BANK TREASURERS TELL NO TAILS!

The U.S. Senate confirmed Kevin Warsh as the Fed’s 17th chair, succeeding Jerome Powell, who will remain a Fed Governor and a voting member of the Federal Open Market Committee (FOMC) until his term ends in January 2028 or sooner. Powell also briefly held the position this month as “interim chair pro tempore” after Warsh’s confirmation, until Warsh was sworn in later in the month. In addition to his predecessor, Warsh joins a seven-member Board of Governors, which includes Chris Waller, who had been a competitor for Warsh’s new seat as chair; Michael Barr, the former Vice-Chair of Supervision and a continued advocate for tighter bank supervision; Michelle Bowman, Barr’s successor, who is leading the charge to loosen supervision; the embattled Lisa Cook, whom the President is trying to fire; and Clinton Jefferson, the Vice-Chair of the Fed.

No fan of forward guidance, and having vowed to end it, Kevin Warsh is likely to find that market participants long ago learned to discount its reliability as a predictor of where the economy or interest rates are headed, and that they probably will not miss it anyway if he follows through during his tenure as Fed chair and ends the practice. He is also no fan of the Fed’s $6.7 trillion balance sheet and vowed to shrink it. But to shrink the balance sheet, he will need to either get the Treasury to leave its $800 billion Treasury General Account with banks or with money market funds, somehow eliminate currency in circulation, half of which is held by foreigners outside the United States, or address the Fed’s current ample reserve policy.

He may find that it is much easier to adopt such a policy, which today means holding $3.1 trillion in reserve deposits on its balance sheet, than to return to the way it was before the policy’s adoption; that, short of making significant changes to the definition of a High-Quality Liquid Asset that equates a short-term T-Bill with a reserve deposit at the Fed, or including an undrawn line at the Fed’s discount window as a liquid asset, it is going to be very hard to get the financial industry to want less reserve deposits when they are the most liquid asset in the financial system.

Sock puppet or not, what Kevin Warsh and the FOMC decide to do about overnight interest rates may have little sway with bond investors (both here and abroad) who are short at all points beyond the overnight term. The yield on a 10-Year Treasury, for example, is up 60 basis points since the beginning of the year, to 4.6%. The 30-Year Treasury is over 5%, the highest in 20 years. Convincing them that the Fed under his chairmanship remains a credible anchor for the rest of the financial system will be tested this summer as higher oil prices filter through the economy and push up inflation, while the labor force is under pressure from job cuts, inflation, and the threat that artificial intelligence poses to the ranks of new hires. Meanwhile, the equity markets continue to hold at or near record highs, seemingly ignoring the danger of wealth destruction posed by global macro, fiscal, political, and economic developments.

In addition to confirming Kevin Warsh as Fed Chair, the Senate Banking Committee reached a compromise to move its version of the Clarity Act forward for a full Senate vote. Along with the GENIUS Act, passed last year, this legislation will support the legal integration of cryptocurrencies into the financial system. Despite opposition from banking lobbyists, the Senate’s draft of the Clarity Act slightly opens the door for nonbank stablecoin issuers to offer discounts instead of interest, which the GENIUS Act bans. While stablecoins are often seen as a way to off-ramp from crypto trading, their main potential for the banking industry is in payments. Currently, less than 1% of the $300 billion in stablecoins is used for payments, and a major challenge for the industry is creating a system where stablecoins are as reliable as traditional currency—serving both as a means of payment and a store of value.

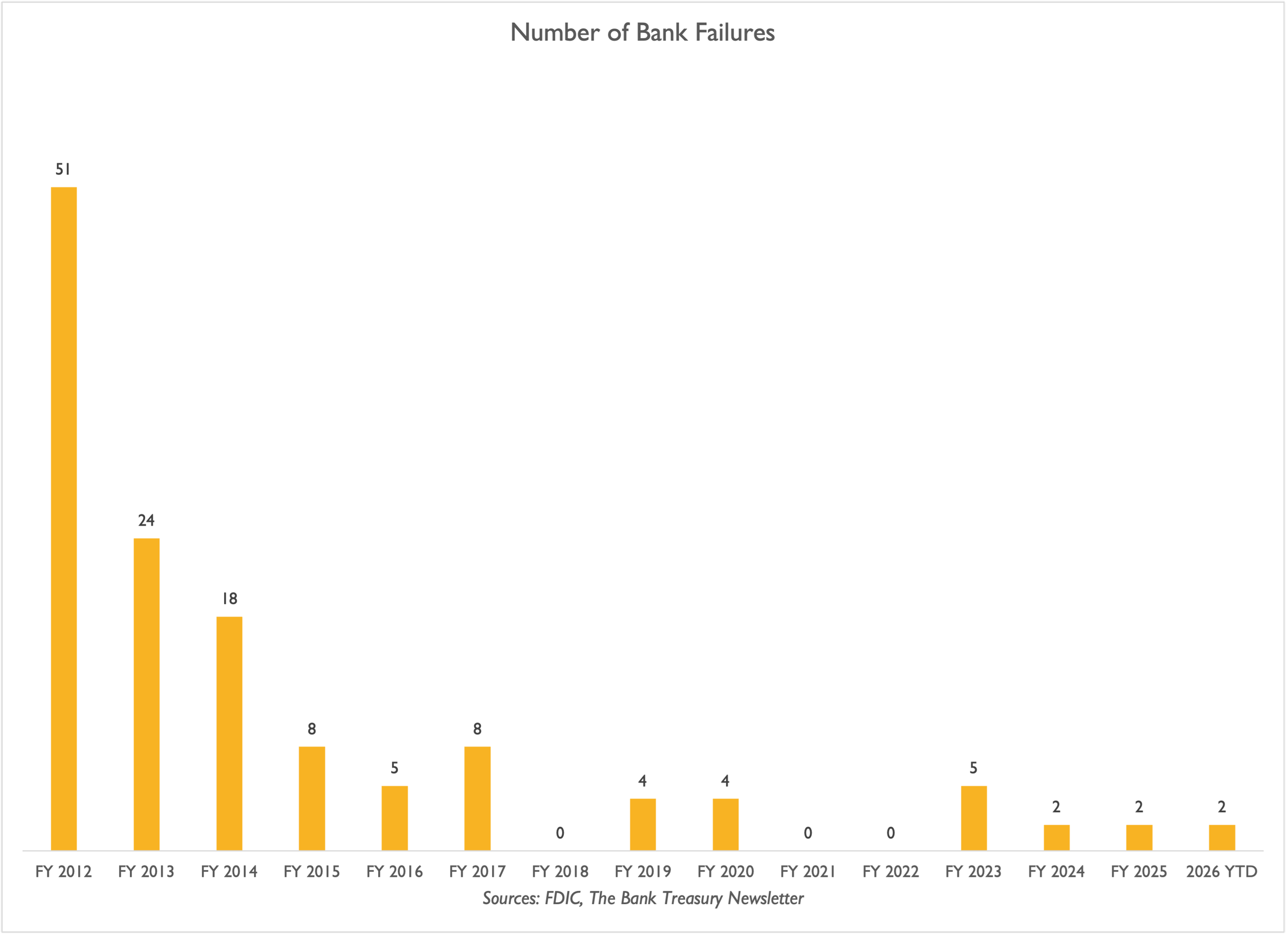

This month, the FDIC closed Community Bank and Trust-West Georgia (WBT), marking the second bank failure this year after Metropolitan Capital Bank (MCB) failed earlier in January. Both were small, with assets under $300 million—CBT had $288 million—and their failure was expected to cost the Deposit Insurance Fund (DIF) more than $100 million, even after asset sales. The bank suffered sudden, severe losses in its agricultural loan portfolio. Uninsured depositors are awaiting some recovery as assets are sold. The failure cost exceeds five times that of Metropolitan Capital Bank, making it the largest asset-related write-off since the financial crisis, when IndyMac Bank collapsed. Despite hearings over the past year, Congress has not yet enacted legislation to raise the deposit insurance cap, which was last set at $250,000 in 2010. Meanwhile, regulators proposed increasing the resolution planning threshold—living wills—from $250 billion to $700 billion, a level last adjusted in 2018.

So far this year, Congress has not enacted legislation to raise the deposit insurance limit, which has remained at $250,000 since 2010. Meanwhile, regulators suggested increasing the resolution planning threshold—living wills—from $250 billion to $700 billion, a level last changed in 2018. Additionally, the House approved the “Community Bank Deposit Access Act,” which would prevent custodial deposits from being classified as brokered deposits, provided they do not constitute more than 20% of an institution's liabilities and the bank remains in satisfactory financial condition.

The Bank Treasury Newsletter

Dear Bank Treasury Subscribers,

Janet: Hello, everyone. My name is Janet, and I am pleased to host today’s episode of the Bank Treasury Newsletter’s Cold Case Murder Mystery series. I have long wanted to do an episode like this, and I think the newsletter’s subscribers are in for a treat. Stay with me until the end for the ultimate surprise twist.

Now, before we begin, the newsletter’s legal team asked me to remind our listeners that, technically, I am a fictional character created by artificial intelligence (A.I.), even though I sound real and may or may not resemble someone you think you know. But any resemblance to someone real is purely coincidental, wink, wink, nod, nod.

Sheila: But please don’t hold that against us!

Janet: Hah, hey everyone, this is Sheila, my co-host, who is also technically fictional. How are you, Sheila?

Sheila: We might be A.I. and sound like voice clones, but honestly, whether real or not, who doesn’t like a real, true-life murder mystery?

Janet: Especially one involving a bank treasurer.

Sheila: Love that. And for bank treasurers listening to the show, this story is right up your alley. We have a story that covers everything you could want, including the bond portfolio, liquidity management, a bank run, and even a bank exam. How much better can it get? We are even going to weave stablecoin into the conversation, so please stick around.

Janet: And by the way, we like to tell all our listeners that if you know something about this case and can come forward with testimony that could help solve it, please reach out to us through the newsletter’s website.

Sheila: Yeah, but I do not think we need operators standing by to take the call. I would doubt anyone could come forward in this case, given that it happened so long ago, right? I mean, this is as cold as it gets for a cold case.

Janet: You never know, but 1878 is a long time ago.

Sheila: OMG, we are talking about a time before the Fed and the FDIC were even established. When the banks, not the Fed, printed their own money and made loans with it. Wow, that is a long time ago. Such a different time.

Janet: Yeah, good times!

Sheila: Haha. So, outline the basic facts of the story for us. What happened?

