BANK TREASURERS SEEK SHELTER FROM THE STORM

Kevin Warsh, nominated by the President to chair the Federal Reserve after Chairman Jerome Powell’s term ends next month, sat down with the Senate Banking Committee this month for his confirmation hearing. Polymarket bets on his confirmation by May 15 ticked lower after his hearing concluded, following two hours of questions from Senators. Notably, the Department of Justice dropped its case against the Fed on April 24th, presumably clearing the way for his confirmation.

The American people learned a lot from the nominee about sock puppets. He demurred from offering a view on the outcome of the 2020 presidential election, renovation cost overruns on the Eccles Building, and the right of Presidents to fire Fed governors, other than to say that the Fed would not be in the trouble it is in if it had done a better job with monetary policy. But he was vocal about his commitment to Fed independence from political influence, his desire for the Fed to be less candid in public speeches, and a return to the days before forward guidance, which bank treasurers already know is less than useful or reliable.

He disdained the current size of the Fed’s balance sheet and ripped the mistakes he believes it made in monetary policy since he resigned his governorship in March 2011 to pursue a career in the private sector. He was generally scornful of FedNow, the Fed’s new instant payment service, calling it outdated, but had no comment on the Fed’s announcement this month to expand the service by letting community banks and credit unions, which are not set up to use it, connect through intermediaries. Here are five questions that bank treasurers might have asked if they had participated in the hearing this month:

1. On the eve of the Global Financial Crisis (GFC), when you were a sitting Fed governor, the U.S. Treasury held approximately $5 billion in the Treasury General Account (TGA) on the Fed’s balance sheet. Nowadays, that balance averages around $600 billion, more than double its pre-COVID level, and varies by about 50% throughout the year as tax payments arrive and payments are made. Do you consider reducing the TGA a crucial step in plans to shrink the Fed’s balance sheet? Would you prefer that the Treasury keep its money in commercial banks or invest it in the Treasury repo market to achieve this goal? If TGA funds were moved to these alternatives, would the resulting volatility pose risks to money market stability?

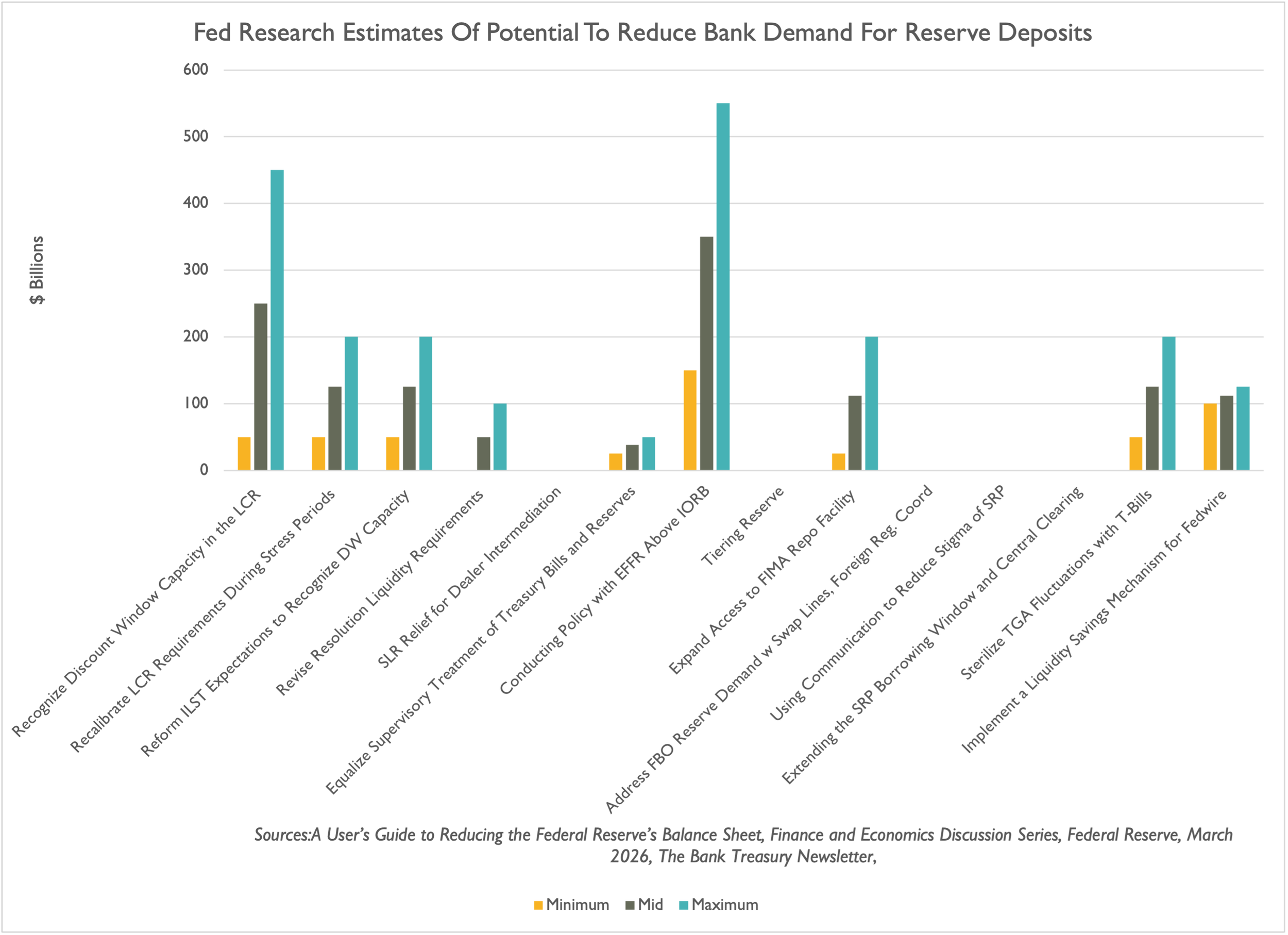

2. According to research that Fed Governor Stephen Miran co-authored last month, if regulators equalized the supervisory treatment of Treasury Bills and reserve deposits for liquidity requirements, they could reduce banks’ demand for reserves by between $25 billion and $50 billion. Do you think that a 3-Month T-Bill and reserve deposits provide the same level of liquidity for a bank treasurer in a stress situation? How much of a stablecoin reserve should a bank invest in T-Bills instead of reserve deposits, or are you indifferent between these alternatives?

3. Late last month, bank supervisors proposed recalibrating the Simplified Supervisory Formula Approach for the senior tranche of a non-Agency guaranteed securitization, lowering the floor from 20% to 15%. However, they did not address the risk weight for Agency mortgage-backed securities (MBS), which is 20% for risk-based capital. Do you think the senior tranche of a non-Agency guaranteed securitization poses less credit risk than MBS guaranteed by Fannie Mae or Freddie Mac, or do you think the omission of Agency MBS risk-weighting was an oversight? If the latter, do you worry that, in the haste to draft proposals to reform capital and liquidity regulations this year, there might be other errors in the proposals that were already published?

4. Bank supervisors are exploring ways to reduce the stigma associated with the discount window, aiming to encourage bank treasurers to view it as a dependable source of contingency funding. However, this stigma has persisted for 100 years. Why do you think the Fed will be more successful today in shifting perceptions about borrowing from the window? How much credit for liquidity purposes should supervisors give banks for their untapped discount window lines? Should untapped lines with the Federal Home Loan Banks (FHLBs) also qualify as High-Quality Liquid Assets (HQLA)? According to Fed Governor Miran’s research (hyperlinked above), adjusting the LCR to account for the discount window alone could reduce banks’ reserve demands by $50 billion to $450 billion.

5. Bank treasurers would ask one final question (even though they likely have more). Since you disclosed owning equity in several crypto companies, do you believe stablecoins pose a risk of siphoning deposits from banks? While the “Guiding and Establishing National Innovation for U.S. Stablecoins” Act, otherwise known as the GENIUS Act, specifically prohibits stablecoin issuers from paying interest to stablecoin holders, bank treasurers worry that nonbank issuers could circumvent the prohibition by offering holders discount coupons. What do you think of the research the White House published this month, which dismissed concerns about stablecoin yields that they would not affect banks?

The banking industry reported Q1 2026 earnings this month, and the basic message from bank executives was that, despite the war and the macroeconomic concerns it has raised, the opportunity to generate returns for shareholders remains good. Bank executives are optimistic about loan and deposit growth, still generally have faith in consumer strength, and expect their institutions to report improving net interest margins (NIMs) through the year as more of their balance sheets reprice, regardless of whether the Fed cuts rates this year or stays pat. Looking for ways to improve shareholder returns through artificial intelligence (AI) projects remains front and center, and credit weakness in lending remains within the range of normal seasoning. However, given ongoing uncertainty, bankers expect to remain conservative about reducing capital and liquidity positions this year.

The Bank Treasury Newsletter

"Twas in another lifetime, one of toil and blood. When blackness was a virtue, the road was full of mud. I came in from the wilderness, a creature void of form. 'Come in,' she said, 'I'll give ya shelter from the storm.'”

Dear Bank Treasury Subscribers,

Okay, okay, the connection with Bob Dylan and bank treasury is a stretch. Not going to argue. The character who was singing was bummed out over a personal breakup and looking for a little comfort, a little salvation. Obviously!

He definitely did not have gold, the almighty US dollar, Treasury bills, reserve deposits, or any other liquid assets in mind when he was singing about someone offering him shelter. And, obviously, April and taxes were not on his mind, either.

For that matter, back in 1974 when he recorded the song, he was not thinking about a war (at least not the one in Iran), interest rate policies, economic outlooks, or anything else that our subscribers worry about at every moment when they catch a chance to break away from the chaos. Nope. He was not looking to escape market volatility, the credit-deterioration story, a slow-motion run on private credit, nor AI’s all-knowing eyes and ears.

He had never heard of stablecoins, could never have imagined tokenized deposits or instant payments (because banks did not even have ATMs back then), nor would he have used the word “digital” much in his daily conversation. Retail was still a good trade, and people continued to buy things in department stores the way their ancestors had. Online meant a physical telephone wire hanging from trees, not a radar sign on a computer screen, which did not exist then either. We get it. A completely different context.

But as your editor-in-chief likes to tell his readers, look at something long enough, and pretty soon everything sounds like a page out of the life of a bank treasurer. And maybe there is no need to apologize for our metaphorical stretches. A bank treasurer’s day is all about toil and blood, as well as sweat and tears, at least metaphorically, though some of it is for real, too. Toil, for sure. The bank treasurers we talk to give their life and soul to their jobs, work long hours, and let their bosses take the glory for their work, reassuring investors this month, as they had before, that they are neutral and have no reason to fear uncertainty or what happens to NIMs with higher for longer.

And the idea that blackness was a virtue! Come on! Bank treasurers always understand that, despite how dire things seem, they can always get worse, and you’re damned if you do or don’t. Their job involves getting their hands dirty—maybe not with mud, but with numerous inconclusive numbers on spreadsheets that muddy their forecasts, cloud their decision-making, erode their confidence, and hold up crucial projects as they wait for one more data point to decide whether to pull the trigger on a new investment or pull the plug on an existing one. This is their daily reality of inconclusion and deciding despite it.

