdrama of a baby wildebeest getting separated from its mother. You can hear its plaintive cries, “mama, mama, bleh, bleh, and, unfortunately, watch it end up as dinner for a hungry cheetah. Tragic? No. As your Maasai guide says, it is just hakuna matata, is what it is, or, as one learns from watching Disney’s “The Lion King”, one of many movies you watched flying for a day and a half to get here, just the circle of life. Hakuna matata!

But you can also get engrossed in macro-drama: how climate change is causing habitat loss, endangering the already endangered giraffes, and creating hungry hippos who feed off of the flora, apparently, and then release noxious greenhouse gases of the rotten egg variety. On the luxury safari your editor in chief went on, you can learn so much, like how climate change can affect you personally. For example, you know that song about blessing the rains out of Africa? Yeah, that came to mind a few times on the afternoon game drives.

Because, despite your plan to come during the dry season, not the rainy season, the rains came anyway. And when they came, usually around 5:30 PM, when the sun was setting, you got drenched to the bone, and, remarkably, for the Apple Maps on your phone telling you that you were smack dab on the imaginary equatorial line, you were left freezing. Pulling out a poncho for you and offering you a glass of South African wine while you waited out the rain to resume the drive and take another picture of the ostriches, blessings aside, your guide blamed the rains on climate change. Yeah, hakuna matata, what does not go down well with a South African rose?

Sante sana, and thank you very much! Yes, there is a danger that talking too much to your guide about the weather can turn into an off-topic discussion that brings you back to work. Just mentioning the term “climate change” to a bank treasurer these days is going to be a no-no for obvious political reasons (although raise your hand if you even remember anymore what ESG stands for or why you cared). But more often than not, mention climate change, and you are liable to find yourself in the middle of a heated debate about how the climate is changing for the dollar as other currency regimes try to replace it.

But you fall back into work thoughts even when all you are trying to do is show polite interest in your guide’s story. For example, be careful not to offer advice while waiting out the rain, to show off how you spend too much time at work researching hot topics in bank treasury. Like, don't ask your guide what they know about microfinance in emerging markets or how it can help their fellow villagers who have suffered from climate change. Discussions like this can be a slippery slope to thoughts like remembering that, just before you left on the safari, the Small Business Administration (SBA)announced that it had reduced the red tape for forming Small Business Investment Companies (SBICs)

SBICs Made Simpler

Kelly Loeffler, the administrator of the scandal-plagued SBA, ordered an audit of the 8(a) program, which small businesses use to procure federal contracts. But the next day, she announced good news about SBICs, claiming that the relaxed rules would help emerging businesses in a first-world country like the United States. By streamlining the application process, she said, it

“…ensures capital can flow more efficiently to qualified emerging growth companies ranging from startups to manufacturers who are powering innovation, strengthening critical supply chains, and securing America’s industrial future by building today.”

As detailed in a 2015 OCC report, Congress established the SBIC program in 1958 to encourage business growth. SBICs are privately owned investment funds that qualify as bank-eligible investments and receive credit under the Community Reinvestment Act. Bank treasurers mainly focus on this asset class because of its returns, but unlike typical assets they add to their portfolios, these assets usually do not pay off for 10 to 15 years. As limited partners in the fund, banks commit an initial amount and then disburse funds over time, typically in 25% increments over four years. However, they also need to be prepared to fund their entire commitment upfront if the fund’s general partner requests it.

These assets pay well, but, as bank treasurers also know, they have a lot of the proverbial “hair on them” and require close, focused attention. They are complicated: you need to review reports, know who the general partner is and whether they know what they are doing, and be prepared to lose principal when things go wrong. SBA debt is triple-A, government-agency paper, but this does not mean that the SBA government guarantee covers an SBIC investment made under its guidelines.

SBICs usually take several years before they start generating returns for their investors. To clarify, they are not as liquid as your underwater bond portfolio held in AFS. Although they are exempt from regulations like the Volcker Rule, they would be risk-weighted at a minimum of 100% for regulatory risk-based capital purposes, and sometimes even higher if the investment in the SBIC exceeds 10% of a bank’s equity.

Endangered Species

There is more to learn, but trying to stay focused on the safari, your editor in chief fumbles with his binoculars at a few distant blips on the horizon that the guide says are a lion stalking a zebra and a baby warthog. However, they are hard to make out until—oh, yeah, you suddenly see it, but not long enough to also take a picture on the phone. Admittedly, you probably would have noticed them sooner and taken the picture if you could resist for a minute from multitasking to check your smartphone and track the latest blip on the market’s horizon.

But as our readers know, it’s hard to compete with the bank treasury news feed. Thanks to surprisingly good cellular service in—let’s face it—the middle of nowhere, the bank treasury news never stops, and thanks to jet lag, you never sleep. Because, let’s be blunt, the crash in Bitcoin late last month is definitely a bigger deal than some dumb lonely zebra or warthog’s life-and-death struggles in the Serengeti. Especially given the Federal government’s push for stablecoin issuance. Hakuna matata!

At some point during the safari, after spotting the umpteenth giraffe, you kind of get into a mindset that if you've seen one, you've seen them all, even the cute babies. Giraffes are an endangered species, sure. But when your editor in chief hears the word “endangered,” what comes to mind? Community banks. Yes, which are losing ground to credit unions and large banks that are acquiring them at a faster pace.

Yeah, sure, giraffes are peaceful animals; why would a poacher want to hurt one, or why would humanity let them go extinct due to climate change? But community banks are also being driven out, and this is a nationwide disaster, partly because of the favorable tax-exempt status credit unions have and their aggressive expansion into traditional commercial banking in recent years.

Here in the Serengeti, giraffes are everywhere you look, even if there are only about 117,000 of them left in the Serengeti. There are fewer than 3,400 community banks left with total assets of less than $1 billion and headquartered on main streets across America, according to Q4 2025 call reports; their numbers may be a quarter of what they were just 25 years ago. Everything serves its purpose, hakuna matata. Giraffes feast on the leaves from the thorny acacia trees that are everywhere. You do not want to get pricked by those thorns, so it is good for the giraffes to clear them out.

Did you know that you can tell boy giraffes from girl giraffes by how colorful their spots are? That's a helpful fact your editor-in-chief noticed while browsing his phone. But getting back to work, is it too much to ask for more color on the community bank that failed last month? With $261 million in total assets, the Chicago-based Metro-something bank’s entire capital position was affected by negative AOCI, due to its bond portfolio concentrated in long-duration Treasurys and pass-throughs. The mess Metropolitan Capital Bank and Trust left behind will cost the FDIC nearly $20 million to resolve.

Admittedly, you don't get your hands as dirty cleaning up a bad bank as you would if you were cleaning up the mess left by an elephant, a rhino, or a water buffalo. Your guide can become very scatalogical at times, helping you distinguish simple mud from something else. But for a small bank, it still left enough of a mess that the FDIC’s purchase-and-assumption agreement with First Independence Bank required it to retain $10 million in total assets from the failed bank. It is a common outcome lately with the FDIC and these purchase-and-assume deals, where the FDIC has to agree to assume some risk to complete the deal. The FDIC just did the same with the Santa Ana bank in Texas, which failed last June.

And Metro’s failure is a notable tragedy not only because it was the only bank to fail so far in 2026, after two failed in 2025, and because any bank failure these days, with the industry in tiptop form as bankers reported last month, is a rarity. Bank failures are like the sighting of a black rhino, but maybe ever rarer than that. But how do bank treasurers get past the fact that the bank examiners let Metro’s problems fester for almost three years before they shut it down?

How did this happen? Were they sleeping, like the lions that sleep everywhere around here? And what does their failure say about other banks in the same situation with their bond portfolios? By the end of 2025, 23 banks had total assets under $10 billion and negative AOCI exceeding 30% of Tier 1 capital (Figure 1).

Figure 1: Distribution of All Commercial Banks Under $10 Billion Total Assets, AOCI as a % of Tier 1 Capital: YE 2025

Maybe the bank’s failure was for the greater good, and maybe the new owner of its assets will put them to more productive use. Hakuna matata. In 1960, Joy Adamson and her husband, George, a game warden, moved to East Africa to care for lions, and after a long story, they ended up adopting Elsa as a house pet. A star and an Oscar-winning song were born from the book Joy wrote. Eventually, they released Elsa back into the wild. Sadly, she died at age five, heartbreakingly breathing her last while she lay in George’s lap from a disease she caught from a tick bite.