Janet: Okay. John Wilson Barron was the treasurer of Dexter Savings Bank. We will call him Barron.

Sheila: Or, how about J.W.?

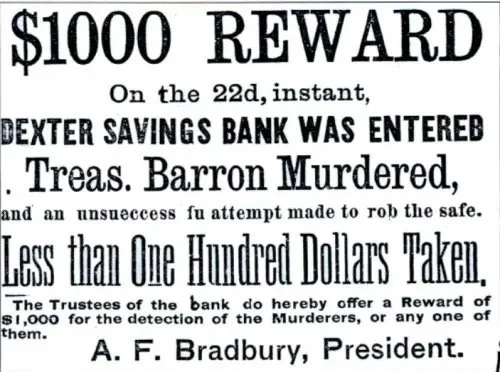

Janet: Let’s stick with Barron. All we know for sure is that sometime in the afternoon on Friday, February 22, 1878, the bank was robbed, and Barron ended up dead. It was a sensational case and made all the newspapers, including the New York Times. Dexter was your typical New England small-town community bank—one branch, located in a building on Main Street in Dexter, Maine. And the building it was in, by the way, is an historic landmark called the Bank Building, which was built two years before our story takes place.

Sheila: Talk a little bit more about the town.

Janet: Sure. Dexter is a typical small town in New England. Lumber was and still is a big industry in these parts. It is on the banks of Lake Wassookeeg, about 30 miles west of Bangor International. Back then, it was the terminus of the Dexter and Newport Railroad—

Sheila: --The A.I. of its day.

Janet: Yes, railroads were one of the major driving forces behind the economy after the Civil War, and as the industry boomed, so did the economy.

Sheila: And when it went bust, so went the economy. A warning for our times with the tech industry.

Janet: In fact, our story begins with railroad over-expansion in the 1860s, which was upended by Jay Cooke's bankruptcy that set off the Panic of 1873. We do not have time to talk much about Jay Cooke and his brokerage house, but you can think of him as the systemic footprint equivalent of the largest too-big-to-fail bank or nonbank you could think of today.

Sheila: Yes, it was an unimaginable, complete disaster for the economy, plunging it into a deep depression. After Cooke went bankrupt, you saw a series of financial panics on Wall Street and bank runs across the country. With the chance that your deposits could fly out the door at any minute, bankers could not even risk making loans, and credit dried up. We take it for granted, and I may have my issues with banks supporting their lending through advances from the Federal Home Loan Banks, but without the financial system infrastructure we have today, banking was tough in those days and anything but a stable profession.

Greenbacks, National Bank Notes, and Stablecoins

Janet: And on top of that, the Government was pushing ahead with its plan to return the country to the gold standard and eliminate the greenbacks. The paper money the Government had printed during the Civil War, with over $347 million in circulation at the time of the robbery, had stoked inflation, which hit 25% in 1864. After the war, it tried to shrink the money supply, which caused deflation. At the time of the bank robbery, deflation was running at -5%. Times were rough for the people who banked with Dexter Savings, like the farmers who owed the bank money and were counting on inflation to help them out.

Sheila: That was the Gilded Age, as Mark Twain called it, all pretty on the outside and rotten on the inside. The rich and super-rich minority lived well, while the masses suffered. You see it today with the data coming from what is popularly called the K-shaped economy. Listen, Janet, I know our audience knows all about greenbacks, but could you give a basic history on them? I know they were the brainchild of Salman Chase, the Treasury Secretary under Lincoln, whose face was on the $10,000 bill that I think is discontinued.

Janet: In 1969, yes. You know, I remember passing by his portrait the last time when I was in the Treasury building. He was a giant—literally. He stood over six feet.

Sheila: Wow.

Janet: But he was a politician, not a finance guy, and ultimately his plan with the greenbacks was a failure, politically almost from the beginning, and financially not too long after. So here is the quick history lesson: When the country was founded, banks issued paper money redeemable in gold or silver under the Coinage Act of 1792. The Treasury did not issue its own money. When it made payments, it used gold or silver.

Sheila: Specie.

Janet: Specie, right. You were able to use the paper money that banks printed for payments, but merchants discounted your cash based on how far they had to go to redeem it at the issuing bank and on the bank's known creditworthiness.

Sheila: You would not take money issued by a bank you did not know. Certainly not one that was failing.

Janet: Yeah, and the fractionalization of the money supply made the payment system super complicated and led to significant frictions because every bank issued its own money.

Sheila: I read how pretty much anyone could start a bank during the Free Banking era before the Civil War. The banking industry underwent a rapid expansion, which then led to an inevitable wave of bank runs and failures.

Janet: You know your bank history, Sheila. But then came the Civil War. War does not come cheap, as the current one the country is waging against Iran is turning out to be, and merchants demanded gold to support the war effort. So the Treasury used its gold reserve to pay for the war, but it was not long before it was in danger of exhausting it.

Sheila: How big is it now?

Janet: It holds more than 261 million fine troy ounces, which is worth about $1.2 trillion based on today’s gold price.

Sheila: What did Chase have in 1861?

Janet: Maybe, less than 2 million troy ounces, worth less than $50 million based on the official redemption price.

Sheila: And there was no income tax back then to turn to for funding.

Janet: And there were limits to deficit spending if foreigners were the ones buying your debt. So, greenbacks were his solution for financing the war and became the country’s first national currency under the Legal Tender Act of 1862.

Sheila: Seignorage. It costs nothing to print a dollar bill, and it solves many financial problems in the short run, until people start demanding more than just paper.

Janet: The only catch was that greenbacks were not redeemable in gold. You could use it to buy groceries, deposit it in a bank, or leave it in your mattress, and it would always be worth its face value. But you could not get one ounce of gold for it.

Sheila: So, the Government cut banks out of the money printing business.

Janet: No. Greenbacks were added to the menu of existing forms of payment, competing with bank-issued currency. But the National Banking Act assessed a tax on currency printed by state-chartered banks. Only nationally chartered banks could print bank notes without a tax, a designation entrusted to the Office of the Comptroller of the Currency (OCC), which it created as an independent bureau of the Treasury to charter qualifying institutions.

Sheila: And the bank notes they printed were redeemable in gold?

Janet: Absolutely. Banks had to meet strict OCC requirements regarding their gold reserves to hold a national charter.

Sheila: Wow, Chase took a complicated payment system and made it even more complex and confusing. Why did you say that it was a failure? Janet: The country was as politically divided over greenbacks as it was over slavery. Farmers loved it because it was inflationary and helped them pay their debts, and banks and creditors generally hated it for the same reason. Inflation soared as greenbacks entered circulation. But generally, the country has always had a predisposition toward hard currency, or money that could be converted into gold or silver coins.

Sheila: You just reminded me how 55 years ago, John Connally, President Nixon’s Treasury Secretary, closed the gold window to pay foreign holders of Treasurys.

Janet: But, do you want to know a fun fact? Lincoln nominated Chase in 1864 to sit on the Supreme Court.

Sheila: So, he comes up with a plan that causes inflation to surge to crazy heights, and he gets rewarded for that with a lifetime appointment to the Supreme Court? I mean, it’s hard to see Jerome Powell appointed for something new in this Administration, considering what happened to inflation under his watch.

Janet: Probably a few other issues that would play a role in his appointment to future roles under the Administration. But here is the best part. While he was there, he wrote an opinion in 1870 stating that the Legal Tender Act of 1862, which he had pushed for while working for Lincoln, was unconstitutional and that nothing in it lets the Government print fiat money.

Sheila: What?

Janet: A year later, technical details led the Supreme Court to reverse the decision, but it goes to show you just how politically toxic fiat money was in those times.

Sheila: At least to the people making the campaign donations.

Janet: It is a lot like today’s politics against the Fed’s balance sheet, arguments that the Federal Reserve Act does not give the Fed the right to balloon its balance sheet and the money supply by monetizing the national debt. According to the Fed’s new Chair, Kevin Warsh, Quantitative Easing was a temporary measure and should have been reversed after the Global Financial Crisis and COVID, not made a permanent feature of the Fed's balance sheet.

Sheila: I assume you heard Michael Barr give his thoughts about plans to shrink the balance sheet by encouraging banks to hold less reserves at the Fed?

“I think shrinking the balance sheet is the wrong objective, and many of the proposals to meet this objective would undermine bank resilience, impede money market functioning, and, ultimately, threaten financial stability…the size of the Fed’s balance sheet is the wrong measure of the Fed’s footprint in financial markets.”

Janet: I think he is right to sound cautious.

Sheila: But unlike the Fed’s balance sheet expansion, at least you could say that greenbacks helped farmers make payments and supported commerce in places like Dexter, Maine.

Janet: Unfortunately, greenbacks did not work any better than the payment system under the Free Banking era.

Sheila: If they were worth a dollar and not eligible for redemption, what was the problem? You no longer needed to have a bank account or gold to participate in the payment system. All that mattered were the greenbacks in your wallet.

Janet: Because prices for everything you could buy with them were quoted in gold dollars. And, remember, greenbacks were issued under the assumption that this was a temporary measure in an emergency and that after the war ended, the Government would redeem them. If you wanted to buy something with a greenback dollar, you paid a premium for it over a gold dollar.

Sheila: Reminds me how merchants charge you today to use a credit card instead of cash.

Janet: That premium rose or fell depending on what people believed the chances of redemption were. In 1878, it ran as high as 6 cents on a dollar. As the war progressed and costs continued to climb, the premium increased as people assumed the chances of redemption were lower. Basically, greenbacks traded at a discount shortly after the war began and never returned to par. After the war, the gold/greenback exchange rates trended with prospects for redemption, which became less and less likely because shrinking the money supply was deflationary, and trying to do so was killing the economy.

Sheila: What about the money printed by the national banks? Why couldn’t they ramp up printing banknotes to take the place of greenbacks?

Janet: The money national banks printed was marginal compared to the supply of greenbacks and outstanding gold and silver specie. How do you really compete with an IOU from the Government as a private issuer, even if your money is redeemable in specie?

Sheila: Then again, the money they could print was interest-free funding on their gold reserves. That was worth something.

Janet: Well, you bring up an interesting similarity between greenbacks and stablecoins under the GENIUS Act.

Sheila: Because paper money does not pay interest, the stablecoin token pays none to the holder? I am sure you saw that the Senate version of the CLARITY Act will permit issuers to offer some form of a discount coupon to stablecoin holders.

Janet: Yes, that is a similarity, too. But I was really thinking that they are similar because greenbacks were not money, and neither is a stablecoin.