Bank treasurers today find themselves lost in the wilderness, blinded by a nonstop blizzard of information and numbed by so many shocks that they are on the verge of overload. They no longer even look for an exit sign or a lit path out of the chaos. What good is past experience when nothing like this has ever happened before?

Nothing shocks them anymore. Nothing shocks any market participant. In the midst of uncertainty and macroeconomic turbulence, equity market indices are gliding serenely ever higher, credit spreads are even lower, all driven by the theme that there is an end in sight to conflict and that everything is going back to the way it was before Liberation Day last year or at least February 28th this year. Cue the magic wand.

To think it all began with Liberation Day a year ago this month, and little did bank treasurers know then, much less suspect what they know today, and even more so fear what they will know tomorrow, how every day sounds scarier and scarier, and more and more overwhelming? There is just so much news, developments by not just days, but by hours, minutes, and hair-raising developments about civilization and survival playing down to the wire.

Between court decisions on tariffs, budget stand-offs, war and peace negotiations, AI-misinformation, cyber-attacks, high-profile Trump Administration turnover, on-line betting parlors for the news of the day, Fed criminal enquiries, stories of civil unrest and disquiet, the curious case of Kevin Warsh and his road to the Fed chair, the Ukraine war, stories about climate-themed catastrophes including fires, heatwaves, coldwaves, floods, tornadoes, hurricanes, droughts, and who knows what upsetting man’s carely laid residential neighborhoods and insurance calculations, how does anyone sleep? And, if that is not enough to toss and turn over, how about the possible existential threat from the non-deposit financial industry?

Taking in the news of the day is like drinking from the proverbial firehouse. A warm bed for the night, even if you have to go back into the chaos the next day, does not sound so bad.

“Not a word was spoke between us, there was little risk involved. Everything up to that point had been left unresolved. “Imagine a place where it's always safe and warm," she said. “Come in,” she said. “I'll give ya shelter from the storm."

A Shelter for a Shaky Dollar

In the news this month, the Treasury projects it will spend over $1.3 trillion in fiscal 2026 on interest on more than $31 trillion in marketable national debt. Okay, our readers tell us, the world will survive, whilst looking past eye-popping numbers, numbers suggesting that the country’s fiscal path is unsustainable. Numbers flashing that catastrophe awaits, numbers used to support theories that the U.S. dollar will lose its reserve status, and that Petro-Yuans will replace it, and that Mr. Money Market will soon teach the U.S. Treasury a lesson it will not forget.

Chaos challenges the assumptions on which their confidence rests and validates concerns that the dollar’s status as a reserve currency is neither permanent nor guaranteed. Those assumptions are that the U.S. is highly rated (even if it is no longer triple-A), has deep, liquid financial markets (which are becoming increasingly more volatile and subject to sudden illiquidity and dysfunction that requires rescuing by the Fed), enjoys political and economic stability (for now), and has a strong and reliable legal system (hopefully). Not that these assumptions are wrong or mean that bank treasurers should head to a bomb shelter, yet.

On the other hand, nothing is forever, not even a safe-haven like the dollar. Something has to be done soon to save Social Security. There is loose talk of doom loops, and even Henry Paulson, U.S. Treasury secretary during the Global Financial Crisis (GFC) and thus no stranger to financial crises, thinks the U.S. should prepare a plan in case disaster hits, and investors flee the Treasury market one day.

But the dollar is not fleeing anywhere. As Beth Hammack, the Cleveland Fed president, pointed out when she spoke last month to a forum on monetary policy, there is a good reason why the U.S. dollar’s safe-haven status is not changing anytime soon. The dollar has T.I.N.A. status, as in There Is No Alternative.

That is because the majority of global trade is in dollars; nearly 90 percent of every day’s $9.6 trillion in FX transactions involve US dollars, compared with the second-place Euro at 30 percent. Dollar reserves account for just under 60% of global reserve currencies, down from the early 2000s, when they were over 70%, but nevertheless remain the sole superpower in global financial markets.

Now, it is not impossible that the U.S. could one day be dethroned. The sun has set on other eternal empires. As Ms. Hammack continued,

“I hear from market participants that while investors may be reducing the proportion of dollar assets in their portfolios, they are still at a neutral or overweight level. But we should not take these allocations as permanent.”

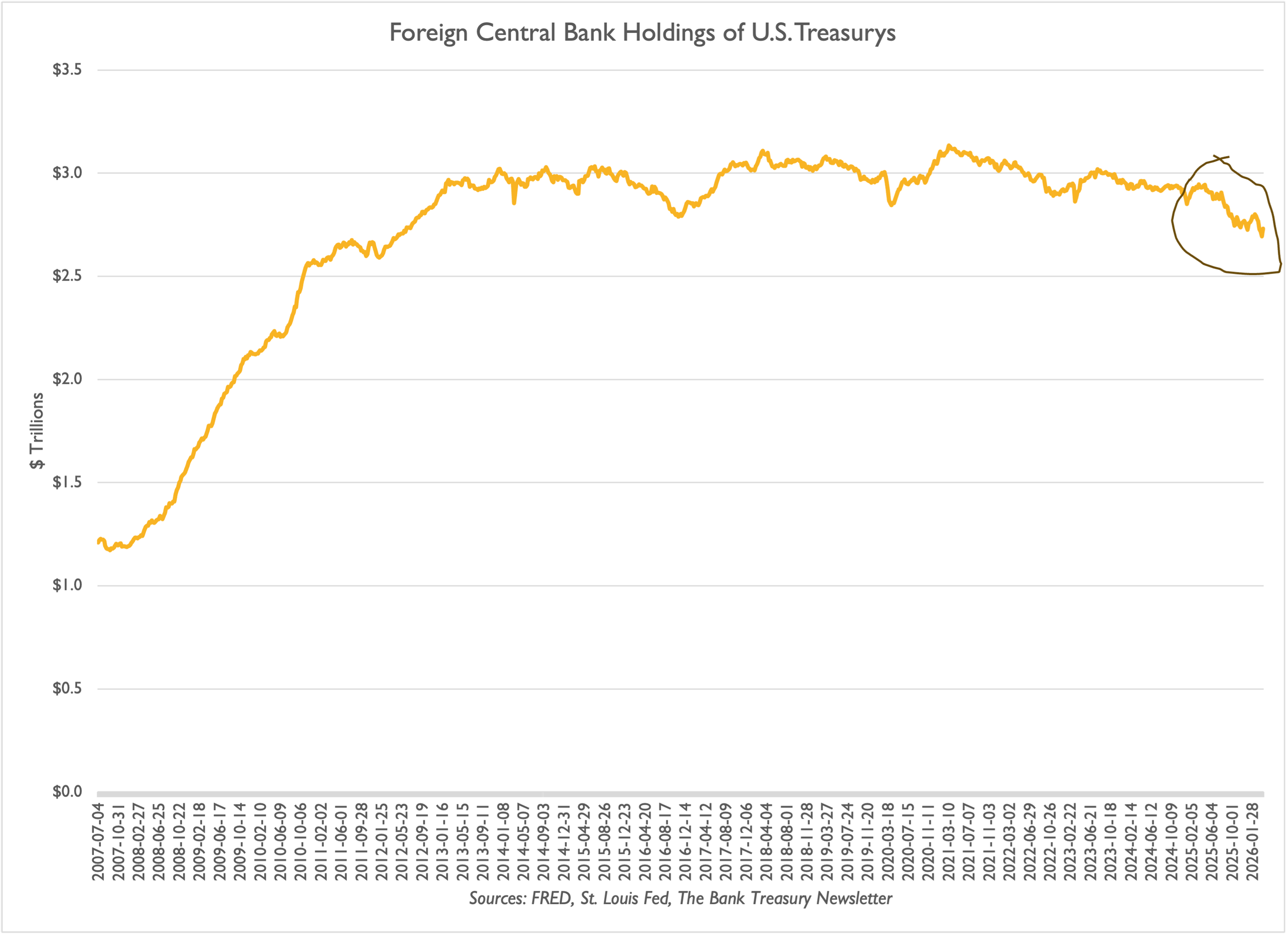

This time could be different. The Financial Times cited a decline in foreign central bank holdings of Treasurys at the New York Fed (Figure 1) as evidence that the war has so unnerved Middle East governments that they are selling their most liquid asset and diversifying away from the dollar. According to research published this month by the Dallas Fed, the war will go down in history,

“A complete cessation of oil exports from the Persian Gulf region would amount to removing close to 20% of global oil supplies from the market, about 80% of which is shipped to Asia. This makes the outbreak of the 2026 Iran War the largest geopolitical oil supply disruption in history.”.

Figure 1: Foreign Central Bank Treasury Holdings

It is hard to make sense of it all. Since the war with Iran began on February 28, as noted in research by the Richmond Fed, the dollar rallied, as usual, against the Euro and other major currencies, which makes sense. The dollar is every investor’s shelter from the storm. But Treasurys also sold off, which runs counter to the flight-to-safety playbook, and the data the U.S. Treasury reported this month, and is harder to square with the basics of the dollar and a carry trade.

You buy a currency to buy assets denominated in that currency. If you buy dollars to protect your wealth, you immediately want to turn around and invest your dollars in the safest interest-earning asset out there: U.S. Treasurys. It is non-negotiable for investors who do not want to just sit in cash that earns nothing. Which means that when the dollar appreciates, so do Treasury prices.