Endangered Babies

Hakuna matata, though, because she apparently found time before her early demise to mate and produce offspring—a miracle in itself, considering how much these animals sleep all day. They do seem cuddly and peaceful when they are recumbent and quiescent, but don't be fooled. According to the guide, male lions compete to mate with the females in a pride and will kill and eat all of a lioness’s cubs with a rival before mating with her themselves. Here's another interesting fact: to protect their offspring from a violent end, females will pretend to have sexual relations with a challenger male so that their cub’s parentage remains uncertain. Is that what happened to Elsa, one wonders.

Look, life in the Serengeti is nasty and brutal, similar to the 17th-century rationalist philosopher Thomas Hobbes’ state of nature. It revolves around survival of the fittest, where most of the young and weak don’t survive for long. That’s how nature works. After lions, cheetahs, and leopards finish chasing, killing, and eating them, jackals and hyenas come in to finish the job, even eating the bones. And that’s considered a good outcome. Hyenas, unlike other predators, have no problem eating their “dinner” while it is still alive.

Baby wildebeests and zebras are vulnerable, as are de novo banks. Regulators want de novo banks to hold more capital than seasoned banks because they face a higher risk of failure when they are new. However, the number of new bank charters that regulators are willing to approve is only a small fraction of the mergers approved each year. Additionally, investors have been reluctant to invest in the industry for years. As a result, the banking industry, like the giraffes, is quickly becoming an endangered species on its own. According to FIS FedFis, LLC, the FDIC has approved 70 de novo banks since 2017, while nearly 1,000 banks have merged during the same period, including another major bank merger announced just last month.

Hakuna matata. Maybe the commercial banking industry is shrinking because it can no longer serve its customers as effectively as new predator competitors in its territory, such as credit unions and fintechs. Hakuna matata. Maybe that is for the best, but not if the Vice-chair of Supervision and the Secretary of the Treasury have any say.

This month, they pushed to loosen risk-based capital rules for mortgage loans and mortgage servicing rights so the industry can restart the historically unprofitable mortgage lending business, offering borrowers free options to prepay their mortgages at any time. And if they want simpler accounting rules to go along with the easier regulatory rules, hooray for the Financial Accounting Standards Board (FASB), which last November relaxed hedge accounting rules, allowing bank treasurers to use similar risk assessments for cash flow hedges, forecasted transactions, and to designate net written options as eligible hedging instruments.

Supervisors Open the Gates to ILCs and Crypto Trust Banks

Who Elsa might have mated with in her life’s struggles is an open question, but a bigger open question is whether anyone at the FDIC knows what they did last month when they approved applications by Ford and General Motors (GM) to open ILCs. These “banks” exist because of a loophole in banking laws that says that an industrial bank is not a bank, even though it can take deposits insured by the FDIC and grow across state lines without limit. Their only limitation is that they cannot offer demand deposits to the public.

To gain approval, Ford and GM agreed that their new “banks” would maintain a 15% Tier 1 leverage ratio and ensure their safe operation, similar to following the Fed’s source of strength doctrine, a law included in the Dodd-Frank Act that was never officially written into regulations. Setting aside how ILCs combine banking and commerce under a single unregulated umbrella, a taboo since the 1929 Great Crash, and ignoring GM’s shaky history during the Global Financial Crisis, the concerning aspect, according to the Independent Community Bankers Association (IBCA), is that these ILCs pose a risk to the stability of the financial system.

They are the equivalent of the artificial intelligence (AI) monster tech moguls warn is a threat to humanity. Commerce is lining up around the door to get these ILC charters. As ICBA warned, when it urged the FDIC to turn down the charter applications by Ford and General Motors in a comment letter it wrote last November,

“If the FDIC fails to exercise its statutory authority to reject these applications, it will open the floodgates to a new wave of commercial and Big Tech applicants. Walmart and Home Depot have previously sought ILC charters, but the universe of potential applicants is not limited to Big Box stores and automakers. Big Tech companies like Meta, Apple, and X.com have previously made forays into the financial services industry, and it is easy to imagine them seeking an ILC charter to leverage the huge amounts of consumer data they possess. They could use this data to monitor consumer shopping habits and to market predatory credit products to their users.”

There are currently 23 ILCs operating in the U.S., mostly headquartered in Utah, with assets concentrated in just a few institutions. Obtaining charters has been extremely difficult. The last two charters approved by the FDIC were in 2020, and before that, it hadn't approved any since 2006. And for good reason! They could cause chaos if not properly supervised by bank holding companies. No disrespect to the Utah bank examiners, who have exclusive authority over industrial banks in the state with the highest concentration of them. Now, the FDIC is just waving these applications through the door!

If left unchecked, ILCs could roam the banking landscape like herds of elephants across the Serengeti. That’s at least what bank treasurers at commercial banks are concerned about. But the real elephant in the room for banks—more troubling than ILCs—is the rise of cryptocurrencies and the Treasury secretary’s willingness to push forward with integrating them into the banking system.

And if bank treasurers aren’t already upset enough about how the FDIC is allowing commercial businesses to operate banks without following the same bank holding company requirements, they can’t be any happier about the OCC’s decision last month to grant five crypto companies permission to establish trust banks, along with its approval of one more this month for custody, safekeeping, and issuing stablecoins. These approvals come on top of a new notice of proposed rulemaking by the OCC to formally include stablecoin issuance within a trust bank’s fiduciary charter powers.

Trust banks currently are limited to offering the public safekeeping and custody services, which a stablecoin issuer needs to hold the reserves backing the stablecoin. Non-bank cryptocurrency issuers are rushing to establish these services to support their plans to issue stablecoins in compliance with the new GENIUS Act. Many bank treasurers are wary of the permissions the Treasury secretary is granting to crypto companies and the potential that stablecoins could someday replace demand deposits in the public’s savings. But despite the hype, others tell your editor in chief all the time that stablecoins will never take center stage in the payments world, because their use case simply isn't there.

Whether or not stablecoins have a legitimate use case for businesses and consumers, the NCUA published a notice of proposed rulemaking this month that requires credit unions to follow the same rules as banks to establish a permissible payment stablecoin issuer (PPSI). The only challenge is that the Federal Agencies have not finalized the stablecoin PPSI rules under the GENIUS Act, which is a very complex subject, but they are likely focusing on it, given that their deadline to publish the final rules after the comment period ends is July 18, 2026.

The only thing bank treasurers are eager to know is whether stablecoin-issuing bank subsidiaries will be subject to the same rules as commercial banks. Because if not, they will be angrier than a male buffalo you never want to encounter on foot. According to the guide, if you find yourself in that situation, either fall down and let the buffalo break your arms and legs, or climb into a thorny acacia tree. The smartest move your editor-in-chief made on the safari was to stay in the tour’s Toyota Land Cruiser at all times and drink the wine when offered.

Intelligence varies widely on the Serengeti. No offense to warthogs, but they’re not exactly genius-level animals. The warthog’s name in The Lion King was Pumbaa, which means "stupid" in Swahili. Lions aren’t particularly smart either, but they manage to get their fill of warthogs because, when warthogs see a lion coming, they start to run, then forget why they’re running after a minute, stop, and, well, you know…chomp, chomp, yum, yum.

Elephants, by contrast, might lumber around a lot and, because they are larger and have thick skins, do not worry much about lions. But they have super good memories, like bank treasurers. They are not territorial; they march everywhere across the Serengeti, wherever they please. But did you know that if an elephant dies somewhere, all the other elephants will avoid that spot afterwards, and even years later, will not forget its location?

Hawk, Dove, or Something Else?

They are herbivores, unlike lions, so you don't need to worry about being eaten by one, although being stomped on by a lumbering Babar remains a real possibility. Their main threat to the Serengeti and its ecosystem is stripping bark from trees, killing them, and harming the birds that nest in them. The Serengeti, if our subscribers aren't aware, is home to over 540 bird species, including unique ones like the Lilac-breasted Roller and the Secretary Bird, which are found nowhere else on Earth. There are flamingos. There's even a bird your guide calls the bare-faced go-away bird because it makes a sound when you walk near it that sounds a lot like it is telling you to go away—like your boss when you ask for a bigger budget for your department. Truly, the Serengeti is an inviting paradise for birders.

Rest assured, your editor in chief focused a lot on taking pictures of the hawks and doves, which come in a fair number of varieties. There is the African harrier hawk, the dark chanting goshawk, the little sparrow hawk, and the black sparrow hawk, and those are only a few of the ones his guide pointed out on the game drives. With doves, you’ve got the mourning-collared doves, the red-eyed doves, and your laughing doves, but try not laughing at the futility of telling any of them apart.