Sheila: They were designed to be used for payments. How are they not money?

Janet: Think of it this way, if someone paid you a greenback during the Civil War, you might accept it for payment under the law, but even if you acquired greenbacks at a discount, you would still need to figure out who would take them and at what exchange rate for specie. Specie was real money, usable for payments and as a store of value. You did not need an off-ramp for specie.

Sheila: But stablecoins are pegged one-for-one with the dollar.

Janet: Yes. They are worth par, but if I accept stablecoins as payment, I still need to find an off-ramp to convert them back to fiat currency. At the end of the day, I need cold, hard cash. But if I pay you in cash today, that is the final step in the payment process. This is why even the GENIUS act does not fully insulate stablecoins from a run.

Sheila: Hmm.

Janet: Oh, and how about this? Under IAS 7, because stablecoins lack guaranteed redemption and have counterparty risk, even though they are pegged one-for-one with the dollar, they are not a cash equivalent; they are a digital asset.

Sheila: And if I accept a stablecoin, I have to redeem it with the issuer, which is like a bank note used to be, no? Each national bank issued notes redeemable in gold or silver, you said.

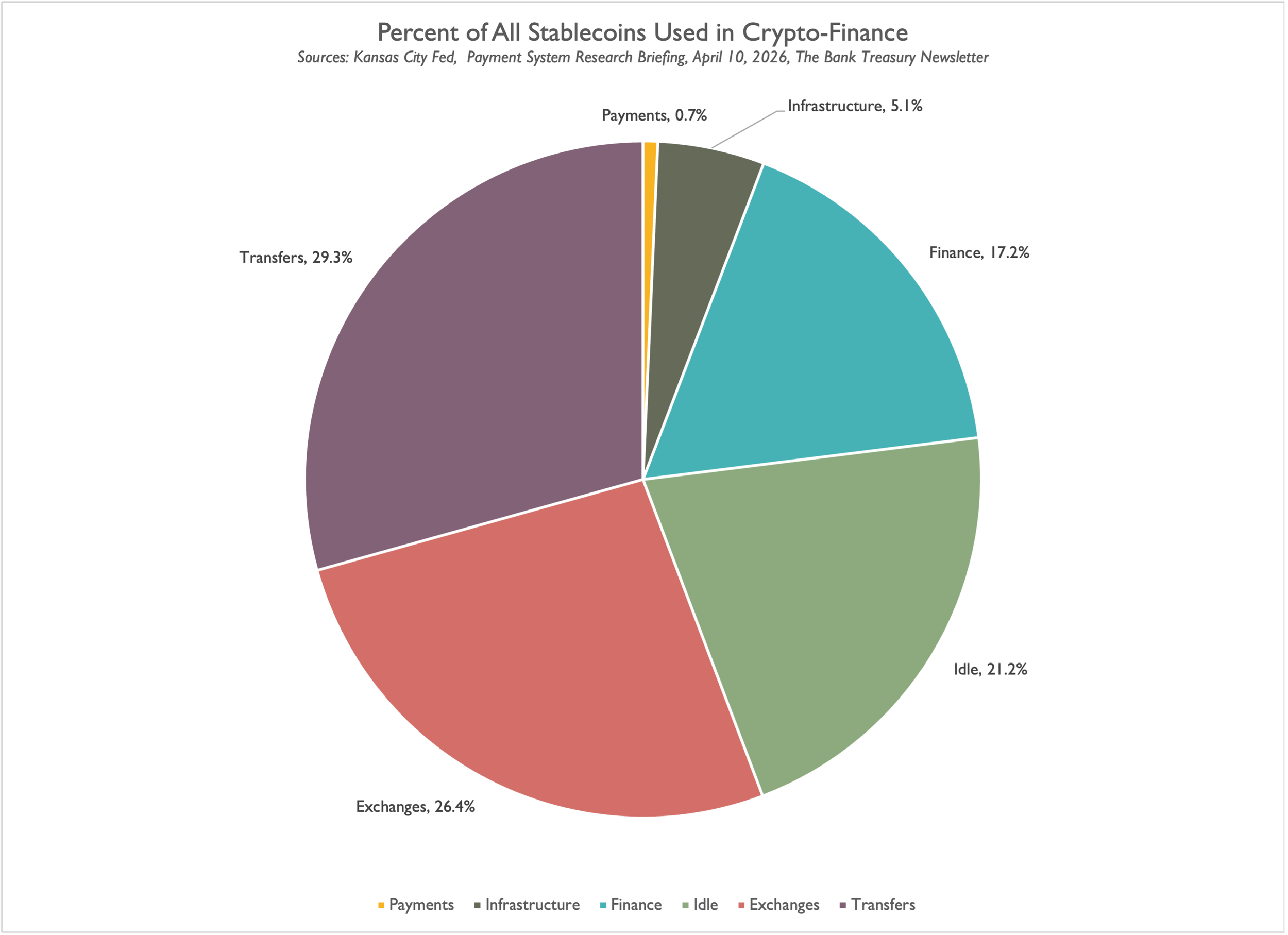

Janet: That was kept at the Treasury. Yes, greenbacks and banknotes share many similarities with stablecoins. But real money is different. You can use real money for payments, and it is a store of value. It is what is often described as the singleness of fiat currency. You trust its value because you trust the central bank that printed it. And by the way, I saw some research from the Kansas City Fed suggesting its use for payments is very limited (Figure 1). Can I read you an excerpt from a speech last month by Pablo Hernández de Cos, the General Manager of the Bank for International Settlements, that fits what we are talking about?

Figure 1: Percent of All Stablecoins Used in Crypto-Finance

Sheila: Okay, because I have more questions about the murder case, as soon as we can get back to it.

Janet: Let me read what he said,

“Stablecoins seek to leverage trust in fiat currency. This underscores that the monetary anchor provided by central banks remains indispensable – regardless of the future role of stablecoins or any other technological innovation. Ultimately, money is far more than a technology: it is an institutional achievement that prospers with trust in domestic and international cooperation… More fundamentally, singleness ultimately relies on the central bank's monetary anchor. While the crypto ecosystem embraces decentralization and rejects the need for a public trust anchor, stablecoins attempt to import credibility from public money while operating outside the established settlement system. This creates a tension that is not easily resolved.”

Sheila: So, you think there is a risk of runs on stablecoins?

Janet: Stablecoins as conceived under the GENIUS Act are like “narrow banks,” institutions that invest 100% of their deposits in overnight, highly liquid, risk-free assets. But they are not the same. Narrow banks have a master account with the Fed, and their depositors are eligible for deposit insurance. Stablecoin holders are not eligible for deposit insurance. So, the possibility of a run on a stablecoin is, almost by definition, higher than that for a narrow bank, as recent Atlanta Fed research shows. And a stablecoin reserve can include deposits at other banks, which means a bank run could spread to stablecoins, too.

Sheila: Preventing that scenario rests on strong supervision to ensure that stablecoin reserves meet requirements and can cover redemptions. Unfortunately, that is not made easier by supervisory agencies' inability to recruit and retain staff. The problems at the FDIC only deepened in recent years, as an Inspector General report published last March found. If this is the system we have to monitor the integrity of stablecoin reserves, we could be in trouble.

Back to the Scene of the Crime

Janet: Okay, so let’s get back to our story, and apologies to our audience for that tangent into greenbacks, stablecoins, and payments, but you will see it will all come together in the end. So, it was just after 6 PM on February 22, 1878, when John Wilson Barron, the bank's treasurer, was found unconscious, beaten, with blood everywhere from terrible gashes on his head. His wife had grown worried when he did not come home for dinner on time and asked one of the bank’s employees to check on him.

Sheila: But wait, it was Washington’s Birthday. What was he doing at the bank?

Janet: Well, technically, it was not a Federal holiday in 1878, because President Rutherford Hayes only made it so a year later, but you are right that February 22nd was Washington’s birthday, and it was celebrated with parades and parties even before it became a national holiday, so I am sure he went to the bank that day thinking that business would be slow and he could catch up on his work.

Sheila: Wow. I cannot conceive of not taking that day off.

Janet: Initially, police believed that burglars had hidden in the building, waited until everyone had left, surprised Barron in the back room where the safe was located, hog-tied him with a rope around his neck that was strangling him when he was found, and beat him to a bloody pulp, all in an effort to get him to reveal the combination to the safe. When he refused, they beat him some more, put a gag in his mouth, and left him to die in the outer room of the safe, according to the newspaper reports.

Sheila: This sounds like a classic bank robbery.

Janet: You are right. In 1876, the Northampton National Bank was robbed. The robbers took hold of the treasurer, forced him to disclose the safe combination, and then made off with $1.6 million in cash, bonds, and other securities.

Sheila: But the robbers never got into Dexter’s safe? Did they get away with anything?

Janet: I saw conflicting reports that they stole less than $100 or maybe $200, whatever was in the Barron’s cash drawers, because they couldn’t get into the safe. Whatever jewelry and securities were in there went untouched because he refused to open the safe.

Sheila: He was a hero.

Janet: That is what you would think.

Sheila: I’m surprised the robbers didn't try to blow up the safe, as they often did, if he wasn’t going to open it.

Janet: Probably because they ran the risk of destroying the contents of the safe along with it, or even blowing themselves up in the process. Plus, the robbers chose Washington’s Birthday precisely to avoid drawing attention.

Sheila: How much cash do banks normally keep in a vault?

Janet: Normally, a bank of its size would have kept between $10,000 and $15,000 in its vault, less than 1% of its assets in pure cash, greenbacks, and national bank notes. As much today as back in 1878, bank treasurers would want to keep as little cash as necessary of their total assets in a vault earning 0%.

Sheila: Which is why if stablecoins ever take off and you figure out the singleness problem, bank treasurers would still not want to invest in them because they could simply take their cash and stick it in a vault.

Janet: Well, the difference there is that stablecoins can be transmitted through distributed ledger technology, while the cash you keep in the vault is of no value from a liquidity standpoint.

Sheila: Other than when you have a mob at your door demanding cash.

Janet: But to complete the point, for purposes of the Basel 3 Liquidity Coverage Ratio, vault cash is not part of High-Quality Liquid Assets. According to March 2026 call reports, currency and coin held by all commercial banks totaled $71 billion at quarter-end, or 0.3% of total assets.

Sheila: That is counting pennies, right?