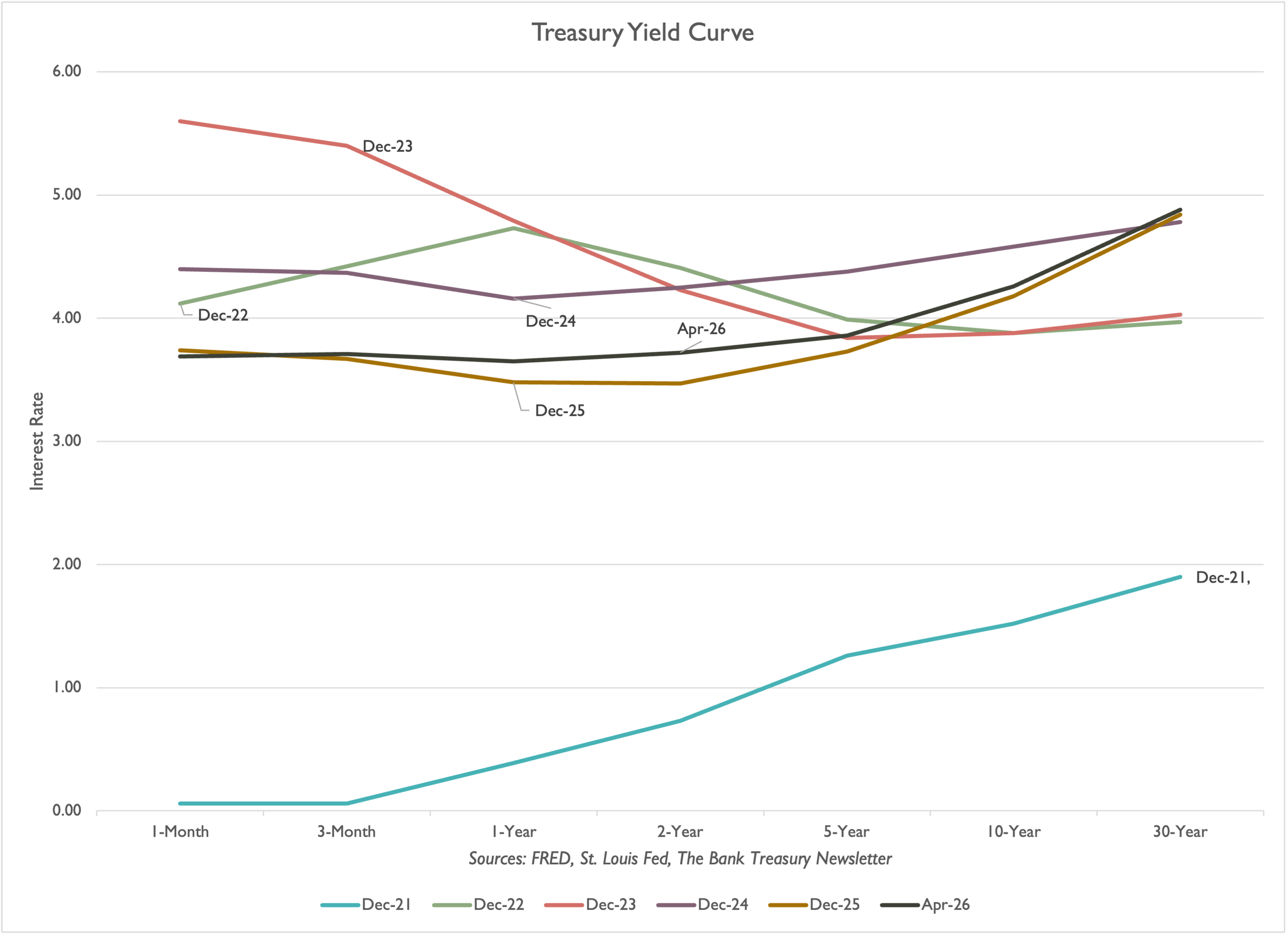

But curiously, or worrisomely, not this time. The 10-year Treasury jumped 40 basis points from just under 4% on the first day of trading after the war began and remains 20-30 basis points higher than before the war. Indeed, the entire yield curve bear-steepened, and no part of it is inverted for the first time in four years since the Fed began tightening in March 2022 (Figure 2).

Perhaps, if it had not been for the dollar’s status as a safe-haven, Treasury yields would be even higher than they are now. Until the market gets a better sense of the direction of monetary policy and the future for prices and employment, a sustained rally in the Treasury market is probably off anyone’s negotiating table. For now, the 30-Year Treasury bond yield remains under 5%. Markets remain far from the shocks that roiled them in the past. The first 30-Year Treasury Bond the Treasury ever sold was in 1977, in the wake of the OPEC oil embargo that Middle East oil producers launched against the U.S. because of its support for Israel during the 1973 Yom Kippur war. It paid a 7.75% coupon.

Figure 2: Treasury Yield Curve, December 2021-April 2026

Everything is Fine

Everything is fine, or will be, provided everything goes back to normal very soon. Okay, people are cautious according to the Fed’s Beige Book, but bankers reporting earnings results for Q1 2026 were not seeing a pullback anywhere. Consumer confidence is weakening, and mortgage applications have fallen since the war began, but everything will be fine.

And the thing is, everything is fine—for now. Everything is fine, as bank executives told the bank analyst community this month and took questions about their banks’ earnings. And the truth is, markets will be fine, provided everyone continues to trade and does not run for cover. According to the chairman of the board (COB) and chief executive officer (CEO) of a global bank, the CEOs he talks to are not seeking shelter. They want to make money, which is why mergers and acquisitions (M&A) are booming,

“The environment for Investment Banking activity continues to be incredibly robust, particularly M&A activity. And I do think, as I talk to CEOs, of course, they're watching what's going on geopolitically. But that's also balanced by the fact that they see an opportunity during this period to drive scale and scale creation in businesses undergoing significant technological change, and they are focused on that. And that candidly trumps some of the geopolitical risk, as they could do consolidating trades. And you saw that in the first quarter; you saw more large-scale strategic M&A.”

And, as he went on later to say, there is money to be made, even in the private credit space, which has seen several high-profile losses lately,

“If you take a very tough cycle, the GFC, the cumulative default rates across the entire leverage lending space during the GFC was 10%, recoveries were about 50%, so the cumulative loss was 5% to 6% against coupons of 9% to 10%. And so that is the business model. I think institutional investors understand that.”

Maybe this is no time to put the pedal to the metal, so to speak, but it is also no time to head to the shelters. Not when there is money to be made. The COB and CEO of a major asset management firm said even his firm’s clients in the Middle East were not blinking,

“Specifically in the Middle East, we have not seen any change in behavior…We have not seen any withdrawals from sovereign funds…Obviously, things could change if there's prolonged uncertainty and violence in the region.”

Business spending is doing amazing, and the way commercial borrowers are stepping up for loans, the COB, president, and CEO of a regional bank based in the southeast, mused, makes you think rates were back at 0%.

“The pipelines in commercial and industrial (C&I) continue to be very good. And while the short-term effects of the disturbance or the trouble in the Middle East have prompted questions, it has not had a significant downward impact on C&I pipelines at this point. And, in fact, we still see a continuation of what we saw building in twenty-five: business owners and leaders looking to grow, invest, and build…Commercial real estate (CRE) pipelines have continued to build…We haven't seen pipelines this strong since 2021-22 when rates were zero…We're very optimistic that the economy is still in a pretty good place, and that over the next several weeks to months, we'll start to see some of this uncertainty settle down.”

Pipelines are performing well, according to the CEO and COB of a large East Coast regional bank,

“We're very optimistic given the strength of the franchise, the likelihood that people want to transact. But…you could see people pull to the sidelines, wait for the opportune time, for example, to go to market…We're certainly not taking our numbers down for the year. In fact, we feel quite good about that, given the level of activity that we see and the pipeline strength that we have.”

The chief financial officer (CFO) from a global bank was very pleased with how well consumers were doing. While it might be too soon to tell what happens when Middle America learns to live with $4 gas at the pump, especially if it persists through the summer and into next fall’s Midterm elections, he told analysts that as long as people are employed, they are going to keep spending and paying their bills on time (for now).

“The biggest single reason that the consumer credit performance is healthy is that the labor market is strong. And if you get bad outcomes in the Middle East, much higher energy prices, or other problems, that will eventually fracture what has been…I think, a surprisingly resilient American economy and a very resilient U.S. consumer…But right now, in the end, the story remains the same, the consumer is doing fine despite higher gas prices.”

The COB, president, and CEO of another global bank was also optimistic about the consumer based on what he saw halfway through this month, when his bank reported quarterly earnings.

“The question will be, will wage growth continue…And you look, and it's growing everywhere at a faster rate…and so the spending ought to be there…And I know people say I’m being optimistic. But I'm telling you what we see today in the spending numbers, even into early April.”

But the story with the consumer is confusing. The New York Fed’s latest surveys suggest that households are growing more worried about employment, less optimistic about wage growth, and less inclined to spend their hard-earned money. New York Fed president, John Williams, made the same observation this month, speaking at a symposium hosted by the Federal Home Loan Bank of New York, noting that,

“Lately, the labor market has been displaying conflicting signs. In recent months, much of the hard data points to stabilization in the balance between supply and demand, while some soft data suggest a labor market that continues to soften gradually.”

From his office on the East Coast, the COB and CEO of a large regional bank told analysts not to believe the headlines.

“Look, I don't know that we can square for you the headline surveys on consumer confidence or small business confidence, which are all not great, how we square that with what we actually see. So when you look through spending patterns, growth in savings, activity levels, loan growth, everything we see day to day in our business is almost at complete odds with the surveys you see on confidence.”

Shelter Basics: Rule Number One and the Discount Window

I was burned out from exhaustion, buried in the hail. Poisoned in the bushes and blown out on the trail. Hunted like a crocodile, ravaged in the corn. "Come in," she said, "I'll give ya shelter from the storm.”

“Come in,” she said, “I’ll give ya shelter from the storm.” Doesn’t that line almost sound like, “Come in,” Powell said, “I’ll pay you interest on your reserves.” A little bit, no? Okay, let’s let that grow on you.

You do not need to worry about shelters when everything looks great, but that is no reason not to know where they are if circumstances go south this year. And no one is saying the far-forward rates will be realized, but the risk that they will is higher now than before the war. Bank treasurers are in for more supply shocks and face rising Federal deficits, and these contingencies cannot lead to happy endings.

Now, there are two basic rules to keep in mind when it comes to shelters. Rule number one is that you have to be in the shelter when the bombs are flying to get any protection. Otherwise, you are wasting your time. Theoretical shelters do not cut it in an emergency. This means you need to have a plan of action to get into your shelter in what bank treasurers call a “contingency.”

The Fed’s discount window is, in theory, a bank treasurer’s contingency, the backup plan, the ultimate shelter from the storm. It is a place that will accept any collateral you have that no one else would take, even in a million years. As long as you are in generally sound condition, you can price your collateral and deliver it to the window; you can borrow against it for Primary credit, overnight or up to 90 days, in accordance with the Federal Reserve Act and Regulation A. No questions asked, even. That is the truth, and it is amazing.

And even if you are not in such great shape, the Fed still wants to help you out through its Secondary Credit Program. Because the Fed cares, and bank treasurers have personally told your editor-in-chief how nice the Fed folks were on the line when they called them during the regional bank crisis three years ago. No kidding!

Maybe the loan will be for a shorter term than you would get under Primary credit, and maybe the clerk at the window will ask you questions about how you will use the money and how you will pay it back, but what is the Fed for if not to offer shelter from the storm? As the lender of last resort under Regulation A, the Fed even offers a seasonal credit program for small banks with total assets under $500 million that regularly face seasonal funding shortages in their markets.

But a lender of last resort is only helpful when you can use it, and most bank treasurers would agree with the statement, “I’d rather fail than borrow.” Nor is this anything new. The stigma attached to an institution that borrows from the Fed could be enough to put the bank out of business in an overnight run.

And it is not like the Fed issues a press release saying, “Hey, look at the loser bank that just borrowed from me.” But if your bank is one of just a few large banks in your Fed district (there are twelve, if you forgot) and one week your reserve bank reports a large increase in discount window loans, just as headlines in the financial press link your bank to credit issues in the economy, it would not be hard for one of your counterparties to put the proverbial two and two together, point an accusing fickled finger of fate at your institution, and yell, “J’accuse.” That could be the kiss of death and start a bank run.

When they failed three years ago, Silicon Valley Bank and Signature Bank were not prepared to use the Fed’s discount window because they had not tested their lines with the Fed and were not ready to move collateral to the discount window in an emergency. Their “next-to-lender of last resort” was their respective FHLB (there are eleven of those), which, unlike the Fed, can make loans only with funds they can access from capital markets, a limitation that certainly does not help if you are under siege, as Signature Bank was on a Sunday afternoon in March.