It takes a discerning eye to note any distinctive colorings and features in your binoculars before the darn things fly away. Try as he might to use binoculars to tell the difference between hawks and doves, he often had to take the guide’s word for it that the two birds that looked like doves that were hanging out on the rhino and buffalo were actually just cattle egrets, not doves. Equally hopeless was telling the difference between a dusky turtle-dove and a plain old rock pigeon.

While your editor in chief tried to snap a picture of one of these birds that the guide was pointing out before it flew away, bank treasurers back home must have been fumbling to identify Kevin Warsh’s bird species. The popular question these days is whether he is a hawk or a dove. The likely answer is neither. He is a different species altogether, one that thrives in the political realm and straddles the financial world, a world where it is possible to be both hawk and dove at the same time, and say things that sound one way and can mean another.

The President’s nominee to become the 17thchair of the Federal Reserve this May is a politician, which is not much different from the man he aims to replace—himself, a lawyer but not a PhD economist. He will need all his political skills just to get through the confirmation process. Senator Tom Tillis, who chairs the Senate Banking Committee, has placed a hold on his nomination, protesting the President’s Department of Justice and its criminal investigation into Chair Powell and the refurbishment of the Fed’s headquarters to pressure the Fed to cut rates.

Kevin Warsh Has Always Said He Is Independent

Asked this month what he thought about the Fed’s independence and the President’s pressure campaign, the Treasury Secretary, who backs Warsh’s nomination, blamed the Fed’s bad decisions for its own troubles,

"The Federal Reserve should be independent for monetary policy, and every other program it undertakes impinges on the monetary policy independence — whether it is cost overruns on a building, whether it is including the climate, or whether it is offering political opinion.”

What do bank treasurers know about Kevin Warsh? Well, when he served on the Fed’s Board of Governors during the GFC, he presented himself as a strong advocate for its independence, as he told the Shadow Open Market Banking Committee in November 2010 in a speech titled “Ode to Independence.”

“The Fed's greatest asset is its institutional credibility. This institutional credibility is rooted in its inflation-fighting credibility, but it is broader still. It is tied up in the full range of Fed actions and balance sheet commitments. This credibility is essential. It adds heft to our communications. It gives weight to our economic assessments. It amplifies the effect of announced changes in the short-term policy rate on longer-term rates. It is, in some sense, the real money multiplier in the conduct of policy.”

And if the Fed loses that credibility and, for example, relaxes its commitment to fight inflation and cuts interest rates when not justified by the fundamentals; if it allows inflation to erode the value of outstanding debt or reduces rates to help the government fund its debt at a lower cost, it might temporarily improve the country’s economic situation, but the long-term damage would be severe. As he continued,

“Governments may be tempted to influence the central bank to keep monetary policy looser longer to finance the debt and stimulate activity. In the more static short run, the real burdens of nominal debt could be reduced by higher inflation. The consequences just over the horizon, however, would be most unwelcome. Higher expected inflation would lead to higher nominal interest rates, further increasing the government’s financing needs. Moreover, higher expected inflation could lead to more variable inflation outcomes and reduced living standards, especially for those least able to protect themselves from unexpected price movements.”

Warsh says he will stay independent if nominated, no matter if the President who nominated him disagrees about the direction of interest rates. If rates need to go up, they will; if they need to go down, they will. It doesn't matter to him what the President wants. Independence is essential for a central bank to do its job. As he mentioned during an interview with the media last summer,

“I’ve strongly believed for 20 years, and history tells us, that independent conduct of monetary policy is essential."

Which is not exactly the same as saying he would not listen to instructions from the White House, displaying some of the political finesse he'll need in the role. Earlier this month, when the President sat down for an interview with NBC, he said he was very confident that interest rates would decrease soon. The interviewer asked him if he would have nominated Kevin Warsh if he had said he wanted to raise interest rates this year. But the President was definitive.

“If he came in and said, ‘I want to raise them,’…he would not have gotten the job. No.”

Which sounds a lot like the President has a fairly specific idea about how independent the Fed should be. But Warsh insisted he was no patsy in an interview last November, saying there are times when a central banker needs to be a dove and times when he needs to be a hawk, and that it all depends on the circumstances.

“I have a track record going back 20 years…There's a time for a bird to change its feathers, and it's with the times. It has nothing to do with this president.”

How will he lead the Fed to cut rates when inflation is still running above the Fed’s 2% target, and the economic indicators are still ambiguous about growth? The answer is AI. AI will drive productivity growth and address inflation issues. As he wrote last November,

“AI will be a significant disinflationary force, increasing productivity and bolstering American competitiveness. Productivity improvements should drive significant increases in real take-home wages. A 1-percentage-point increase in annual productivity growth would double standards of living within a single generation.”

Which sounds fantastic, provided AI does not damage employment in the short term, which is a serious concern to economists working at the reconstructed Eccles Building, as Fed Governor and former Vice-chair of Supervision Michael Barr wrote this month. But in the longer run, Kevin Warsh is forward-looking, aligning well with Fed Governor Miran’s advice to him, as he said this month at the Dallas Fed.

"Be forward-looking, not backward-looking. If you’re going to be excessively backward-looking, you’re guaranteed to be behind the curve.”

Fed Balance Sheet Size is the Issue

The nominee has a nuanced view of the Fed’s balance sheet, meaning he opposes it but cannot do much to change it, at least before his term ends in four years. During the GFC, when he was a Fed Governor, he supported quantitative easing in 2008 and 2009 but turned against the program when the Fed continued to grow its SOMA portfolio in 2010. It was not that he disapproved of the Fed’s use of the balance sheet to address a crisis.

Rather, he was and remains against continuing with crisis-era remedies long after the crisis passes. By 2010, the economy was recovering from the Great Recession, and the crisis was over as far as he was concerned. Consequently, as he said in a speech at a SIFMA conference in November 2010, called “Rejecting the Requiem,”

“By my way of thinking, the risk-reward ratio for Fed action peaks in times of crisis when it has a full toolbox and markets are functioning poorly. But when non-traditional tools are needed to loosen policy and markets are functioning more or less normally…the risk-reward ratio for policy action is decidedly less favorable. In my view, these risks increase with the size of the Federal Reserve's balance sheet.”

He still opposes a large balance sheet today, as he wrote last November in an opinion piece in the Wall Street Journal.

“The Fed’s bloated balance sheet, designed to support the biggest firms in a bygone crisis era, can be reduced significantly. That largesse can be redeployed through lower interest rates to support households and small- and medium-sized businesses.”

He also had a skeptical view of government stimulus, calling government checks short-term fixes for bigger issues, like when outstanding Treasurys totaled $14 trillion—less than half of what it is today. As he stated in his November 2010 speech, he didn't want to take away the proverbial punchbowl; instead, he argued that what’s in it isn’t good for the economy in the long run. There must be a third way, a better way.

“Fiscal authorities should resist the temptation to continually increase government expenditures to compensate for shortfalls in private consumption and investment. A strict economic diet of fiscal austerity has greater appeal, a kind of penance owed for the excesses of the past. But, in my view, root canal economics does not constitute optimal economic policy. The United States would be better off with a third way: pro-growth economic policy.”

Some hakuna matata was needed during the GFC. Failures, bankruptcies that put people out of work and on the street, and devastating losses are all part of the circle of life, and the phoenix will rise from the ashes. You can just hear the song as he talks…

“It's the circle of life, and it moves us all through despair and hope through faith and love, 'til we find our place, on the path unwinding in the circle of liiiiiiiiiiiiife!”

Hakuna matata, as he continued,

“Deleveraging by our household and business sectors is not a pattern to be arrested, but good prudence to be celebrated…The steep correction in housing markets, while painful, lays the foundation for recovery--far better than the countless programs that sought to subsidize and temporize the inevitable repricing. It is these transitions in our market economy--and the adoption of pro-growth fiscal, regulatory, and trade policies--that lay the essential groundwork for greater, more sustainable prosperity.”

Indeed, the Fed’s large balance sheet, which at $6.6 trillion is no longer shrinking through quantitative tightening and has started to grow as shown in this month’s chart deck, is the problem, the anchor holding back the economy and the bright future he envisions. Interviewed last summer, he said that the Fed’s large balance sheet is holding back economic growth.