Janet: Funny. Yes, that is counting pennies, although who knows for how long, as the Fed does what it can to help with the circulation of a coin that had cost more to produce than its worth before the mint stopped its production last year. I could not find published financials for Dexter Savings at the time of the robbery, but in 1881, Dexter reported total assets of $160,000, including $27,000 in cash. Of this cash balance, the bank kept $12,000 on deposit at the First National Bank of Dexter, and the rest was in its vault. First National Bank of Dexter, by the way, was not much larger than Dexter Savings; its total assets equaled $240,000. And here is a fun fact for you. The First National Bank of Dexter and Dexter Savings were literally down the hall from each other in the Bank Block.

Sheila: Dexter and Dexter. Interesting. Presumably, it was Dexter National’s notes that the robbers stole from Dexter Savings Bank’s cash drawers. And did anyone hear anything? I guess Barron never said what happened to him.

Janet: Nah, sadly, he never woke up. A doctor who examined him at the scene thought he might have been drugged. The people who found him carried him home, and the story goes that he opened his eyes briefly, saw his wife, and died. As far as witnesses, Charles Curtis, the cashier at Dexter National, which was across the hall from Barron’s office, never heard anyone come in or out of Barron’s office that day, but I think he left around 5 PM. As for the last hour before he was found, the postmaster, “Mr. Woods,” was in the building, too, in an office just below Dexter’s safe room, where Barron was found.

Sheila: And did he hear anything?

Janet: Not a thing. But he did notice the Barron had left a window open in the back.

Sheila: In the winter? That is strange. In any case, he was a hero.

Janet: Right. That was the initial assumption. There were whispers that three “strangers” were seen passing through town at the time of the robbery, and police stopped to question possible suspects, but everyone had an alibi. Whoever the robbers were, they were in the wind and disappeared without a trace. There was a theory that the robbers escaped from the roof of the building. But the robbery took place right after a fresh snowfall, so there should have been footprints up there, yet the police found none. Normally, after a bank robbery, people see strangers turning up somewhere, maybe trying to spend some of the loot. But nothing turned up. Every lead was a dead end.

Sheila: So, curious how much money was in the safe?

Janet: Great question. The answer is that there was no cash in the safe.

Sheila: What? How? No greenbacks? No Dexter National Bank notes? Nothing?

Janet: The only thing found in the safe was a $500 Treasury Bond that Barron bought literally just the day before.

Sheila: Stop! Wait. Like SVB? What was the term?

Janet: The typical bond had a 10-year term and paid 4% interest.

Sheila: What was he planning to do if he needed liquidity? Repo it?

Janet: But let’s think about this. It is 1878, and bank runs are practically an everyday occurrence in the banking industry. It is five years since the Panic of 1873, when 100 banks failed nationwide. That panic set off subsequent panics. A week before the robbery, a run on another bank in Maine, Newport Savings, led to its suspension of payments and failure. The run on Newport Savings led to runs on other banks, including Dexter.

Sheila: Talk about a stress situation.

Janet: Yes, Barron was already dealing with liquidity strains from large withdrawals. If those outflows had continued much longer, the bank would have been forced to suspend withdrawals and would probably have failed. So, in such an environment, ask yourself this: why would Barron have kept such a low level of cash and then bought a long-term Treasury with the little cash he had on hand? Does that make sense?

Sheila: Nothing here makes sense. I am sorry. I am so confused.

Janet: It gets worse. Nine months after the robbery, the bank’s new treasurer, George Hamilton, had to prepare a summary of the bank’s financials for an upcoming bank exam. But when he tried to use Barron’s last report as a template, he could not get Barron’s numbers to add up.

Sheila: What?

Janet: You see, when you asked how much cash was in the safe, I said there was none. There should have been $1,600 in the safe.

Sheila: In greenbacks or banknotes?

Janet: There was neither. Then George discovered that Barron was keeping two sets of books, one showing the bank’s total liabilities at $220,000 and the other at $218,000. Auditors later found that several entries in the ledger had been erased and rewritten multiple times.

Sheila: So, what did the police think happened? It sounds like Barron might have been embezzling money from the bank. But are we saying Barron staged a bank robbery to hide his crime? And why would he be killed? Or are you saying it was a suicide?

Janet: Great questions. By the way, according to what I read, there were two sides to the story. One side knew him as an “honest and upright” individual, a devout Methodist, and a town trustee. That side believed he would never have stolen from the bank. The other side believed there was no other answer, that he was a crook who tried to cover up his crime with an elaborate charade.

Sheila: But why did he have to die?

Janet: I think Barron was worried that after Newport Savings failed, Dexter would be next, and that the run on the bank would have forced him to suspend withdrawals, which would have led to an audit that would have uncovered his crime.

Sheila: But what was his motive for even stealing from the bank?

Janet: Here are a few facts about Barron. His annual pre-tax income was $1,030, which he used to support his wife and five children after paying annual expenses, including $150 in mortgage interest on his home and $600 in taxes.

Sheila: So, you are saying that he was over his head in expenses and stole from the bank to balance his books, so to speak? Couldn’t he have just asked for a raise?

Janet: Sheila, this story is more confusing than you could ever imagine. Just before the robbery, he bought a $13,000 life insurance policy.

Sheila: He took out an insurance policy for his wife and kids?

Janet: No. He took out one payable to the bank. And remember the $1,600 I told you was missing from the safe? That was the policy's annual premium.

Sheila: He bought BOLI—bank-owned life insurance? Bank treasurers hate BOLI, I thought, because of the accounting.

Janet: Assuming he used the missing $1,600 for it, yeah.

Sheila: Wait, this story is nuts. So he staged his suicide as a robbery gone wrong to help the bank’s return on assets? Huh?

Janet: But hold on. I have one more little piece of information to give you the complete story of our hero/crook, who was or was not murdered for refusing to open the bank’s safe for the robbers, if they even existed.

Sheila: All ears.

Janet: The safe was on a timer lock. Barron could not have opened it, even if he had wanted to.

Big Bank, Little Bank, and Deposit Insurance

Sheila: So, the bank may or may not have been robbed; Barron may or may not have been a crook and complicit in a bank robbery if there was one; nothing of much value was actually stolen from the bank; and Barron ends up dead to solve his cash flow problems and the bank’s bottom line. Is it me, or does nothing about this case add up?

Janet: It is not you.

Sheila: What happened after the robbery? You said you found a financial statement from 1881, but what happened after? Being a small bank in those days was perilous. Many of them failed during those financial panics, unlike the large, too-big-to-fail banks that dominate the banking landscape then and now.

Janet: Yes, the philosophy of "too big to fail" led clearing houses during the Gilded Age, which served as a substitute for the Fed before it was established, to help save the big banks when they got into trouble and to turn their backs on the small ones. But for the record, I do not think Dexter failed, at least not after this robbery and the scandal.

Sheila: I only bring it up, and I am sorry to get us off topic, but I am still trying to wrap my head around the failure of Community Bank and Trust - West Georgia this month. It is the second bank and the second small bank of the year to fail.

Janet: Yes, I saw the notice on the FDIC’s website.

Sheila: It reported last March that it had $288 million in total assets. From what I can tell, its ag-loan portfolio suffered a sudden, massive hemorrhage. Until last year, its numbers were fairly normal. This is the second bank to fail this year, and like the first, Metropolitan Capital, it is small. As with Metropolitan, uninsured depositors are not being rescued and are relying on asset sales to recover their uninsured deposits.

Janet: Whether large or small, bank failures affect the economy. Vice-Chair of Supervision Miki Bowman noted in a speech this month that the banking industry underserves many agricultural communities and that small community banks often step in to help. In Kansas, for example, community banks use mobile offices to serve these communities.

Sheila: But this is what I found so surprising. The failure will cost the FDIC nearly $100 million, five times what Metropolitan cost. Metropolitan failed last January and had total assets of $261 million. Such losses relative to total assets are very rare. Honestly, I never heard of it since Indymac, which was $32 billion when it failed and cost the FDIC $12 billion.

Janet: Well, at least the FDIC is there to protect depositors, especially at small banks. And if the country had deposit insurance in 1878, maybe we would not have seen as many runs as we did.

Sheila: The country needs adequate deposit insurance, Janet. How can the OCC propose to raise the asset threshold for resolution planning to $700 billion from $250 billion and make that a priority, when the last time the threshold was addressed was 2018, and Congress cannot figure out how to raise the deposit insurance cap from $250,000, when the last time the cap was adjusted for inflation was 2010?

Janet: I agree. And deposit insurance is a critical factor for community banks, which compete with larger banks for deposits.

Sheila: You know why deposit caps have not changed in 16 years? Because big banks do not want them changed. I read somewhere that between 1886 and 1933, there were about 150 bills in Congress to establish the FDIC, and they went nowhere because the big banks opposed them. It took a catastrophic wave of bank failures after the Great Crash, which nearly brought down the financial system, to prompt radical change and the establishment of the FDIC. Big banks didn’t want adequate deposit insurance then, and they don't support it now, because it really helps small banks, not them.

Janet: I hear you, Sheila. Deposit insurance reform is one reason those economically ruinous bank runs you saw throughout the 19th century are less common today, as Fed research shows.

Sheila: Meanwhile, after holding a few hearings on the subject, I saw nothing further in Senate Banking Chair Tim Scott’s year-end report about it as a 2026 priority.

Janet: But there is a bill in the House to introduce an inflation adjustment for the insurance cap.

Sheila: And to my point, it has gone nowhere.

Janet: Look, I can tell you that the Fed needs small banks as much as it needs large banks to conduct monetary policy and ensure that its supply of reserves remains ample, the maintenance of which is not an exact science. A Fed research paper published last February found that small banks significantly adjust their demand for reserves in response to deposit inflows and outflows, and that their demand for reserves is more elastic in response to supply constraints than that of larger banks.

Sheila: Which are not active in the Fed funds market because they already hold a ton of liquid assets for regulatory purposes.

Janet: Exactly. The researchers concluded that the best way to gauge whether reserves are ample is to pay attention to small banks and their bids and offers in the Fed funds market.

Sheila: But I thought Kevin Warsh is against an ample reserve regime.

Janet: Ample or not, small banks’ trading volumes in Fed funds might be a good early warning signal for the Fed when financial stress is forming long before we get to a full-blown emergency.

More Twists and Turns in the Story

Sheila: I know I took us on a tangent, but let’s get back to the story.

Janet: As you would suspect, with your main suspect dead, and all other leads having gone cold, and with the losses accounted for and even recovered thanks to the insurance policy Barron had bought, the case went cold for nine years. One day, however, Charles Francis Stain, a small-time thief serving time in the Norridgewock Jail just down the road from Dexter, told the police he had information about the robbery and Barron’s involvement.