Given the sizeable runs the two banks experienced over a very short period, the discount window would not have served as much of a life preserver, even if they had been prepared to borrow from it. Supervisors unanimously believe that had these banks been better prepared, it would have helped reduce the cost of their FDIC resolution. Given the speed of the run (SVB lost 87% of its deposits over two days), being better prepared meant already having their collateral at the discount window, priced and ready to borrow against.

Hence, collateral prepositioning has been a major mantra for bank supervisors over the past three years. Though Miki Bowman, the Vice-Chair of Supervision, believes the push has gone too far and places too heavy a burden on the banking industry, there is no question that there are too many frictions for a bank treasurer in trouble who tries to use loan collateral to borrow from the discount window in a hurry with collateral that has not already been priced and prepositioned at the window.

But prepositioning carries an opportunity cost. Bank treasurers could preposition their entire balance sheets at the Fed if they wanted to, but they do not, because doing so would tie their hands if they want to use the collateral elsewhere. If you preposition collateral at the Fed, you cannot also preposition it at the FHLBs or with another backup lender at the same time, and then decide, based on terms, which “shelter” to go to for the night. You have to pre-arrange the couch you sleep on, so to speak.

You cannot even move collateral as easily from one place to another, say from the FHLBs to the Fed or even from one Fed bank to another, if it makes more sense to borrow from the Fed and your collateral is at the FHLB. Or maybe you want to use the collateral to borrow in the repo market, but now it's tied up at the Fed. Prepositioning, under the way the system works today, is a headache. And the haircuts the Fed charges are not competitive when times are good, though when times are not, they might seem too good to be true. The system is rickety and needs a major upgrade, as the Vice-Chair of Supervision has said.

Note that the Fed accepts all collateral that can be priced, which falls into two categories: securities and loans. Securities are generally easier to price and to use in the repo markets as an alternative for bank treasurers seeking short-term funding. Thus, bank treasurers who preposition collateral at the Fed generally use their loans, and probably only those that the FHLBs do not take, since the FHLBs are set up to support home mortgage lending.

In April 2024, the Fed published a report on the collateral banks and credit unions have prepositioned with the Fed, comparing loan and securities collateral balances at year-end 2021, 2022, and 2023. According to the report, 57% of the 9,537 banks and credit unions that filed call reports at the end of 2023 had the paperwork required to use their Federal Reserve Bank’s discount window, compared with 50% in both year-end 2021 and 2022. After the bank failures in 2023, banks increased their prepositioned collateral, which rose from $2.0 trillion to $2.8 trillion by the end of 2023, two-thirds of which was loan collateral. But the Bank Term Funding Program (BTFP) prompted bank treasurers to actually take funds from the discount window (at its peak, the balance topped $160 billion) because the Fed was effectively paying banks to borrow from it, given its generous terms.

According to a report by the National Bureau of Economic Research, the industry’s largest banks regularly preposition 28% of their unencumbered assets at the Fed. The researchers also showed that even the precautionary act of prepositioning collateral with the Fed, let alone borrowing from it, carries a stigma that bank treasurers are highly sensitive about disclosing. Banks that disclose how much collateral they have prepositioned at the Fed tend to fund more with uninsured deposits than banks that do not disclose their prepositioned collateral.

In January 2024, the Group of 30 published a report recommending that banks preposition collateral against their runnable liabilities. When he was Vice-Chair of Supervision, Fed Governor Michael Barr pushed to require banks to preposition collateral to at least cover the $8 trillion in uninsured deposits they hold. But bank supervisors today would rather first focus on fixing the plumbing to enable banks to move collateral efficiently and refocus bank supervision on the basics, which they believe allowed institutions such as Silicon Valley and Signature to get away with inadequate contingency funding plans and preparedness for so long. At a minimum, as regulators pressed in the wake of the failures, a contingency funding plan must be credible and demonstrably workable under stress.

Rule Number Two: Temporary Means Temporary

The second rule for shelters is that they are temporary: if I let you sleep on my couch tonight, you can have breakfast in the morning, but then you need to leave. Generally, bank treasurers respect the concept of temporary. They regularly leave about $3 trillion at the Fed overnight, but they are not happy about it. Domestic banks generally leave much less at the Fed than foreign branches and agencies, which have fewer options for deploying overnight cash (see Slide 2 in this month’s chart deck for more details).

Yes, bank treasurers are happy that the Fed pays them Interest on Reserve Balances (IORB) instead of requiring reserve deposits and paying them nothing, as it was before the GFC. But bank treasurers are not paid the big bucks (ha, they wish) for parking cash at the Fed! They would be much happier if they could find a better, higher-yielding place to park their cash than the Fed. Who wouldn’t?

Now there's a wall between us, something there's been lost. I took too much for granted, I got my signals crossed. Just to think that it all began on an uneventful morn."Come in," Powell said, "I'll pay ya interest on your reserves."

It is growing on you, no?

As in life, you have a choice between the couch and the floor for the night. You can leave your excess cash at the Fed or in your vault, for all anyone cares, but be advised that vault cash is generally not eligible as HQLA. Also, keep in mind that you need reserves to make payments via FedWire, which handles an average daily transfer volume of $4.6 trillion.

And if you happen to be the treasurer of one of those newly chartered trust banks that can issue a stablecoin, your stablecoin reserve can be held as reserve deposits at the Fed, in T-Bills maturing in less than 90 days, or in another bank. So you do have a choice of investment. But last February, the OCC published proposed rules to govern stablecoin issuers under the GENIUS Act, and one of the proposals would place significant limits on a bank treasurer’s ability to keep too much of the stablecoin reserve in any single bank deposit account.

Of course, if treasurers did not want to deal with the administrative headache of managing a stablecoin reserve across multiple bank accounts to satisfy an OCC diversification requirement, or with selling unmatured T-Bills to fund unexpected redemptions, they could keep all their stablecoin reserves in reserve deposits at the Fed. End of story. Yeah, you leave a few basis points on the table in IORB compared to the 3-Month T-Bill, but what price is there for speed of execution when we are talking about a currency designed for instant payment?

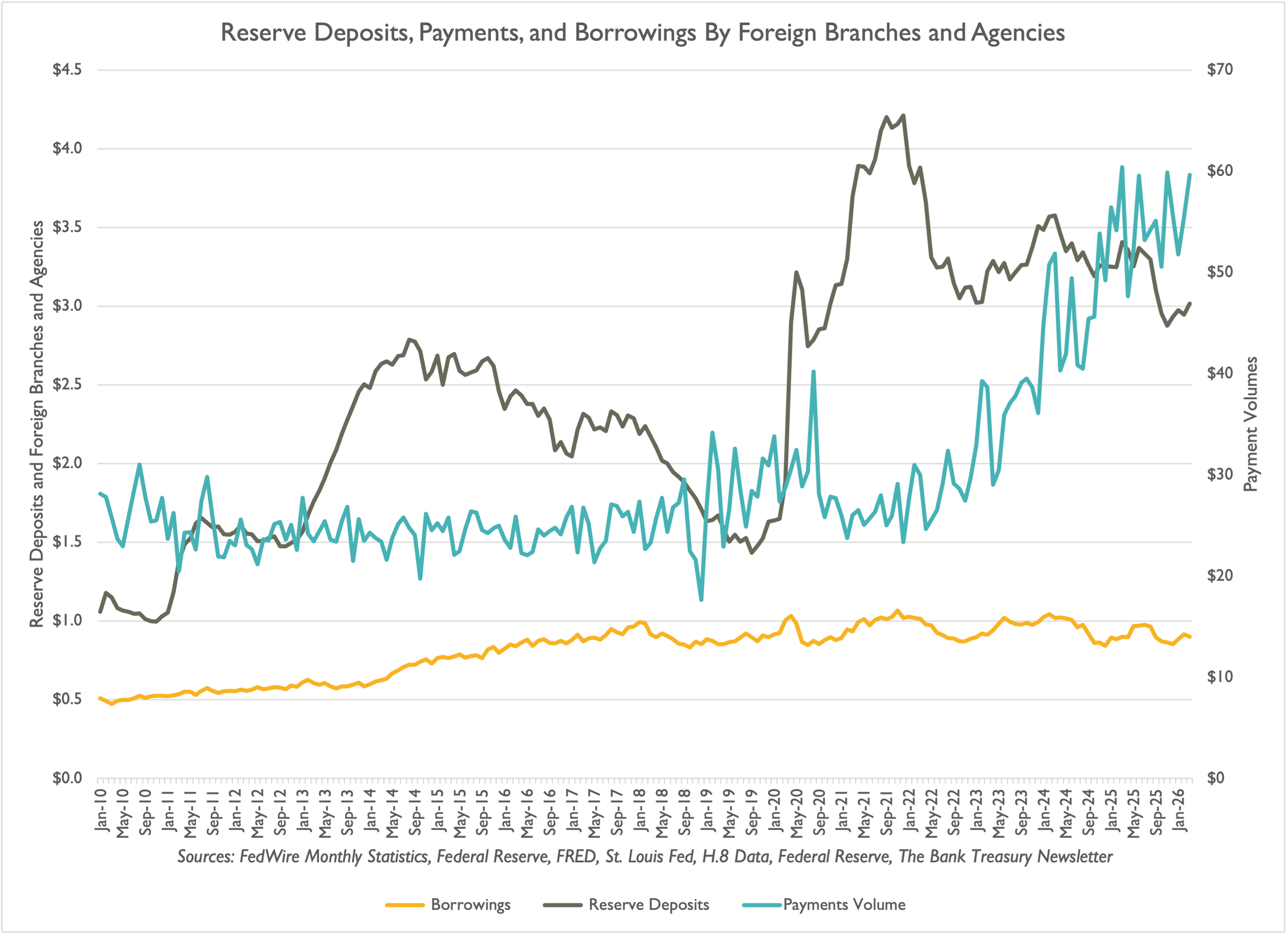

Bank treasurers may recall that after the Fed began paying interest on reserve deposits, foreign branches and agencies began leaving their cash at the Fed and arbitraging the interest earned against their borrowed funds in the Fed funds market, which in the 2010s ran a few basis points below IORB. Researchers at the New York Fed showed that in the decade after the Fed launched Quantitative Easing, payment volumes moved in line with the supply of reserves, and as the Fed increased reserves, payment volumes rose. But this relationship has been less clear since 2020, as the graph in Figure 3 shows: Borrowing by foreign branches and agencies in the Fed funds market, according to H.8 data, has been flat, even as reserves more than doubled and payment volumes soared.

Figure 3: Foreign Branches and Agencies Slowed Borrowings

Narrow Banks Violate Rule Number Two

When the Fed was paying 2.40% on reserve deposits, it received applications for bank charters from applicants proposing to accept customer deposits and leave them at the Fed at 100%. These institutions, which bank supervisors call Pass-Through Investment Entities (PTFI), otherwise known as narrow banks, would not make loans and would not even buy bonds, including Treasurys. Everything would go to the Fed as a permanent business strategy.