“Economic growth in the U.S. is poised to boom, but it’s being held down by bad economic policies coming from the central bank. Interest rates should be lower. The balance sheet should be smaller.”

While he generally prefers a smaller balance sheet, his ability to reduce it is limited because balance sheets follow basic arithmetic: assets must equal liabilities. The Fed’s SOMA portfolio, on the asset side—the left—totaling $6.3 trillion. On the liability side—the right—there is $2.4 trillion in printed currency, half of which is held in vaults outside the U.S., the Treasury’s $0.9 trillion checking account, and bank reserve deposits just under $3.0 trillion.

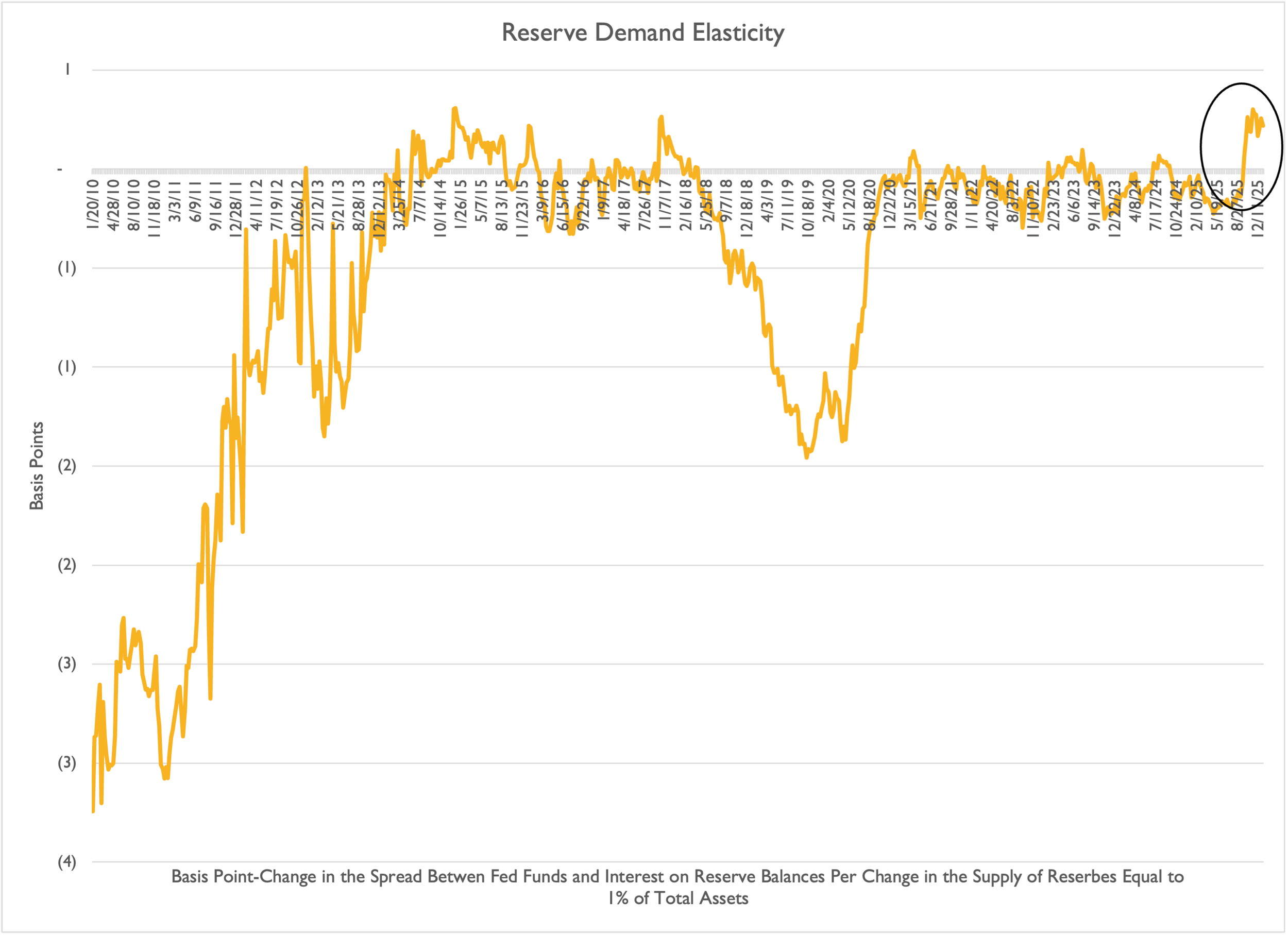

He can favor a smaller balance sheet, but the Fed has no control over currency in circulation or over how much money the Treasury leaves in its checking account. This leaves the reserve balance, which is basically unchanged since June 2022, when the Fed began shrinking its total assets, which had topped $9.0 trillion. Reserves are the lifeblood of the financial system, and the Fed’s institutional thinking is that by keeping the balance of reserves at a level it describes as at least “ample,” which is a hypothetical level between abundant and adequate, the Fed can control market volatility to the benefit of Treasury issuance.

The New York Fed publishes a regular reserve balance analysis that it believes demonstrates that reserves are indeed abundant, with a measure it calls reserve demand elasticity (Figure 2). The measure compares changes in the effective Fed funds rate to changes in the balance of reserves, and shows the generally calming effect on markets since 2019, when the Fed adopted the policy. The smooth operation of the Treasury repo market is especially sensitive to the supply of reserves in the system. The latest blip in the measure since the new year supports the Fed’s economists, who now argue that reserve balances should not go any lower.

Figure 2: Reserve Demand Elasticity

Demands on reserves will likely increase when the SEC’s new clearing mandate for Treasury trading and repos takes effect next year, requiring all Treasury securities and repo transactions to clear through a central counterparty. The goal is to improve risk management and settlement processes in the Treasury security and repo markets. However, it could reduce liquidity by undermining the economics of the Treasury basis trade.

In a basis trade, market participants take a position in a futures contract and an underlying deliverable security, and use the repo market to finance the cash leg. The trade creates demand for the cheapest-to-deliver securities, which are typically off-the-run, thereby boosting liquidity in the broader Treasury market. However, margin requirements from the futures exchange, the Fixed Income Clearing Corp (FICC), and other central counterparties could end up tripling collateral requirements and discourage market participation unless the clearers adopt cross-margining for similar risk positions.

Shrinking reserves is not a viable option, especially now, when primary dealer balance sheets are already strained by the increasing debt supply, due to last year’s hike in the debt ceiling from $36 trillion to $41 trillion. Even with the capital relief the Fed provided to global banks under the enhanced Supplementary Leverage Ratio last year, which was intended to encourage them to hold more Treasurys, dealer banks still face liquidity limits imposed by the Basel 3 Net Stable Funding Ratio and the Liquidity Coverage Ratio. Even if these regulations were loosened, global banks would still be limited by stress testing; the latest scenarios the Fed released this month continued to factor in market shocks in their capital adequacy assessments.

But capacity constraints on dealer balance sheets only become clear during a crisis, as discussed in a 2024 Fed study. Fear disrupts many well-balanced systems. For instance, if the FICC or another major clearinghouse came under stress, the ripple effects would likely strongly impact the Treasury market, highlighting how the Fed nominee’s goal to shrink the balance sheet ignores some basic, harsh realities. There's no going back, and the balance sheet is the balance sheet.

Politically speaking, when you can't actually do something, the next best approach is to keep talking about doing it anyway. The laws of arithmetic and accounting don't leave much room to cut, and the fiscal mess will require a marginal buyer to step in—likely the Fed. However, the Fed nominee and former Fed Governor insists on working toward shrinking the balance sheet someday, in time.

“There needs to be an exit plan to get the Fed out of the fiscal business, to give powers back to Secretary Bessent. But it can't be done in a rushed way.”

And he didn't hold back, either, blaming the Fed chair and the other current voting members of the FOMC for putting the financial system in the mess it's in. They need to be fired, he told an interviewer last fall. There needs to be a regime change.

“The credibility deficit lies with the incumbents who are at the Fed, in my view…Their hesitancy to cut rates, I think, is actually ... quite a mark against them…The specter of the miss they made on inflation, it has stuck with them. So one of the reasons why the President, I think, is right to be pushing the Fed publicly is we need regime change in the conduct of policy.”

Exactly! Warsh has famously proposed a new Treasury “Accord” similar to the one the Fed and the Treasury crafted in 1951 during the Truman administration. As the previous newsletter noted, before that agreement, the Fed was controlled by the Treasury and could not independently raise interest rates, even if then-Fed chair McCabe wanted to do so to combat rising inflation. That accord forms the foundation of the Fed’s current independence.