Sheila: I have to imagine his widow was going through hell. Even if the guy is a con, he could have helped Barron’s reputation and his widow’s chances of avoiding ostracism in a small town like Dexter.

Janet: For sure. So his story is that his father, David Stain, and a friend of his, Oliver Cromwell, who lived in Massachusetts, robbed the bank.

Sheila: Oliver Cromwell, like the guy who beheaded the king of England and declared himself Protector? Haha.

Janet: Charles said his father told him and threatened to kill him if he told anybody. Stain said his father told him they had entered the bank and demanded money. Barron refused. David Stain hit Barron over the head, and Cromwell tied him up and strangled him. Stain also said that no one meant to kill Barron, that it was an accident.

Sheila: I have lots of questions about this story. I thought the police found no tracks, found no leads. How did they get away?

Janet: David outright denied the allegations, saying his son made up the story because he would not give him money while he was in jail. He certainly did not check many boxes. He may have had an alibi, too. The father, unlike his son, had no criminal record and was already well into his 50s by the time of the robbery. But on the strength of the son’s accusation, he was convicted and sentenced to life in prison in 1888.

Sheila: Justice was finally served?

Janet: Yes. I even found a letter from 1890 in which the treasurer of another community bank congratulated Chloe Barron, his widow, on her husband’s exoneration. But 13 years later, Maine Governor Llewellyn Powers pardoned Stain, set him free, and he died a pauper not long after.

Sheila: For good behavior?

Janet: No, his son recanted his testimony, and the case against his father collapsed.

Sheila: Amazing. So we are back to square one. This doesn't explain why, even if he wasn't involved in the robbery, he let his cash position run down. Or why there were erasure marks you said George Hamilton found, and the two sets of books. If only he could have printed money like his friend Curtis, who worked across the hall at the National Bank.

Janet: But the story is not over. Did you ever hear about George Leslie? He was considered the greatest bank robber of his day because he invented a safe-cracking tool he called the “joker,” a device he somehow slipped into the safe's dial that secretly recorded the combination. Unlike his peers, he used no explosives and maintained a strict code of nonviolence.

Sheila: Interesting.

Janet: The gangs that robbed banks began to realize that instead of trying to rob stores of merchandise and then try to fence it for a fraction of its value, why not just rob the bank where the money was kept and bypass the fence entirely? As Willie Sutton used to say, he robbed banks because that is where the money was.

Sheila: Sounds like another argument against stablecoins, greenbacks, and bank notes.

Janet: Before the Dexter robbery, Leslie was planning one of the day's biggest bank heists, the October 1878 robbery of the Manhattan Savings Institute. The robbers made off with $3 million from the bank. But four months after Dexter, and before the Manhattan Savings Institute heist, George Leslie turned up dead, his body found with no identification by the Bronx River in New York, apparently murdered by a bullet to the head.

Sheila: So, he killed Barron?

Janet: No, and I regret to tell you that officially, the Dexter Savings Bank robbery remains officially unsolved.

Sheila: So why did the Pinkertons think that Leslie was involved?

Janet: Most of the $3 million stolen in the Manhattan Savings Institute robbery consisted of nonnegotiable bonds. When some of the robbers tried to sell them, they were arrested. One of them told the police that Leslie planned the Dexter robbery because he believed Barron had $800,000 in Dexter’s safe and that Dexter could serve as a dry run for the bigger heist he was planning. He bribed Barron into letting his gang into the bank on Washington’s Birthday.

Sheila: They came in through the open window?

Janet: Probably, but when they arrived, Barron was waiting for them and told them he had changed his mind and would not cooperate.

Sheila: What was with this guy?

Janet: Leslie apparently gave up at this point and left Barron in the hands of his accomplices, who were quite upset and beat Barron nearly to death. The next day, when he read the news about Barron’s murder, he complained to his fellow accomplices that what they had done had made him an accessory to murder. The other gang members grew worried that he would go to the police and decided to kill him first.

Sheila: No honor among thieves, I suppose.

Janet: No, but even with this story, nothing was ever proved in court, and the story about Barron’s murder and his involvement in the Dexter Savings Bank robbery remains a true unsolved bank treasurer murder mystery. But if you ever find yourself up in Dexter, Maine, be sure to visit Barron, his first wife, Sarah, his second wife, Chloe, and all that is left of this story at Mount Pleasant Cemetery.

Sheila: Quite a story. I cannot wait for the next time we talk on another episode of the Bank Treasury Murder Mystery Series.

Janet: Until then.

The Bank Treasury Newsletter is an independent publication that welcomes comments, suggestions, and constructive criticisms from our readers in lieu of payment. Please refer this letter to members of your staff or your peers who would benefit from receiving it, and if you haven’t yet, subscribe here.

Copyright 2026, The Bank Treasury Newsletter, All Rights Reserved.