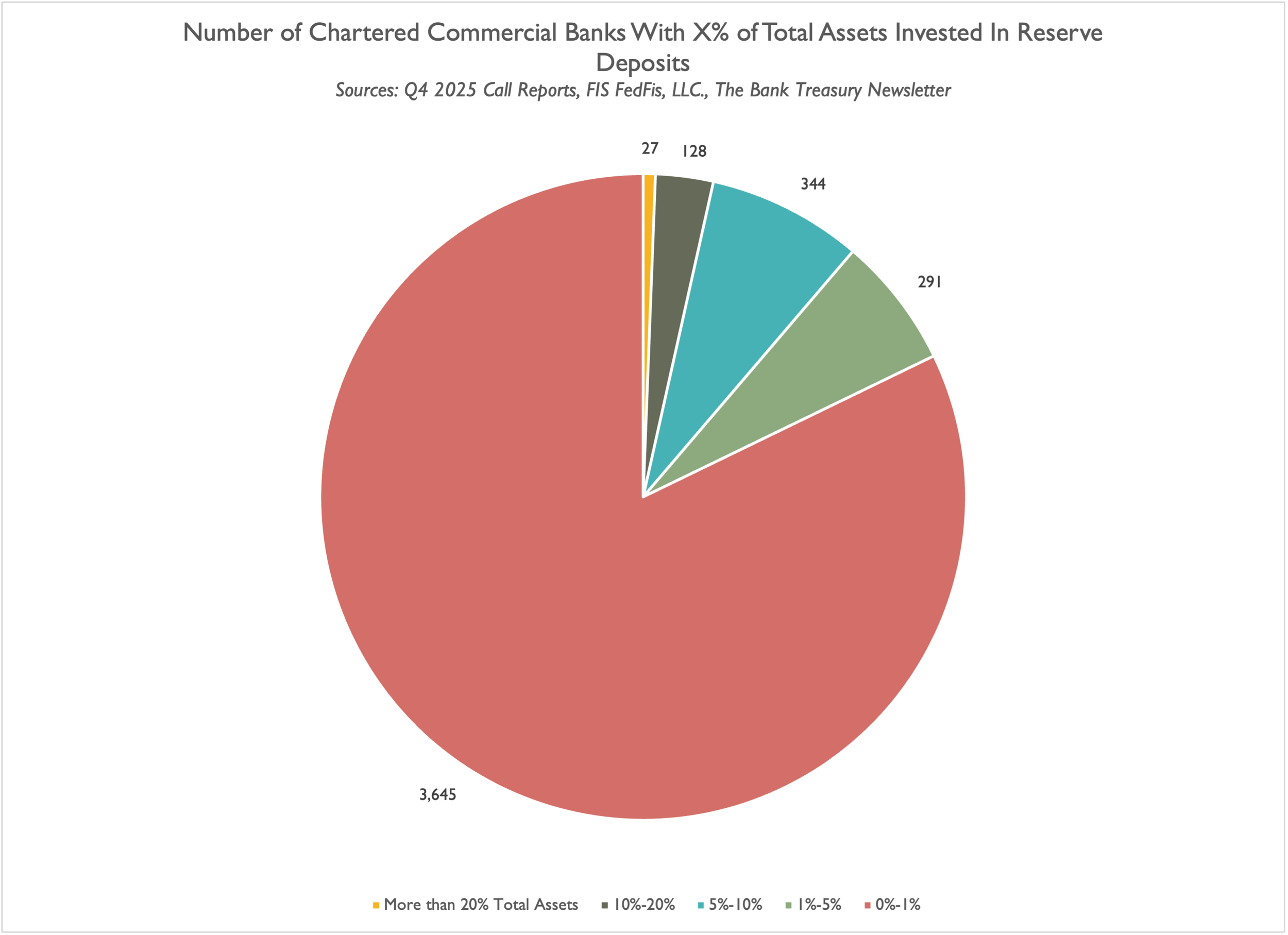

Strictly speaking, there are no narrow banks chartered to operate in the U.S. banking system. In aggregate, reserve deposits held by domestic banks at the Fed, according to the Q4 2025 call reports, amounted to 6% of their total assets, but a few dozen banks, ranging from small community banks to some global banks, hold multiples of that at the Fed. Holding the entire balance sheet at the Fed does not exist.

Notably, two years ago, the Fed turned down an application from the appropriately named “The Narrow Bank” (TNB) that proposed to do exactly that. Given that stablecoin-issuing trust banks are, in theory, like “narrow” banks, that bias may change. But in 2024, bank supervisors worried that narrow banks posed a risk to the financial system's stability.

And not because the bank proposed operating without FDIC insurance. Instead, they worried that in a financial crisis, depositors would withdraw all their deposits from traditional banks and place them in narrow banks, triggering a run on the financial system. The day after, the surviving traditional banks, lacking sufficient deposits, would be constrained from making loans, to the detriment of the economy.

Denying the application was not surprising to anyone who had been following the Fed’s views on narrow banks. In 2019, the Fed proposed a tiered system for paying interest on reserves, paying narrow banks less than it pays traditional banks, thereby eliminating the arbitrage that owners of these banks were earning from the Fed’s balance sheet. Traditional banks supported the Fed’s tiering idea, while the American Enterprise Institute argued that the proposal was “unconscionable” and an affront to American enterprise.

In the end, the Fed never finalized the proposal, and since there are no narrow banks, the concerns it raised remain theoretical. But Kevin Warsh would like to see ideas like tiering IORB used to help reduce the Fed’s balance sheet. Sadly, the topic did not come up during this month’s Senate Banking Committee testimony.

He is a proponent of the theory that the Fed’s balance sheet is too large, a view he shares with Fed Governor Stephen Miran, Treasury Secretary Scott Bessent, and other members of or those engaged with the Hoover Institute. If he could, he would reverse the Fed’s entire “ample” reserve policy, begun with Quantitative Easing during the GFC, and return to a world of scarce reserves. Maybe not right away, and maybe not all the way back to scarce reserves, but that would at least be his goals for the balance sheet.

In his view, the Fed’s balance sheet harms the economy by distorting markets through its bond purchases. Maybe market intervention in the middle of a crisis is forgivable, his thinking goes, but the Fed buying bonds when markets are healthy is not. If nothing else, it cannot help its political image to pay IORB to banks while losing money on its System Open Market Account (SOMA) portfolio, especially when the bulk of its interest payments go to the large banks.

Its 2025 statement shows that the gap between IORB and the interest the Fed earns on its SOMA portfolio is nearly even. In 2023, when Silicon Valley Bank was failing, the Fed was paying banks and money market funds more than $100 billion in IORB, more than it was earning on its bond portfolio. Cumulatively, since it first raised rates four years ago, the Fed has paid out $260 billion more in interest to banks and money market funds through the Reverse Repo Facility than it has earned. The hard part to appreciate is that the Fed incurred these net costs over four years, all to bring the inflation rate back to its long-term 2% target. After four years, inflation remains above 2% and could rise further due to oil prices and the war.

Instead of flooding the financial system with reserves during a crisis, the Fed could offer emergency lending facilities, as it did with the BTFP, and then shut them down when the emergency passes. Why do you need the programs to continue forever? On the other hand, a Fed study published last summer suggested that emergency lending programs have a downside of their own: they encourage moral hazard.

The anti-Fed balance sheet proponents argue that leaving a $4.4 trillion Treasury bond portfolio and a $2.0 trillion Agency MBS book to a government agency must have some effect on market prices, even if minuscule, given that quarterly trading volumes for Treasurys and Agency MBS were $1.3 trillion and $413 billion, respectively. The Treasury issued $8 trillion in new bonds in the first quarter alone.

Hard Truths About the Fed’s Balance Sheet

Shrinking the balance sheet will take time, as a note co-authored by Fed Governor Miran warned directly in its abstract on the front page. Shrinking the Fed’s balance sheet,

“…If undertaken, there are good reasons for moving slowly and gingerly, and to take steps to ensure financial markets are able to absorb the reissue of securities that roll off the Federal Reserve’s balance sheet.”

Regardless of how long Kevin Warsh, Stephen Miran, and Scott Bessent plan to take to shrink the Fed’s balance sheet, doing so requires a reckoning with some hard truths about the right side of it. Currency in circulation is one of those truths.

As bank treasurers well know, every line item on the balance sheet has to balance some other line item. If assets go up, liabilities go up. The Fed’s balance sheet is no different than any other balance sheet. Reserve deposits, which sit on the right side of its balance sheet, are necessarily always equal to the Fed’s SOMA portfolio on the left side of the balance sheet. Against its $6.4 trillion SOMA portfolio on the left, it holds $3 trillion reserve deposits on the right. The rest of the liability side of the Fed’s balance sheet primarily consists of currency in circulation and the Treasury’s checking account, the TGA.