But here is a question for the nominee, and this business with the Treasury accord he is pushing. If the Fed is already independent and can set rates as it wants, what would a new accord look like? One where it is not independent? The Fed chair nominee seemed to suggest, misleadingly, that the Fed was working at cross-purposes with the Treasury before the 1951 accord. But how can that be if the Treasury was forcing it to hold long-term rates below 2.5%? And why would Treasury ever be aligned with higher interest rates for its debt issuance if that were needed?

“We need a new Treasury-Fed accord, as we did in 1951, after another period where we built up our nation’s debt, and we were stuck with a central bank that was working at cross purposes with the Treasury. That’s the state of things now…So, if we have a new accord, then the Fed chair and the Treasury secretary can describe to markets plainly and with deliberation this is our objective for the size of the Fed’s balance sheet.”

For the record, the Fed only controls overnight interest rates, and it takes leadership and credibility to get the rest of the market to align the yield curve in the same direction. When the Fed cut 100 basis points from the Fed funds rate in Q4 2024, the entire back end of the yield curve rose, unlike every previous rate-cutting cycle going back to Alan Greenspan’s days as Fed chair.

And whatever objective the Fed and the Treasury have regarding the Fed’s balance sheet, it certainly won’t be clear to market participants, who see a wave of debt issuance ahead and little interest in buying unless higher rates are offered. It’s basic accounting: money has to come from somewhere, and the Federal Reserve is a convenient buyer of bonds to help keep interest rates low, aligning with what the President, Secretary of the Treasury, and the nominee seem to want.

Ode to Game Wardens and Bank Examiners

You learn to appreciate the game wardens on the safari. They are there to prevent animal poaching. They track the animals, making sure the elephants are in their designated spots and not busy eating tree bark, and they have cameras set up everywhere to monitor baby wildebeests or zebras that have lost their mothers. They also manage tourism and establish reasonable, transparent rules, such as that you cannot go on a game drive at night unless you're on one of the privately owned and managed conservancies on the Serengeti. Otherwise, they will assume you are a poacher and fine you a large amount of USD cash.

The game wardens have a tough job, given that they need to monitor the Serengeti, which spans 12,000 square miles. If only bank examiners had it that straightforward. Because Kevin Warsh and Miki Bowman believe they are lost in trivial details, so much so that they cannot see through to an institution’s core risks. That is their explanation for the bank failures three years from now, next month. Examiners are so caught up in minor issues that they can miss the elephant in the room, if not miss the forest for the trees.

One word defines the Vice-chair of supervision’s approach to bank examinations—"materiality." Bank supervision today, she said in a speech this month, is distracted from what really matters.

“…the approach to supervision has led to a world in which core financial risks have been de-prioritized, and non-core and non-financial risks—things like IT, operational risk, management, risk management, internal controls, and governance—have been over-emphasized. These issues are important, and certainly worthwhile topics for examiners to consider, but their review should not come at the expense of more material financial risk considerations—and they should not drive the overall assessment of a firm's condition.”

The President’s nominee for Fed chair agrees completely. Bank supervisors should avoid overwhelming bank treasurers with too many details. Yes, details matter, but the main point is that rules shouldn't hinder growth. This probably was his thinking as a Fed governor in 2010—that banks, even large ones, need to fail.

“Pro-growth policies also demand reform in the conduct of regulatory policy. It would provide more timely, clear, and consistent rules so that firms — financial and otherwise — could innovate in a changing economic landscape. It would allow firms to succeed or fail. It would not protect the privileged perch of incumbent firms--no matter their size or scope--at the expense of their smaller, more dynamic competitors. Regulators would be hostile to rent-seeking by the established. And hospitable to the companies whose names we do not know.”

Out with the bad, in with the good, whether we are talking about bad banks that should have been closed long before they failed, or we are talking about poor supervisory practices that hinder preventing bad banks from costing taxpayers money to clean up. Kevin Warsh and Miki Bowman no doubt appreciate their upcoming task. They understand why bank supervision is a lot like a termite mound.

Dotting the Serengeti, termites build mounds towering several feet in the air, which also descend as much as 30 feet underground. Dealing with reforming a system like supervision, a complicated edifice thanks to different regulators with overlapping responsibilities, will require more work than simply writing new rules. They will need to go root and branch if their reforms have any hope of scratching the surface of the issues the bank supervisory agencies face, including even finding people to fill critical roles in bank exams.

But Kevin Warsh wants to go further than just reforming bank supervision. He wants to tear up Basel, an international accord under the auspices of the Bank for International Settlements, which the U.S. created after World War I and is headquartered in Basel, Switzerland. Central bankers joined together for the express purpose of creating a level playing field for banks operating across the globe. It has been in place since 1988, when Basel 1 was published.

The large banks may face issues with excessive capital and liquidity requirements, but they fundamentally want the level playing field established by the Basel Accord nearly 40 years ago. No, if the Fed nominee is anything, he is an iconoclast. In his view today, the U.S. banking industry does not need an Endgame; it needs its own new game, writing in the WSJ last November that,

“…the Fed under Janet Yellen and Mr. Powell has spent more than a decade negotiating bank regulatory and supervisory standards with its global counterparts in Basel, Switzerland. Fed leaders have tried to bind U.S. banks to a complicated, vaunted set of rules in the name of global regulatory convergence. In my view, the Basel Endgame isn’t America’s endgame. A new, reformed American regulatory regime should make the U.S. the best place for the world’s banks to do business. That would spur new lending here at home.”

Hakuna Matata

While many of our bank treasury subscribers were attending the annual “Acquire or Be Acquired” infomercial conference in Phoenix, Arizona, this month, your editor in chief was watching eat or be eaten in action. Remember the baby wildebeest that got separated from its mama and then ended up as dinner for a cheetah? The story is very sad.

The cheetah that caught it was only 1-1.5 years old, according to the guide. Its mother was literally hanging out in a tree branch nearby, and the “child” cheetah was showing off to its mother that it could fend for itself, running down its prey. But by that point, the entire wildebeest herd had run off, including the baby’s mother, who was not interested in finding out if her baby was an appetizer and she could be an entrée. Understandably, she probably did not want to watch it get torn limb from bloody limb.

Fortunately or unfortunately, depending on your perspective from the baby wildebeest and the cheetah, the cheetah’s jaws were not strong enough to choke and kill the wildebeest. So, after trying to choke it to death for what seemed to your editor-in-chief another great opportunity to check markets, trying to drown out those plaintive cries, it suddenly let go of the poor animal and ran back to its mother.

And then the drama, because you see the wildebeest struggling to its feet, stumbling away from what should have been its violent end. Unfortunately, as the guide explained, it will still die, alone and abandoned by its mother, who probably forgot it even existed. Unable to digest the grass without its mother’s help, it will be dead by the morning, by which point the hyenas and the jackals would have finished whatever was left. Hopefully, that is not the fate for community banks. Hakuna matata.

The Bank Treasury Newsletter is an independent publication that welcomes comments, suggestions, and constructive criticisms from our readers in lieu of payment. Please refer this letter to members of your staff or your peers who would benefit from receiving it, and if you haven’t yet, subscribe here.

Copyright 2026, The Bank Treasury Newsletter, All Rights Reserved.