Ethan M. Heisler, CFA

Editor-in-Chief

This Month’s Chart Deck

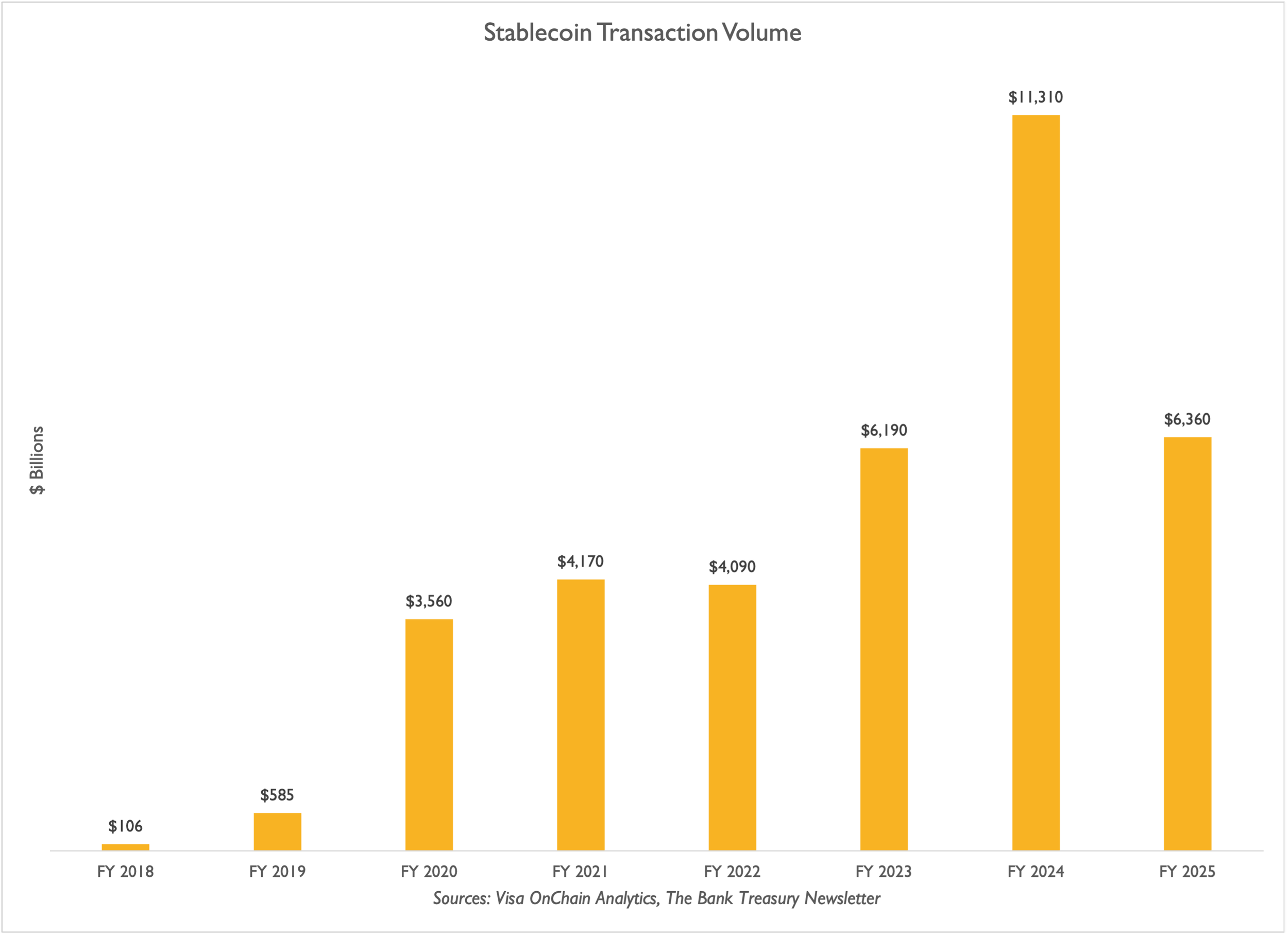

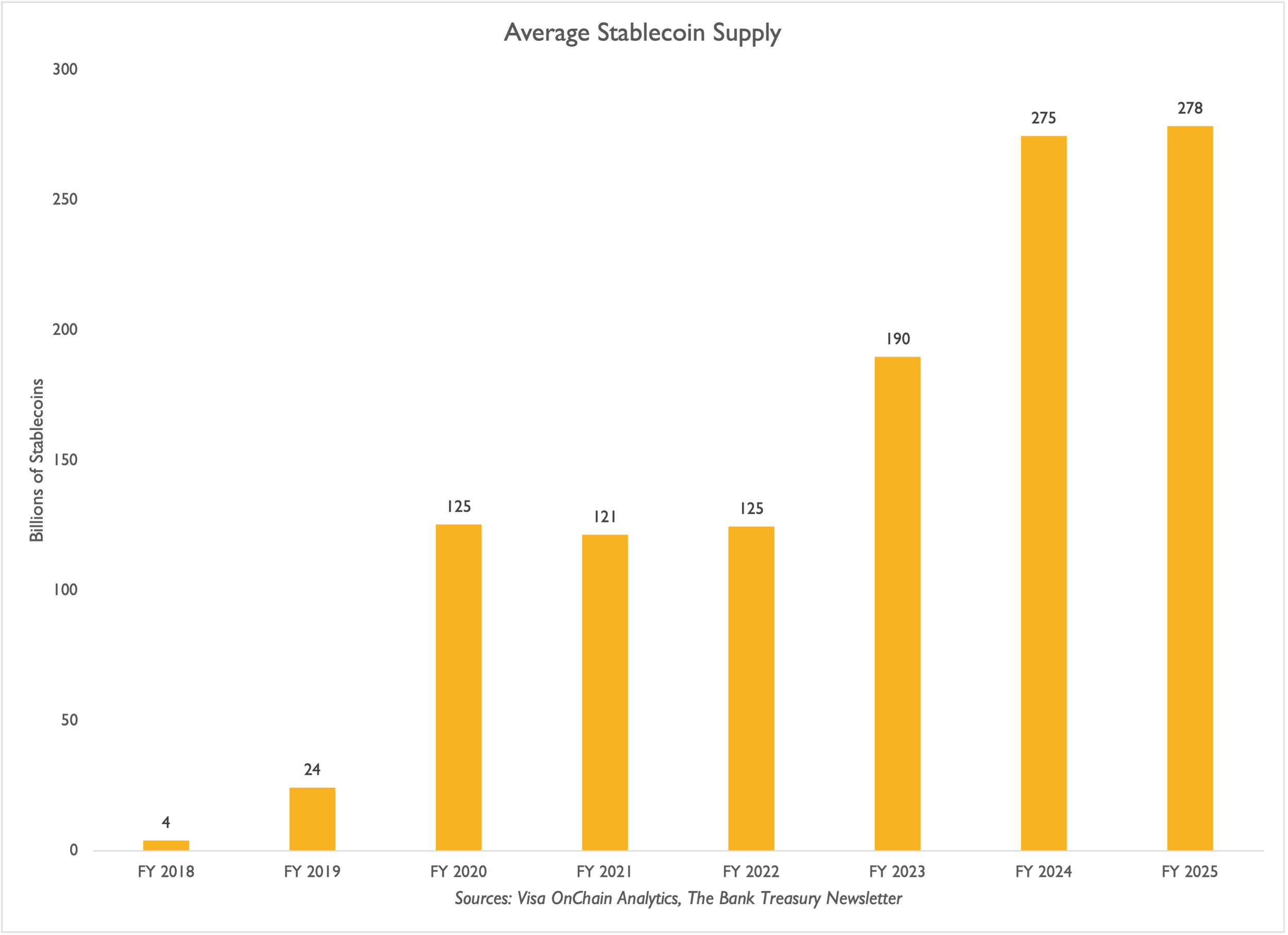

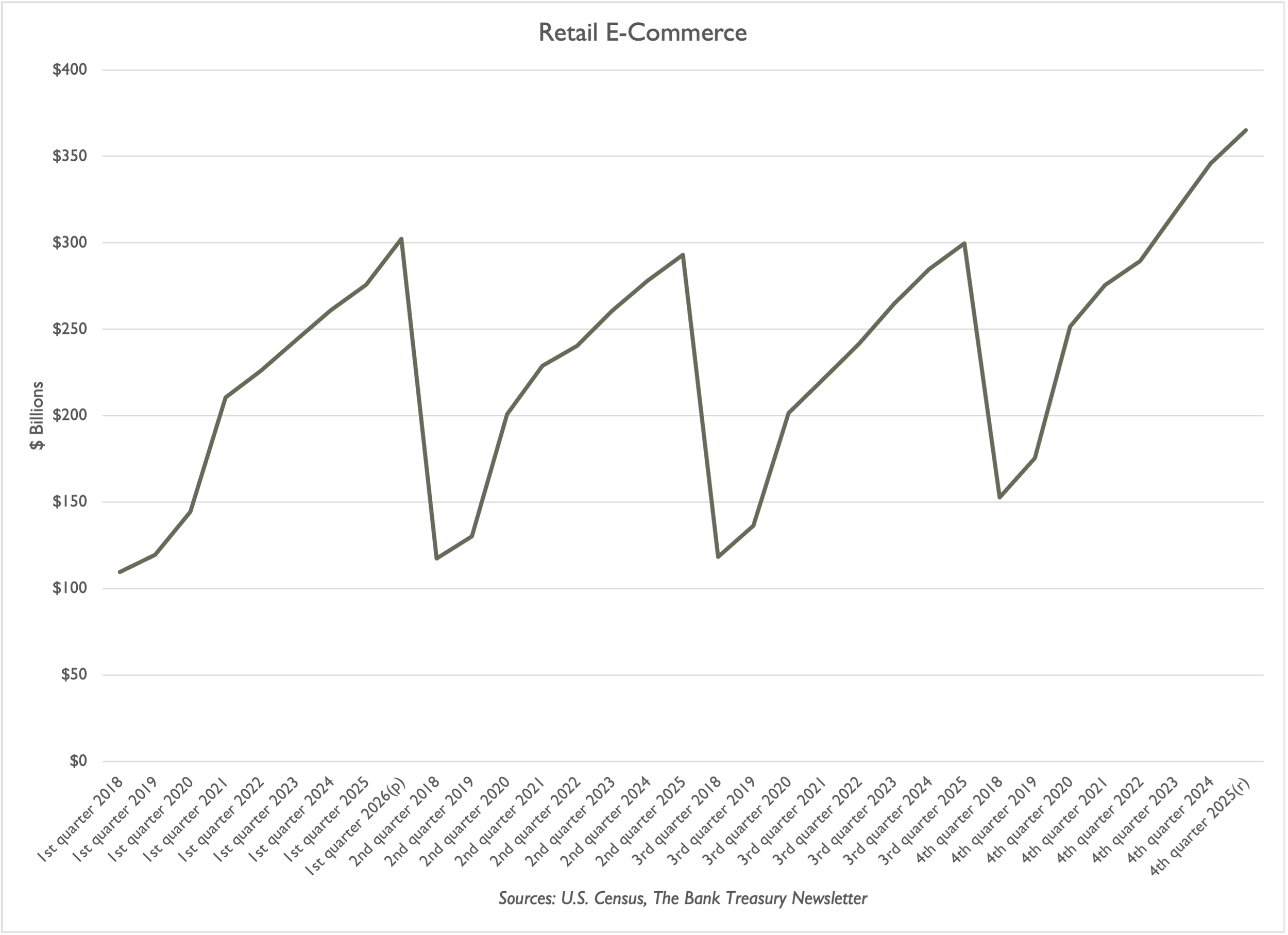

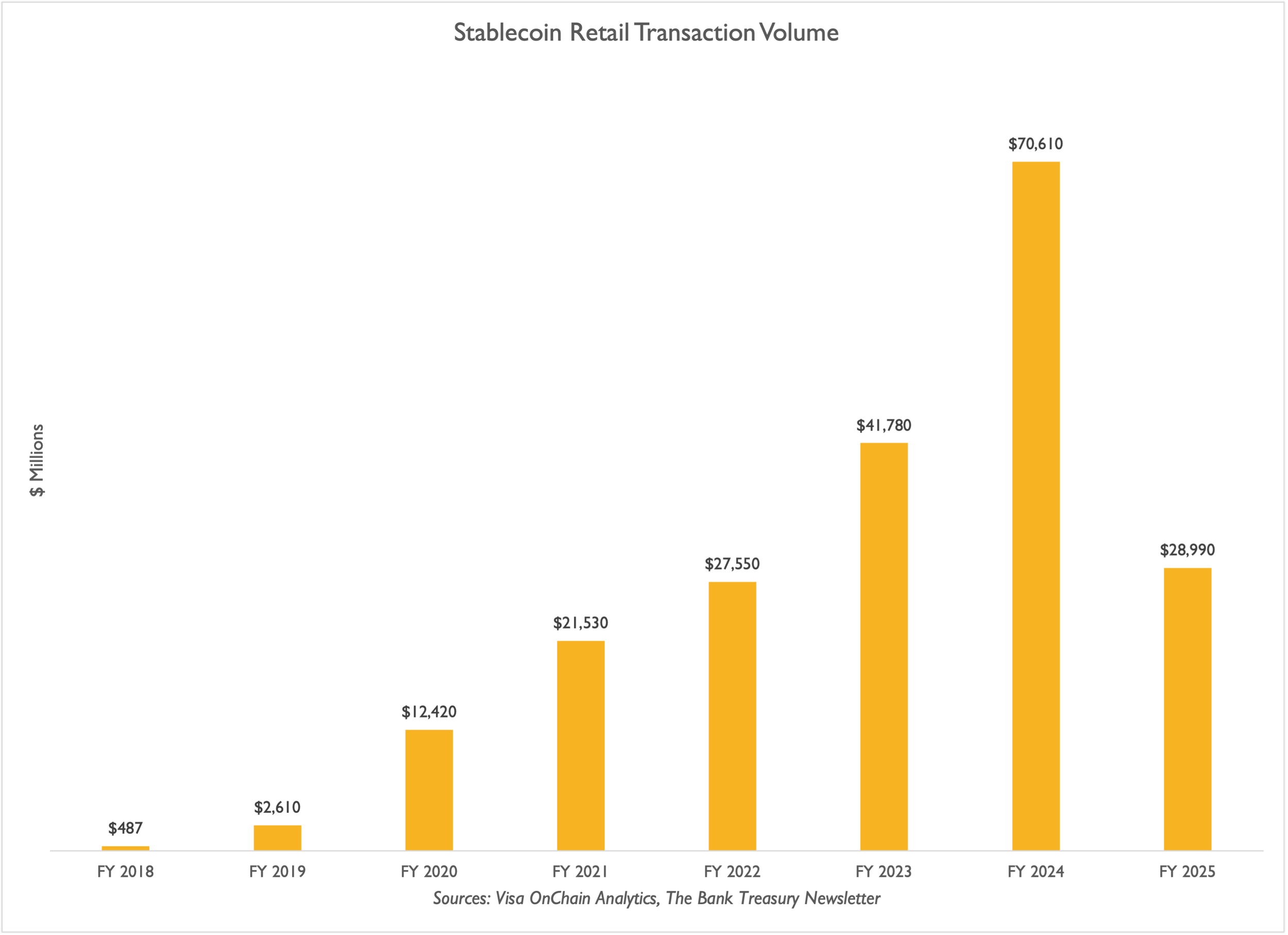

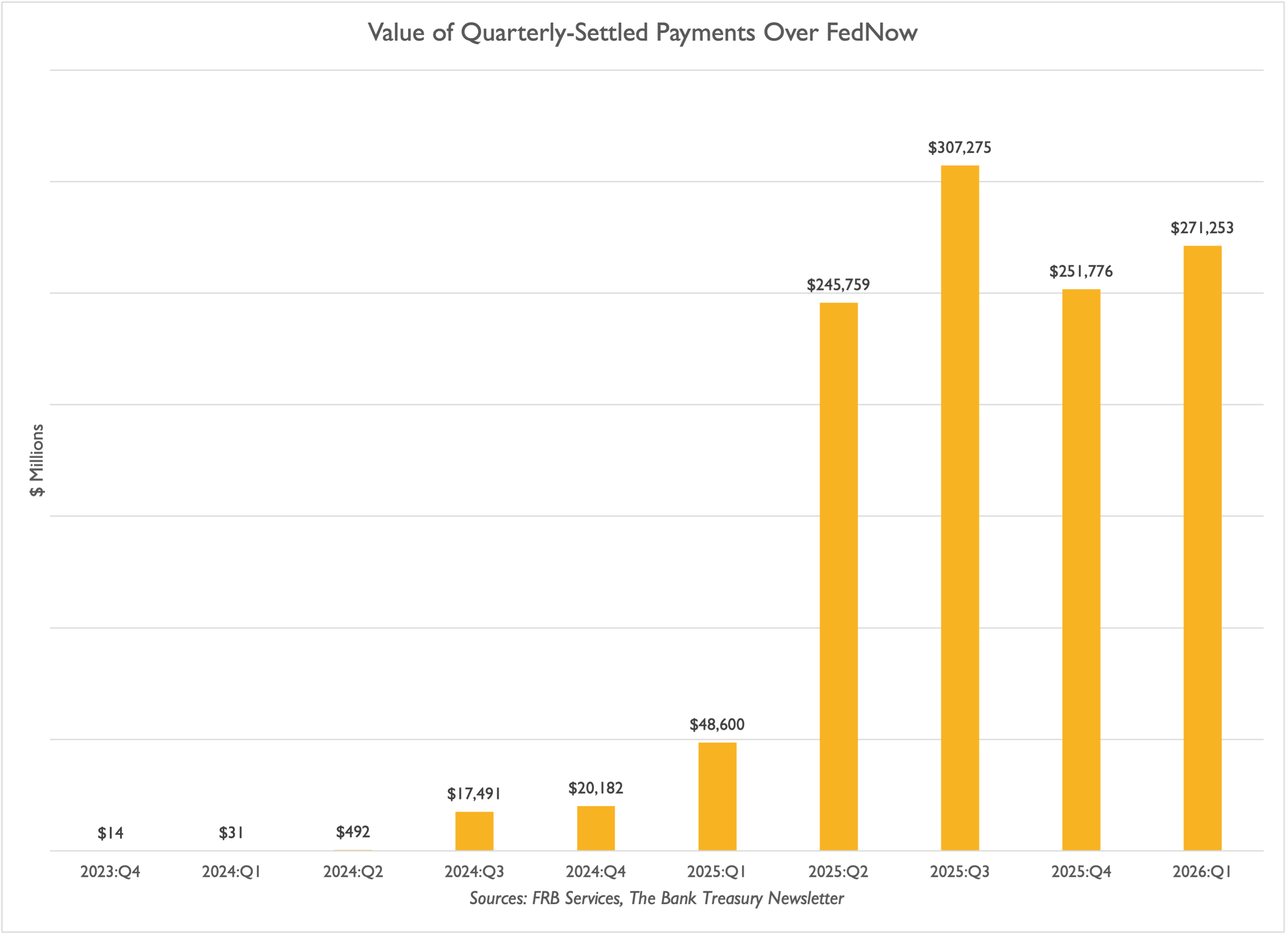

As the Clarity Act nears a Senate vote, legislative efforts to expand the cryptocurrency industry and promote stablecoin adoption for business payments are taking shape. However, as highlighted in this month’s newsletter, the use case for stablecoins in payments remains limited. Last year, stablecoin transaction volumes exceeded $6 trillion, driven primarily by trading activity (Slide 1), but adjusted for high-frequency and high-volume trading wallets, high-frequency and high-volume smart contract addresses, and bot-related activity. According to Visa, the supply of stablecoin tokens increased significantly in the first half of the decade, averaging 278 billion last year (Slide 2). While e-commerce sales topped $1 trillion last year (Slide 3), retail transactions using stablecoins accounted for only $71 billion of that total (Slide 4). Overall, instant payment activity has been growing rapidly in the first half of the decade, but recent FedNow platform data indicate it has stabilized in recent quarters (Slide 5).