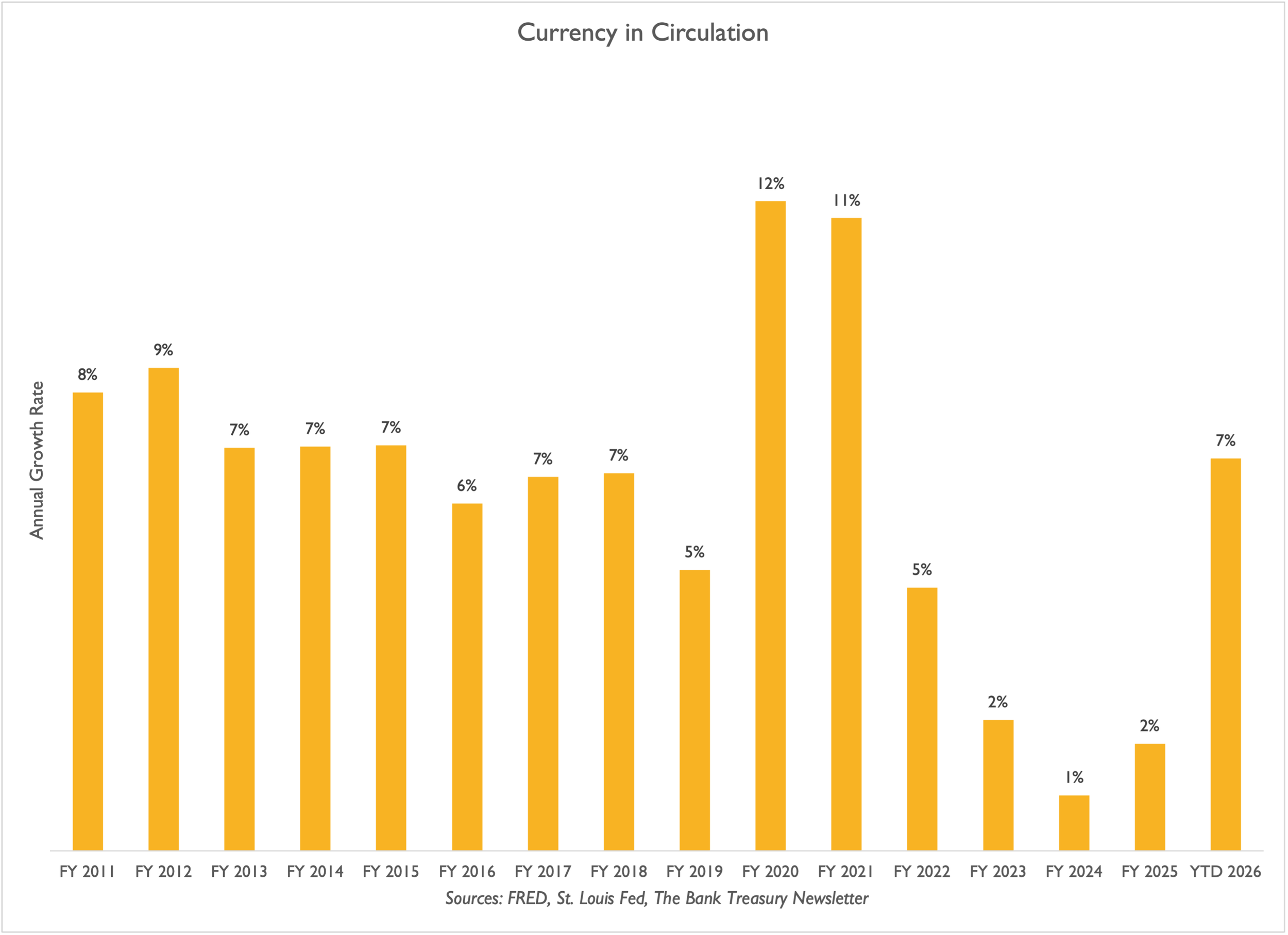

The hard truth about these two liability items is that the Fed has no control over them. Paper money stands at $2.5 trillion, and short of the Government eliminating printed money and declaring all money in circulation invalid unless immediately held in a bank, it will never shrink back to $800 billion, as it was on the eve of the GFC. It can slow the growth of currency, and countries such as Sweden are moving toward a cashless economy. Since $100 bills make up the bulk of the currency, the Fed could stop printing them as one way to at least slow the growth of currency in circulation, whose balance grew by 7% last year. Then again, as the Dallas Fed pointed out in research it published this month exploring a menu of options to shrink the Fed’s balance sheet, the downside of reducing paper money is the loss of seignorage revenue. Currency is an interest-free loan from the public to the Treasury, as it pays no interest and costs pennies to print.

Now, the Treasury could shrink its TGA, which Governor Miran and his co-authors believe could reduce demand for reserves by between $50 billion and $200 billion. But there are several hard truths to consider about shrinking the TGA. First, the Treasury now holds significantly more in its checking account than before the GFC, when it averaged less than $5 billion in 2007. Currently, the TGA exceeds $900 billion and averages about $600 billion.

While the Treasury might consider moving some funds to national banks, banks might resist the Treasury’s frequent shifts, especially during tax time. Additionally, if the Treasury deposits its cash with banks rather than directly with the Fed, the banks will need to return most of the Treasury’s nonoperational deposit “hot” money to the Fed anyway. The Treasury could shift money to the repo markets, allowing the Fed to shrink the SOMA portfolio; instead of the Fed manipulating interest rates, the Treasury would do so directly in the money markets.

Fed and Treasury officials are more optimistic that they can reduce the size of the Fed’s balance sheet simply by adjusting current capital and liquidity requirements. They are considering giving banks some credit for the discount window, recalibrating the stress scenarios banks use to calculate the Liquidity Coverage Ratio, equalizing the treatment of T-Bills and reserves, and adjusting leverage ratios, thereby, they estimate, reducing demand for reserves by $175 billion to as much as $1 trillion. But that would mean easing back on liquidity and capital requirements in the middle of a potential storm as the global economy heads further into the unknown. Bank treasurers may still want to hold more reserves than required, given the uncertainty and risks.

Payments and Hard Truths

“Well, I'm living in a foreign country, but I'm bound to cross the line. Beauty walks a razor's edge, someday I'll make it mine. If I could only turn back the clock to when God and her were born. "Come in," Powell said, "pay ya interest on your reserves."

One main reason bank treasurers might hold more reserves than required is to cover payments. If the Fed and Treasury want to reduce the Fed’s balance sheet, figuring out how to reduce the supply of reserves to support payments is key. Some of their ideas include moving payments on FedWire to a batch system, such as that used by the Automated Clearing House, which processes payments in a day rather than by the minute. They would also introduce Liquidity Savings Mechanisms (LSMs), which would allow banks to send payments without reducing their reserve balances on an intraday basis, as other central banks do in their payment systems. Fed researchers believe that LSMs could cut demand for reserves by as much as $125 billion, although, like the rest of their ideas, they remain untested in a system as large as the U.S. dollar.

Reforming FedWire is still only part of the challenge to reduce demand for reserves. If the stablecoins’ use case takes off in the international payments space, where annual volumes approach $1 quadrillion, demand for reserves will necessarily increase, per the OCC proposal, which will require issuers to hold Fed reserve deposits as a component of their stablecoin reserves. SWIFT just adopted new protocols to make uptake of stablecoins in international payments more likely, as it highlighted in its release this month, which it said will enable

“…the seamless exchange and settlement of tokenized bonds, while supporting payments in both fiat and digital currencies.”

One lesson the Fed and Treasury have learned the hard way is that payments and financial markets are intertwined and that disruptions to the supply of reserves can quickly lead to a crisis. A Brookings publication last month explained that whenever the largest banks active in the payments space start the day with low reserve balances at the Fed, they delay outbound payments via FedWire until they receive more inbound payments. This behavior can create logjams that then ricochet through the money markets and Treasury repo. In September 2019, a reserve shortage caused a sharp spike in Treasury repo rates.

Critically, reserve demand and the market’s sensitivity to supply are not defined by an absolute line that says $3 trillion in reserves is ample while $2.9 trillion is not. The study confirmed that the market’s sensitivity to reserve supply can be volatile, which leads to the hardest truth for central bankers. You need to be careful about reducing reserves, or even risk returning to the dark days before the GFC, when the Fed maintained scarce reserves, because this sensitivity is unpredictable:

“…the estimated sensitivity of Treasury repo rates (spread to the ON-RRP rate) depends on the quantity of reserves…As shown, this sensitivity can change abruptly.”

As Randy Quarles, former Fed Governor and former Vice-Chair of Supervision, conceded in a July 2022 interview, just as the Fed began to shrink the balance sheet for the second time under quantitative tightening,

“I just don't know that there's going to be that much appetite at the Fed for a materially smaller balance sheet. After September 2019, when... So, the Fed had been following the view that "The balance sheet needs to be as small as possible, but not smaller. And we don't know exactly what that size is. But we'll see it when we reach a kink in the demand curve as we begin to shrink reserves and the balance sheet. At some point, we'll see a developing slope in the demand curve, and we'll know that we're there. And then we'll kind of expand it back out a little bit." The disruption in September 2019, as we were shrinking the balance sheet, was significant enough that I think the general view on the FOMC became, "We don't want ever to get that close again," and a movement away from the view of, "Let's shrink it until we're absolutely as close to that kink as possible." It was, "Well, let's just make sure we've got plenty of cushion before that ever happens again."

Which brings us to rule number three: shelters can sometimes mean the difference between life and death, between a smooth-functioning, liquid Treasury market and a safe haven for international investors in the middle of a global macro-geopolitical, fiscal, and economic storm, and—well, you do not want to find out. As Mick Jagger of the Rolling Stones would say, “Ooh, a storm is threatening my very life today, if I don’t get some shelter, I’m going to fade away.”

The Bank Treasury Newsletter is an independent publication that welcomes comments, suggestions, and constructive criticisms from our readers in lieu of payment. Please refer this letter to members of your staff or your peers who would benefit from receiving it, and if you haven’t yet, subscribe here.

Copyright 2026, The Bank Treasury Newsletter, All Rights Reserved.

Ethan M. Heisler, CFA

Editor-in-Chief

This Month’s Chart Deck

Kevin Warsh discussed his views on monetary policy, Fed independence, and the balance sheet during his confirmation hearing. If confirmed, he aims to gradually shrink the Fed’s balance sheet. As shown on Slide 1, while the $3 trillion in reserve deposits has remained stable since 2022, M2 has continued to grow, increasing by $1 trillion to $23 trillion over the last 12 months. Most banks hold minimal reserves at the Fed relative to their total assets, as shown in Slide 2.

The Fed is exploring ways to reduce reserve demand on its balance sheet, which could lead to a smaller footprint, since reserve deposits account for nearly half of the balance sheet. Slide 3 reviews options for accomplishing this goal, like adjusting liquidity requirements and crediting banks for unused lines with the discount window.