Ethan M. Heisler, CFA

Editor-in-Chief

This Month’s Chart Deck

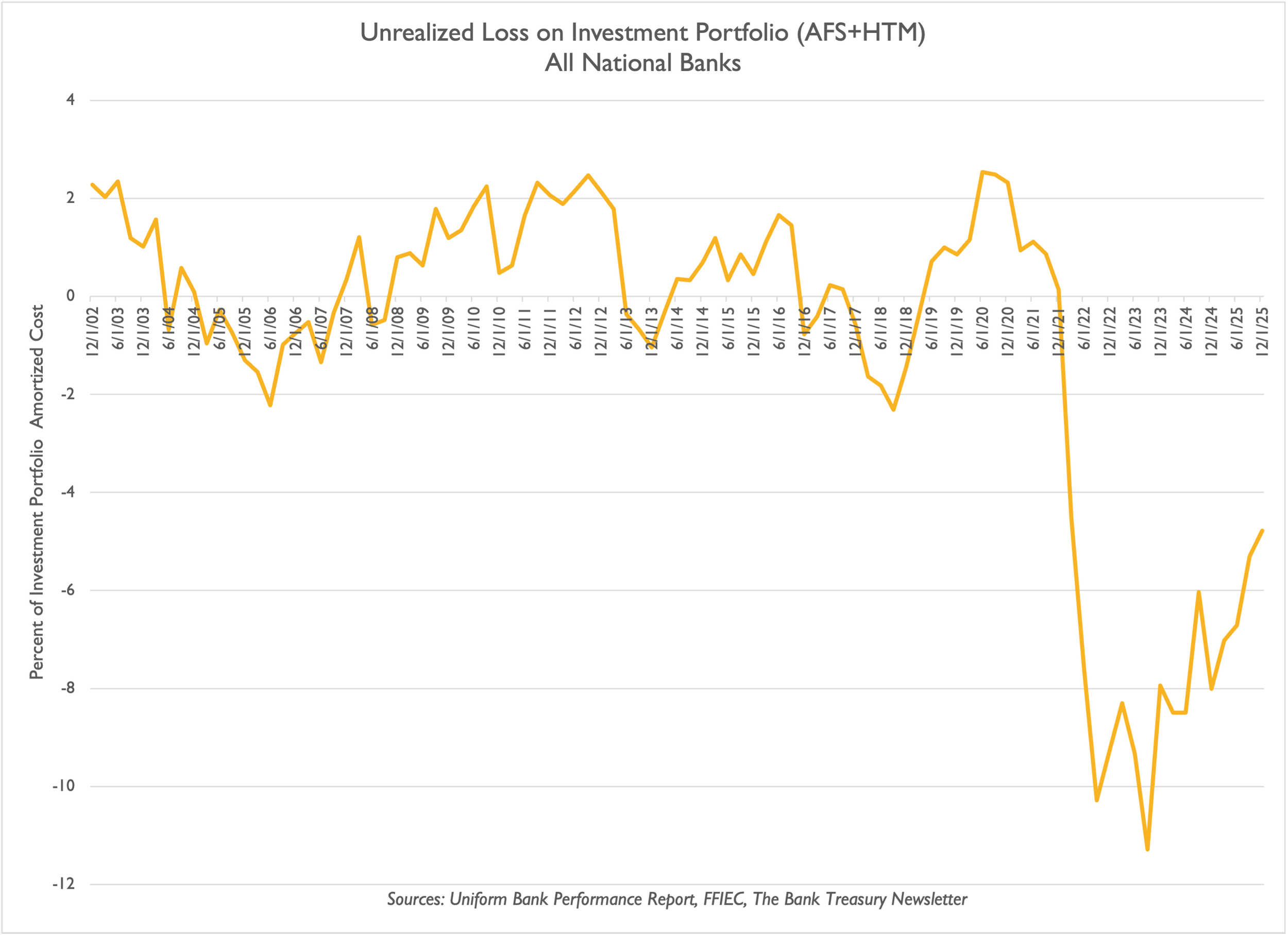

Metropolitan Bank and Trust last month became the first bank of the year to fail, and at the end of last year, reported that unrealized losses in its available-for-sale (AFS) portfolio (the bank did not hold any bonds in held-to-maturity (HTM)) exceeded 100% of its Tier 1 capital. As highlighted in this month’s newsletter, there are 23 banks with total assets under $10 billion that have unrealized market losses in their bond portfolios exceeding 30% of their regulatory capital. However, the first slide in this month’s chart deck shows that the industry continues to climb out of the negative accumulated other comprehensive income hole they fell into three years ago when the Fed went hard and fast, raising interest rates, which caused Silicon Valley Bank to fail.