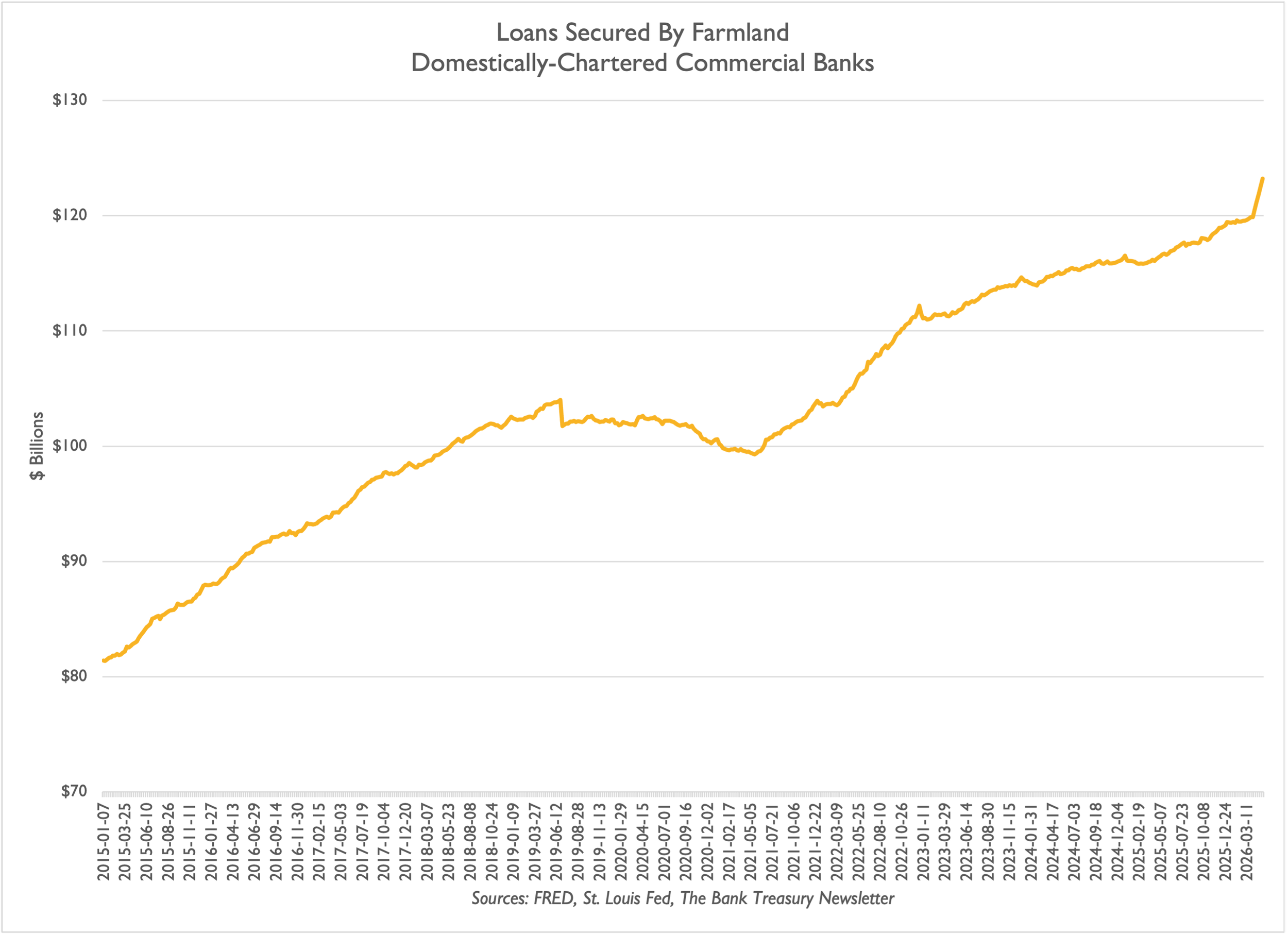

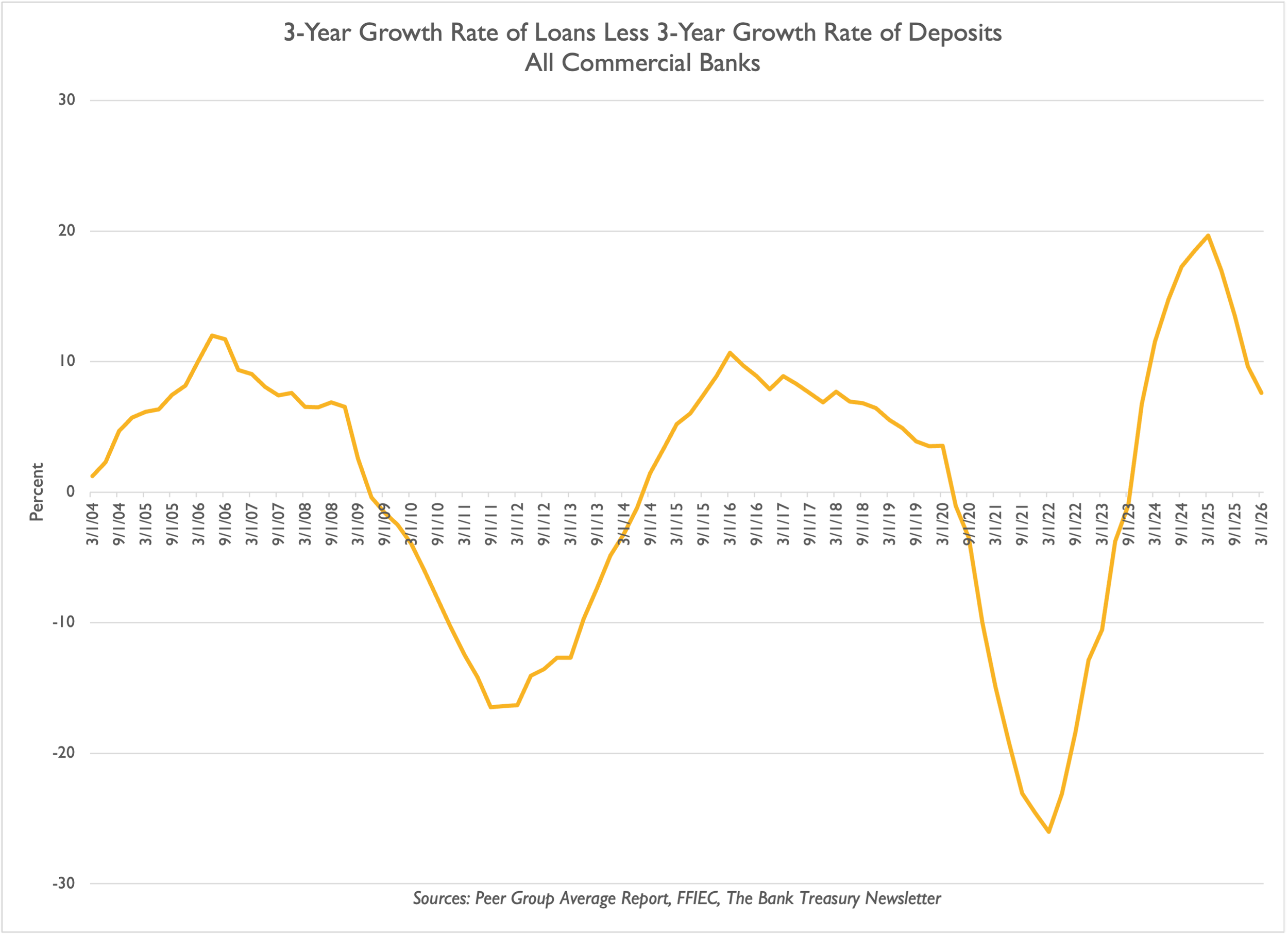

As noted in the newsletter, Community Bank and Trust-West Georgia, a $288 million bank mainly focused on farm loans, became the second bank to fail this year (Slide 6) due to credit issues in its portfolio. Its failure will cost the FDIC’s Deposit Insurance Fund $100 million, the largest proportional loss since IndyMac. Although agricultural lending represents a small part of the overall banking industry loans, it has increased by 50% over the past five years, reaching $123 billion last quarter (Slide 7). Loan growth has exceeded deposit growth since late 2021, but the growth rate has slowed in the past year. Nevertheless, the three-year loan growth rate still surpassed deposit growth by 8% in the most recent quarter (Slide 8).

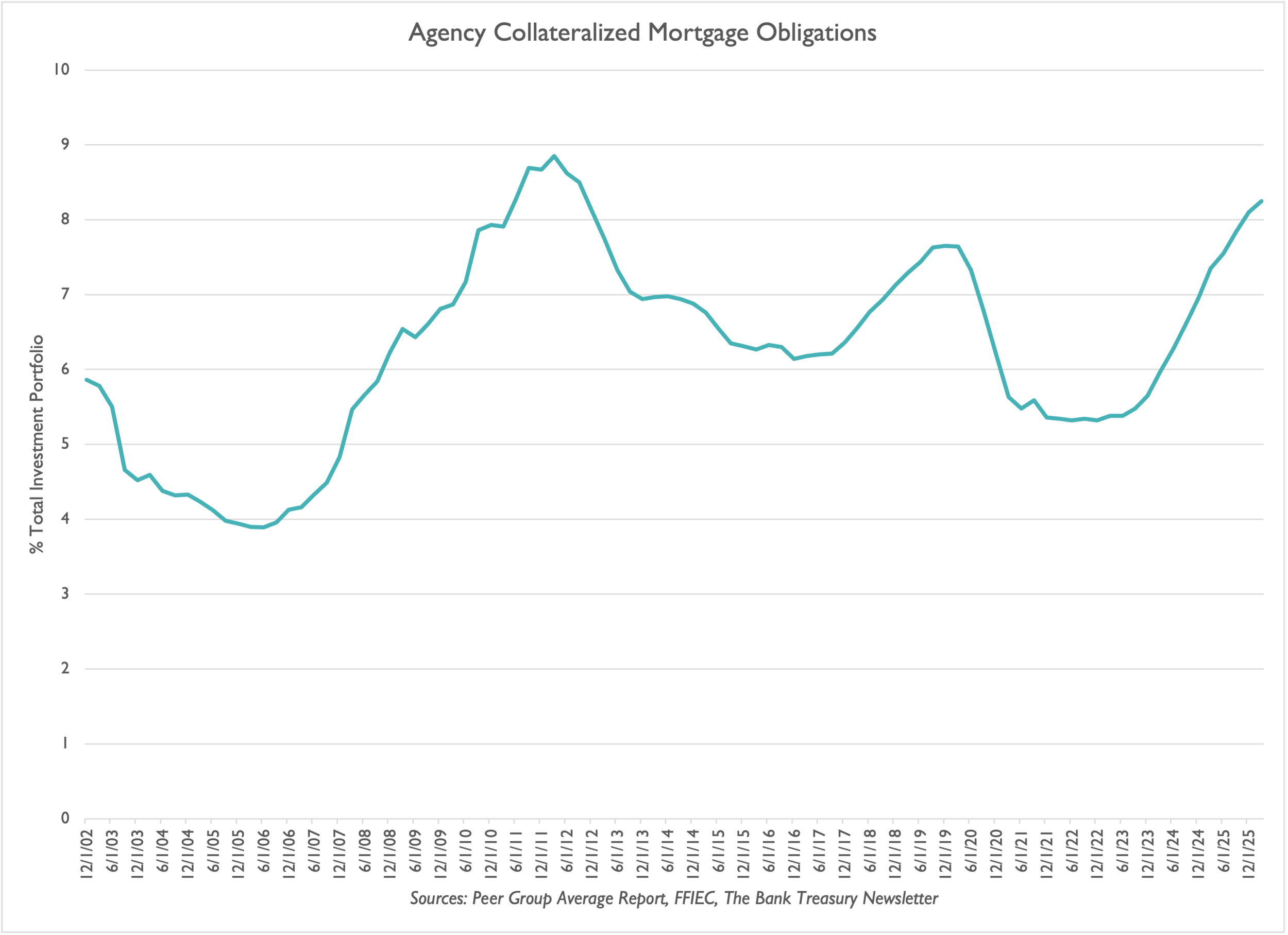

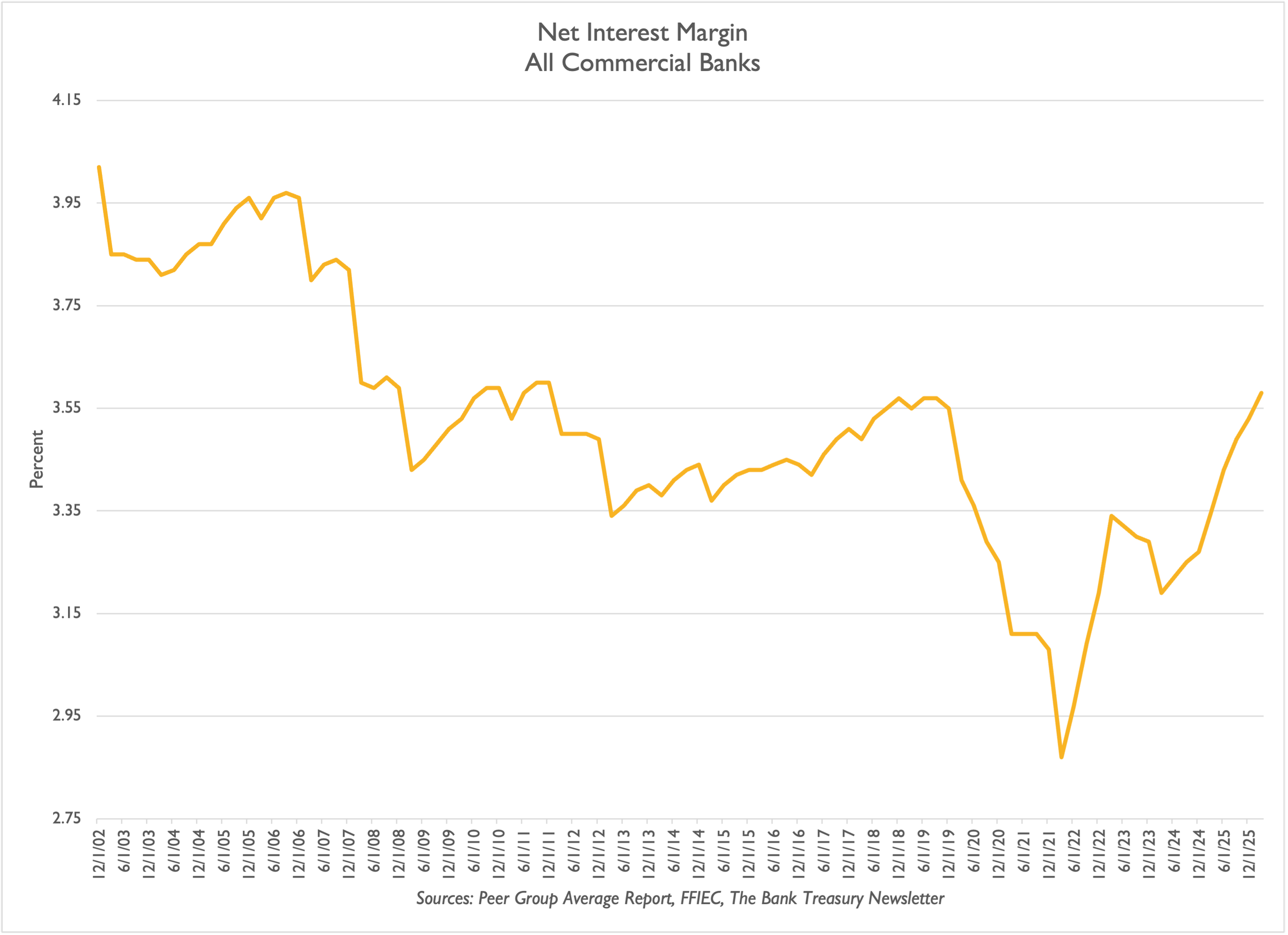

Banks continued to boost their concentration in interest-rate-protected short Agency CMOs last quarter, reaching 8% of their total investment portfolios—their highest level since 2012 (Slide 9). Meanwhile, after dropping below 3% in 2022, the industry’s average net interest margin (Slide 10) rose to 3.6%, the highest since 2010.

Stablecoin Transaction Volumes Have Soared

Token Supply Increasing To Meet Demand

Retail E-Commerce Topped $350 Billion Last Year

Stablecoins: A Growing Fractional Role In Retail

Quarterly FedNow Activity Is Leveling Out

An Ag Lender Failed This Month

Banks Ramp Up Farm Lending

Loan And Deposit Growth Coming Into Balance

Banks Increase Their Concentration In CMOs

NIM Is Back To Its Pre-COVID Level