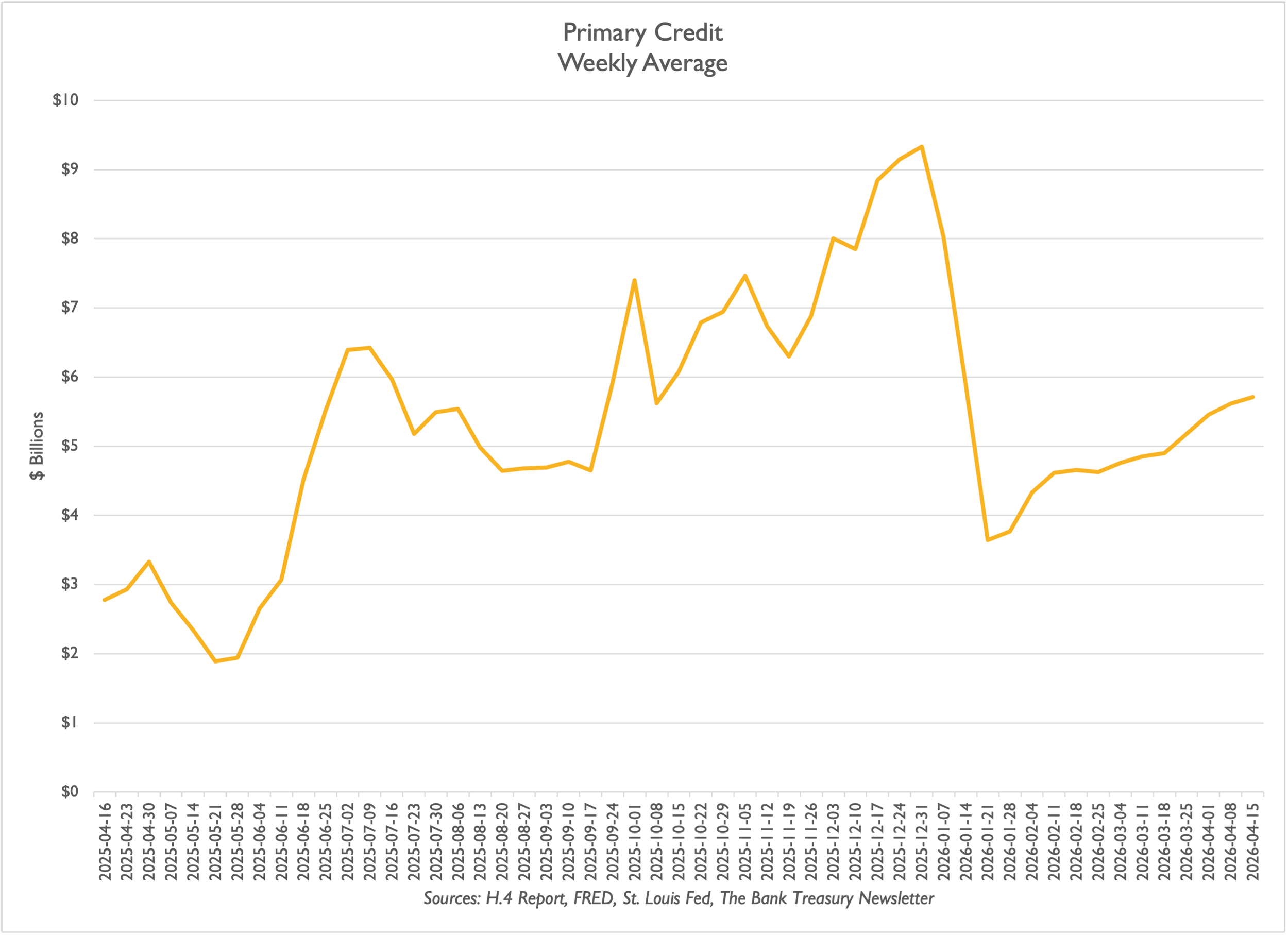

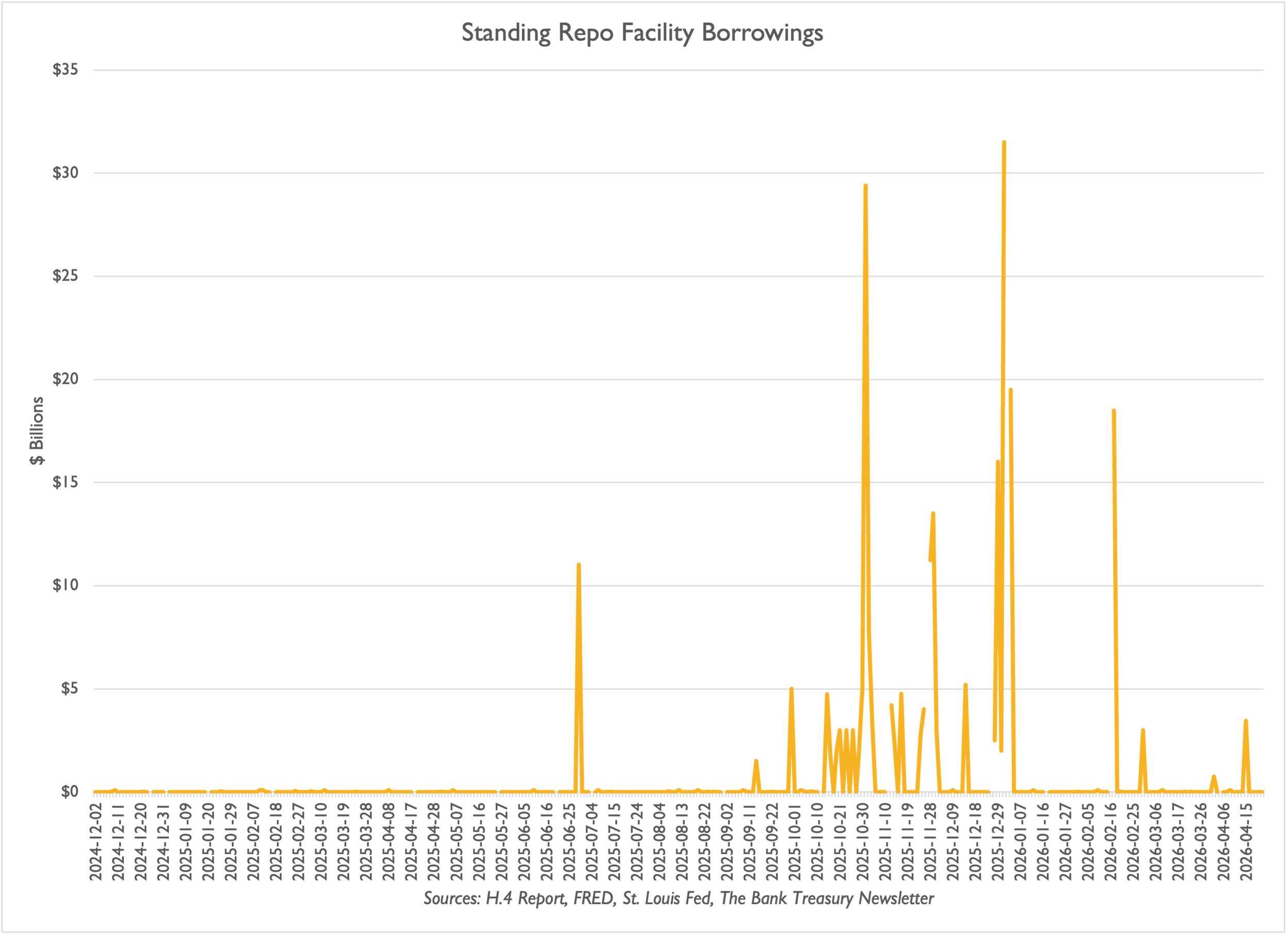

The stigma of borrowing from the Fed as a last resort discourages bank treasurers from using it for contingency funding, even as Primary Credit borrowings are up by $2 billion since the war began, to nearly $6 billion (Slide 4). The Standing Repo Facility (SRP), providing emergency funding to banks and nonbanks (Slide 5), has also seen increased use over the last six months.

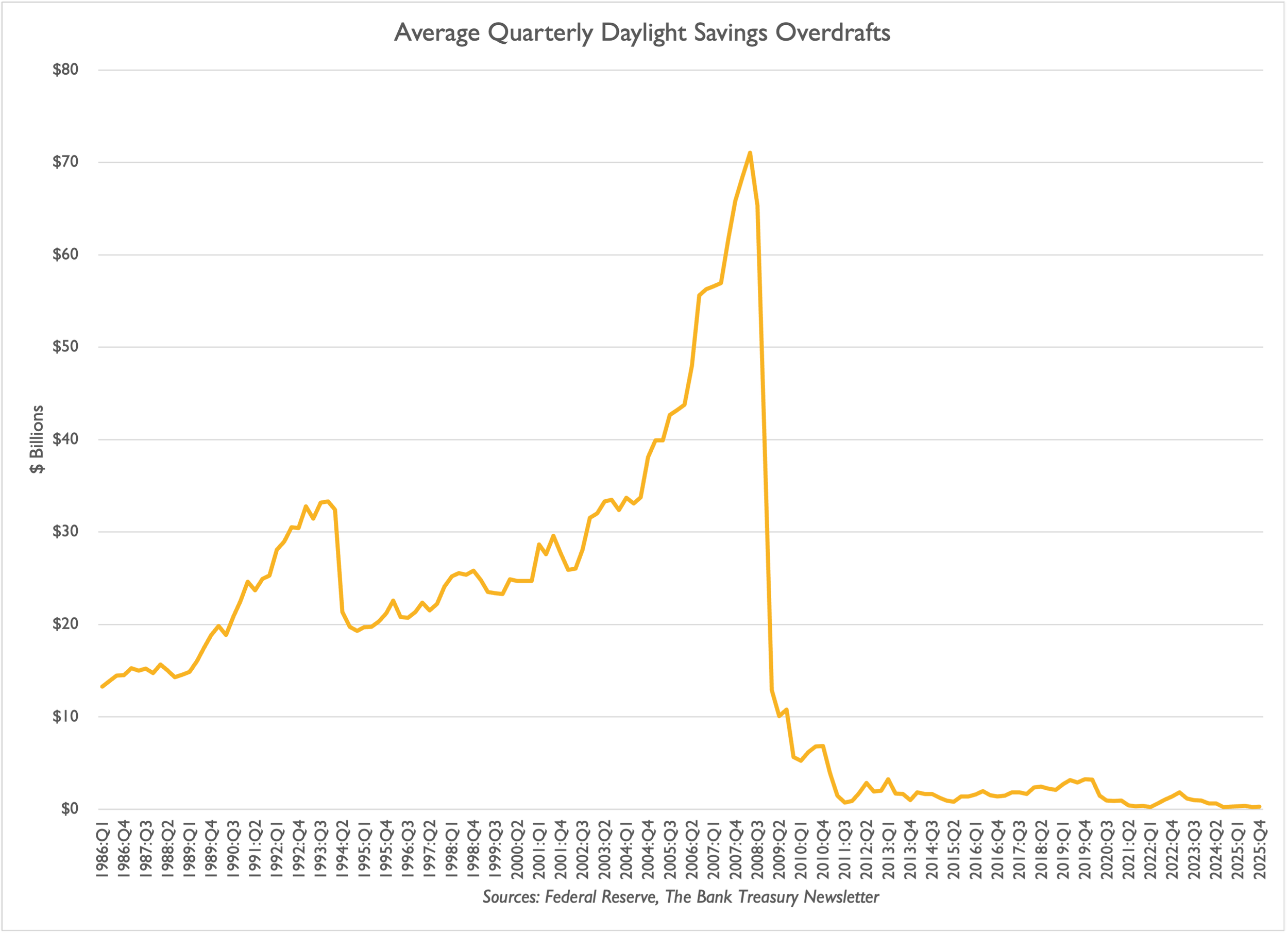

Conversely, banks rarely use daylight overdrafts (Slide 6) to cover shortfalls when making FedWire payments, a practice that was more common before the Fed expanded its balance sheet in 2008. Today, a bank treasurer with low reserves in the morning waits for incoming payments before making outgoing ones, which can cause jams and spike money market rates, especially in Treasury Repo, as happened several times, including September 2019, early COVID days, and March 2023, after Silicon Valley and Signature Bank failed.