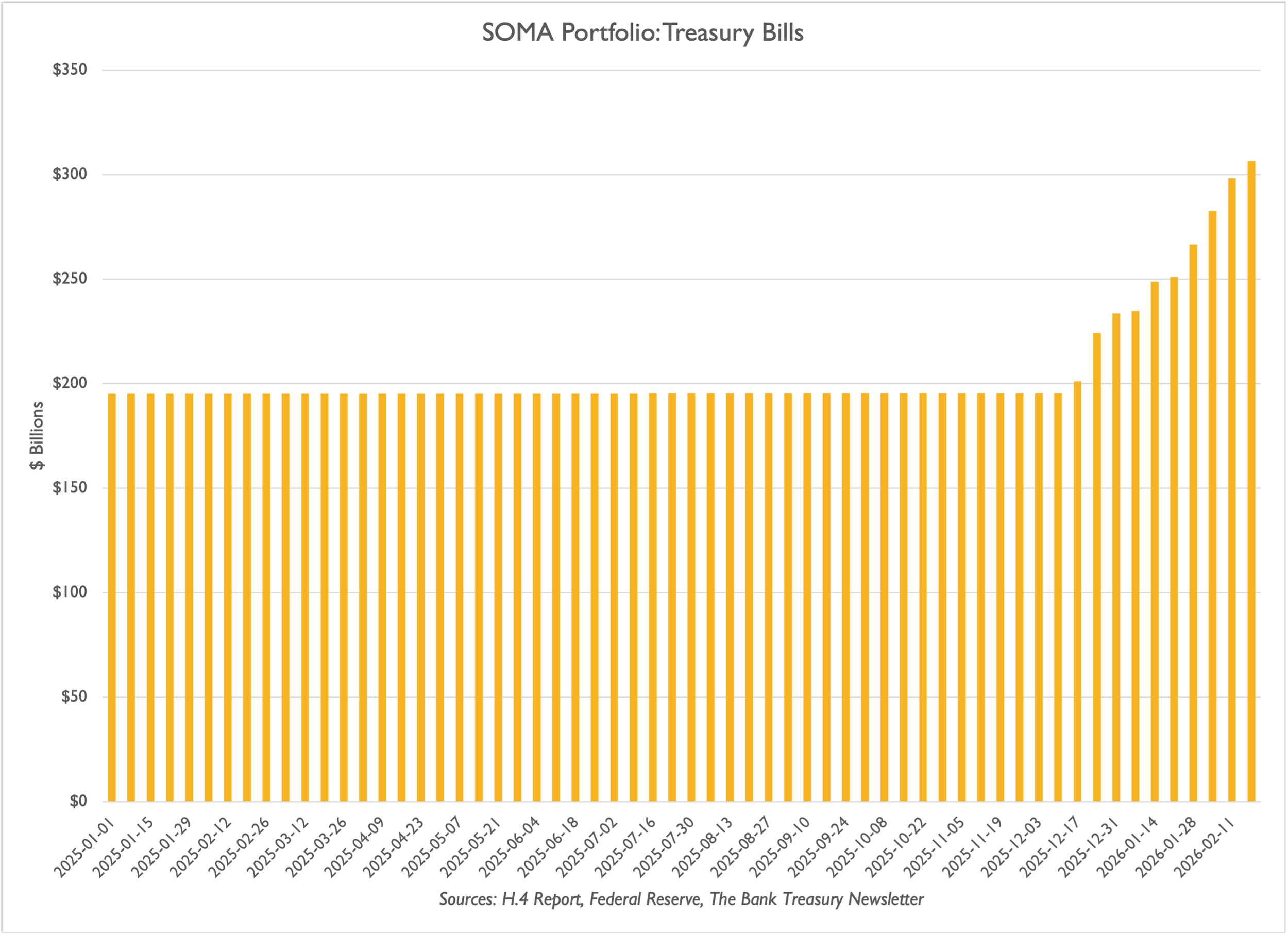

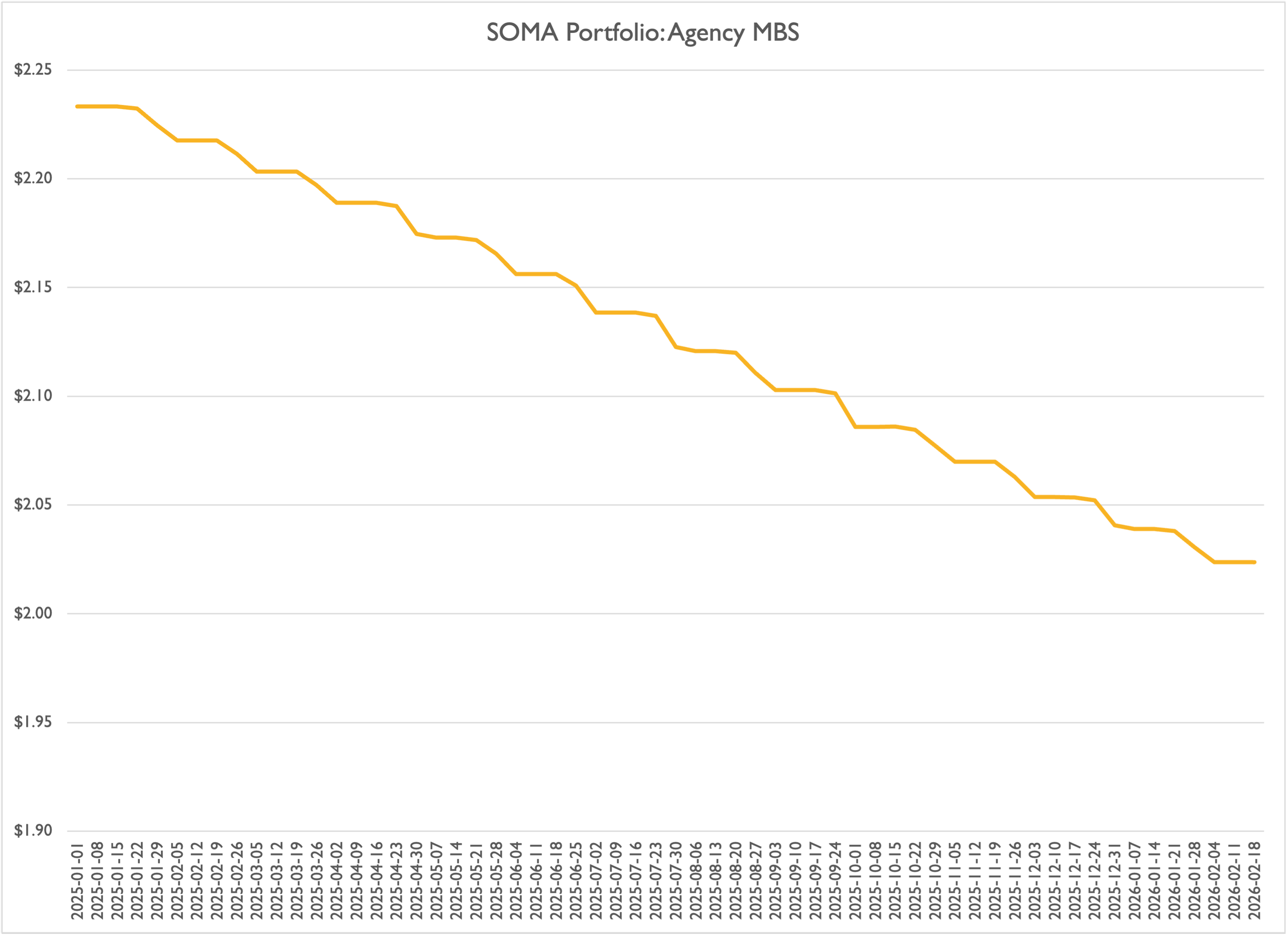

Former Fed governor Kevin Warsh, the President's nominee to chair the Fed, is not a fan of the Fed's balance sheet size and has suggested he would work toward a new Treasury Accord to reduce it. However, the balance sheet today leaves little room for shrinking it. Indeed, its System Open Market Account (SOMA) portfolio began growing again this year (Slide 2), driven by the Fed's decision to expand its holdings of Treasury Bills (Slide 3), which is offsetting the run-off from its Agency MBS holdings (Slide 4).

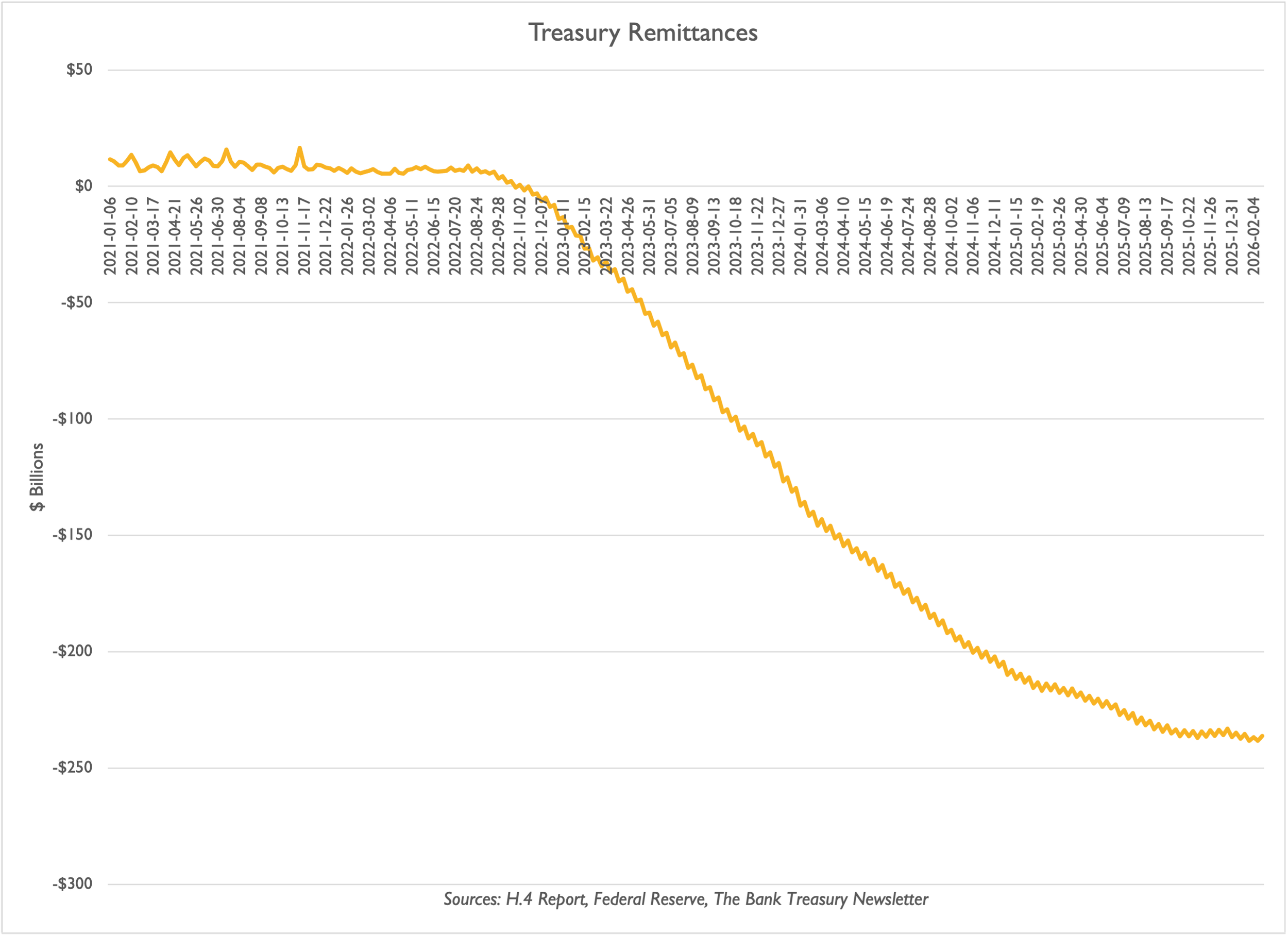

But even if the Fed were not rebuilding its SOMA portfolio by buying Treasurys, the composition of its liabilities would leave it with little room to reduce assets because the liabilities that balance its $6.3 trillion SOMA portfolio include currency in circulation (Slide 5), which this year surpassed $2.4 trillion. Over the past 15 years, since Kevin Warsh resigned as a Fed governor, the average balance in the Treasury's "checking" account at the Fed (Treasury General Account (TGA)) has grown from less than $100 billion to surpassing $900 billion this month (Slide 6). It still earns less on its SOMA portfolio than it pays interest to banks for their reserve deposits, which cumulatively added nearly $240 billion to reserve deposits (Slide 7) through negative Treasury remittances. Even with the offset, higher-trending balances in the Treasury's TGA account, especially over the last six months, explain why reserve deposits (Slide 8) are down since the summer to their lowest level since the Fed began quantitative tightening in June 2023.

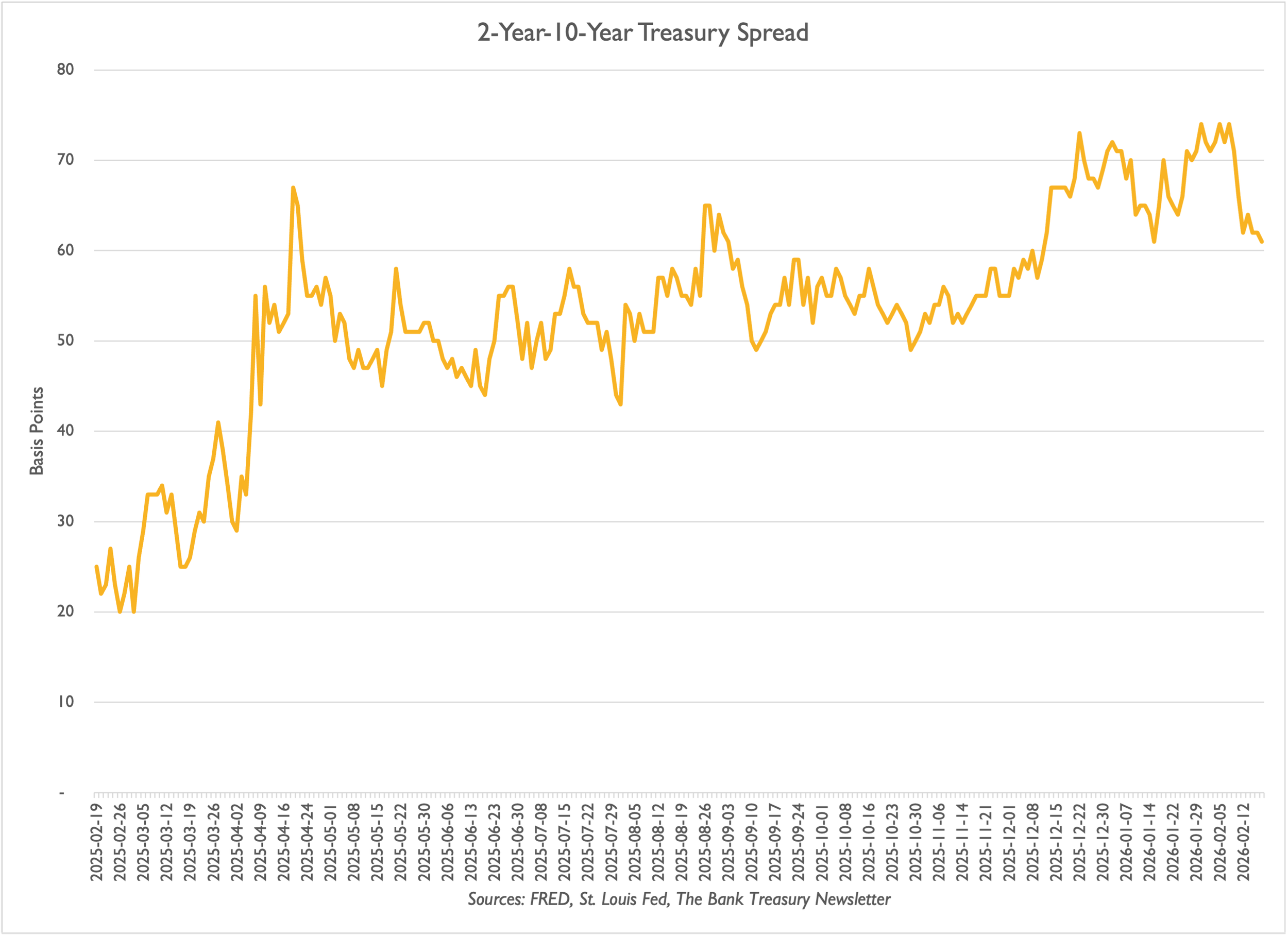

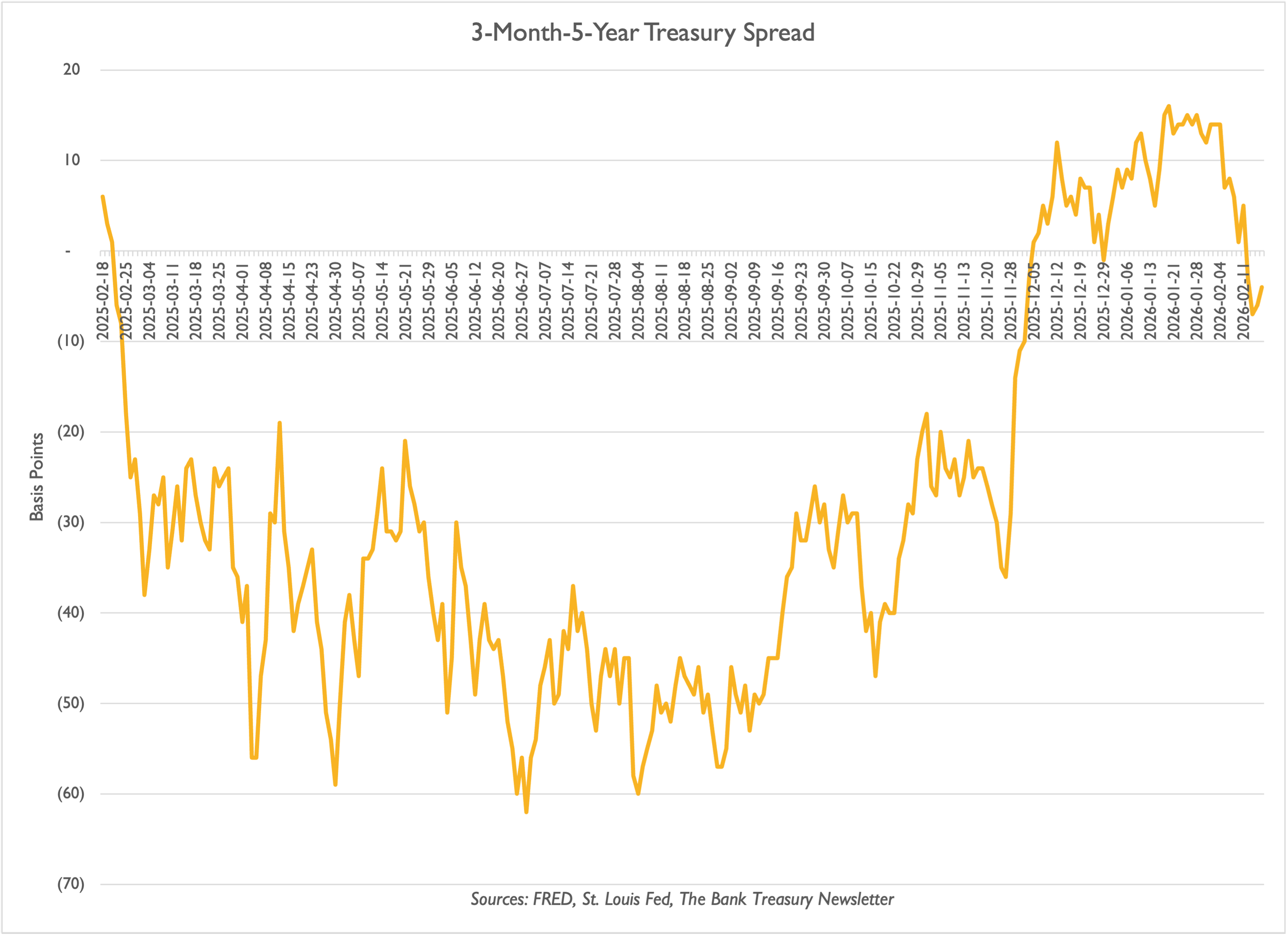

Economic weakness and persistent inflation above the Fed’s 2% target are keeping bank treasurers confused about the direction of interest rates. While initially steepening at the beginning of last year, the 2s-10s spread has remained locked in a narrow range around 60 basis points for most of the past year (Slide 9) as market participants try to divine the future path of interest rates. In contrast to the positively, yet modestly, sloped 2s-10s curve, the 3-month-5-year curve spread began the year flat, then immediately inverted and remained so up until December, when it turned briefly and became barely positive, hitting 10 basis points before falling back into negative territory again this month.

Long Climb Left To Get Out Of Negative AOCI

QE3?

Fed Ramps Up Its T-Bill Holdings

T-Bills Are Replacing Agency MBS Run-Off

Basic Accounting: Higher Cash = Higher SOMA

Treasury Is Holding More Cash In Checking

Negative Remittances Add To Reserve Deposits

TGA Puts Downward Pressure On Reserves

Interest Rate Uncertainty Flattens 2s-10s

3-Month-5-Year Back To Inverted Territory