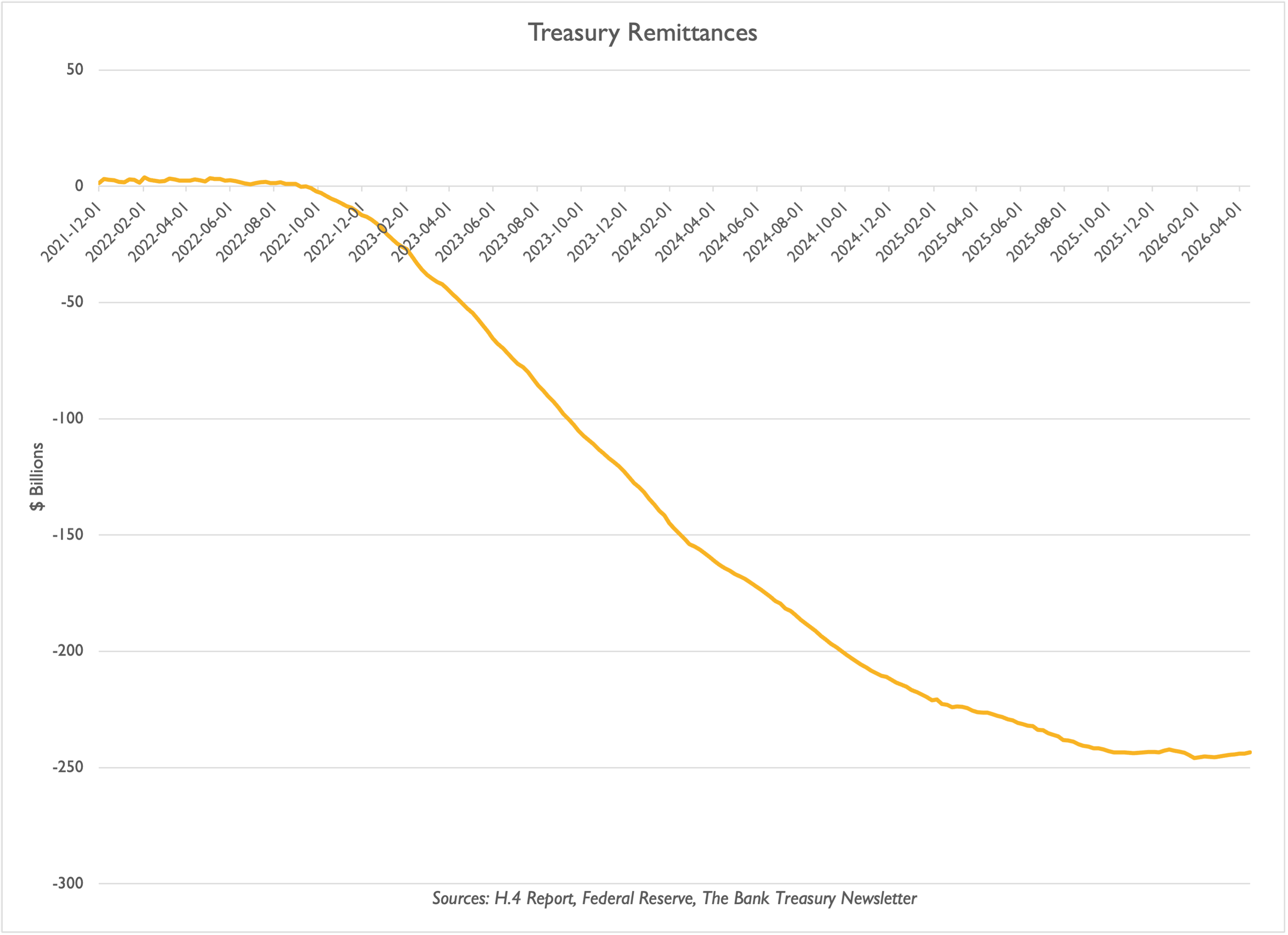

Negative Treasury remittances flattened out this year as the Fed broke even between the interest it earned on its bond portfolio and the interest it paid on reserves. However, the Fed still owes $260 billion to the U.S. Treasury due to negative remittances. Repaying these reduces reserve deposits. Currency, equal to $2.5 trillion, grew by 1% in FY 2024 and 2% in FY 2025, but leaped to 7% YTD in 2026. Every dollar of printed currency decreases reserves equally.

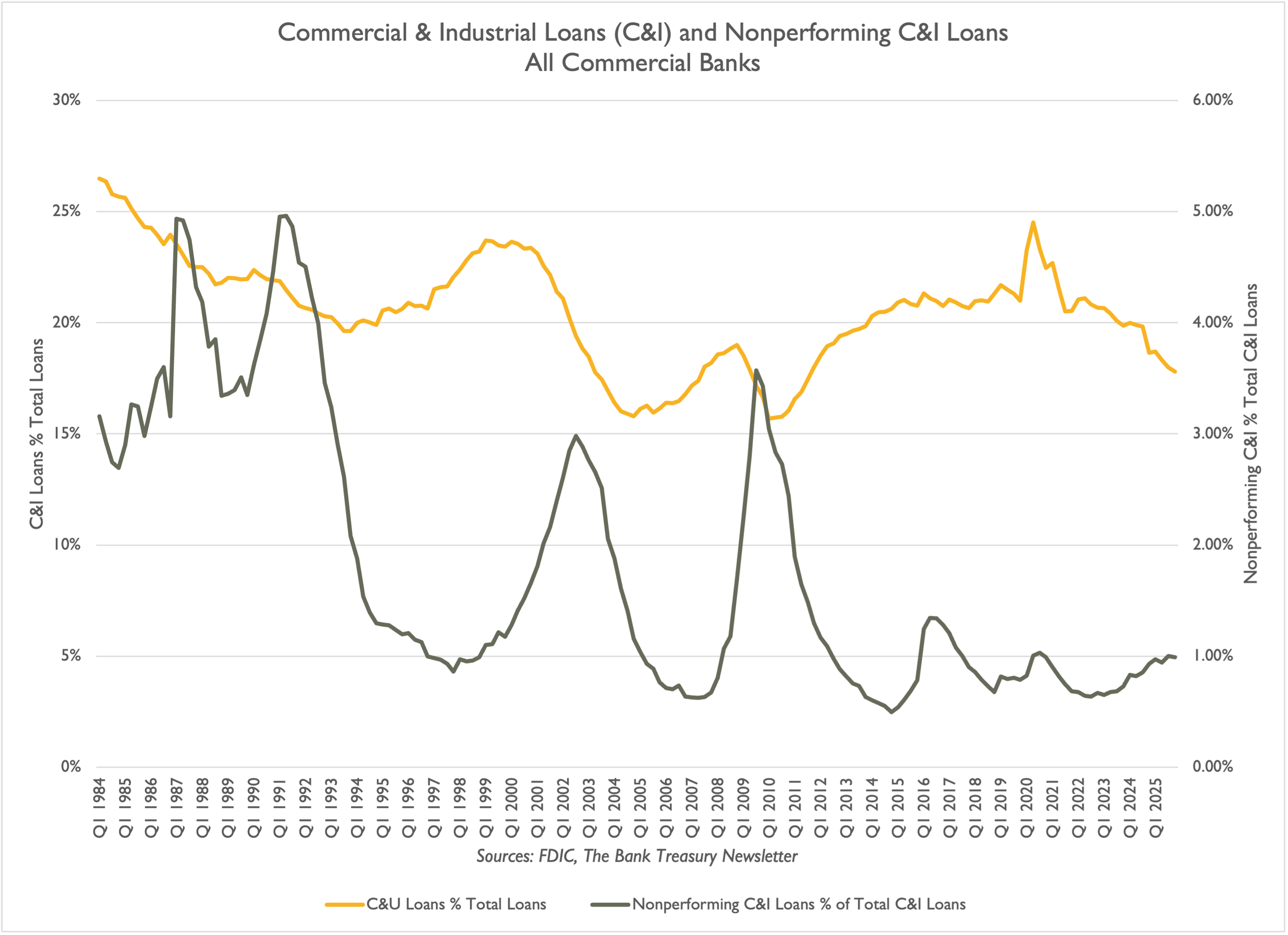

Bank executives are optimistic about making loans this year, but FDIC data shows that last year's most active lending was to non-deposit financial institutions. Commercial and industrial lending is flat and shrinking as a percentage of total loans. However, credit risk remains benign.

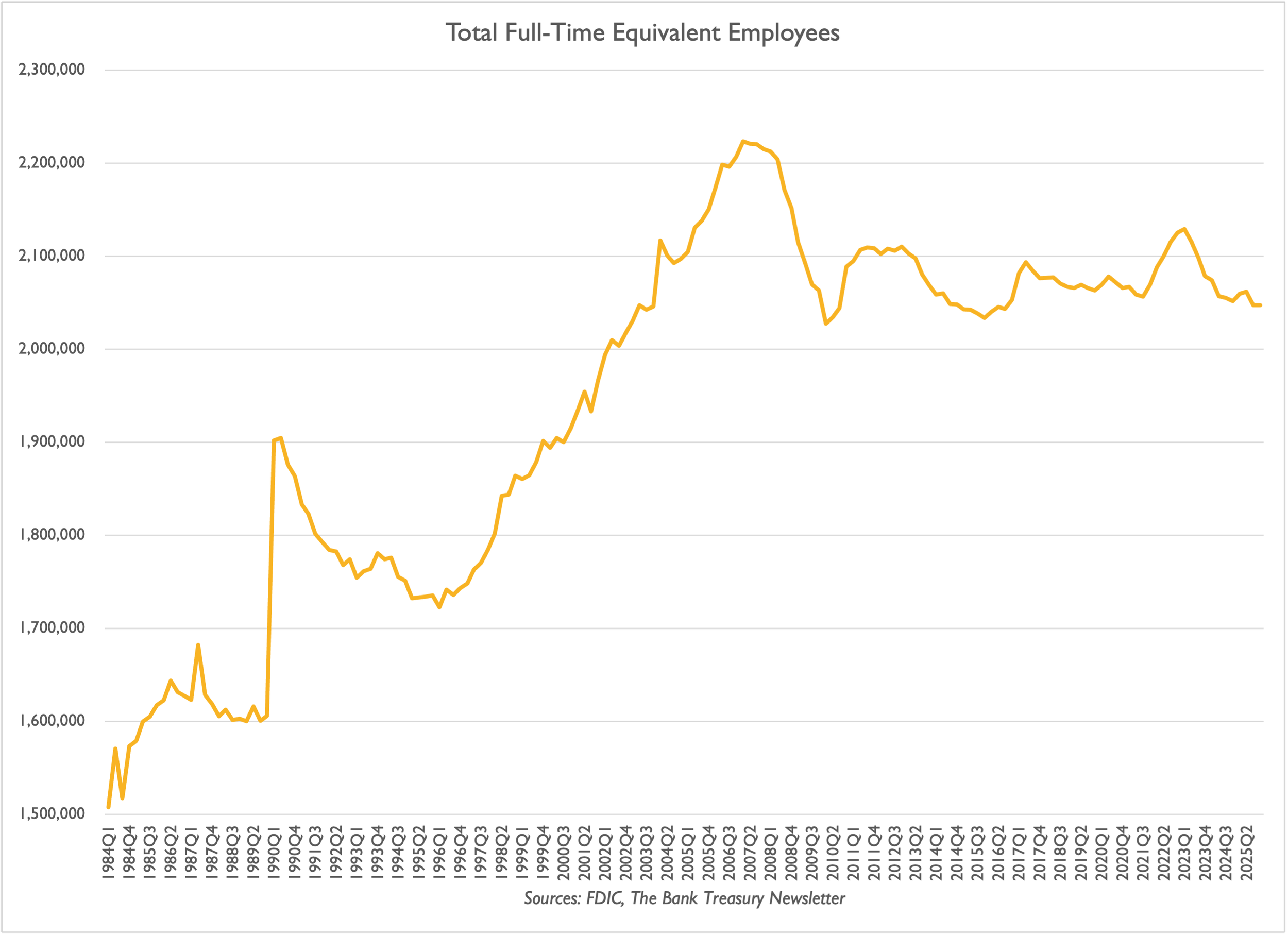

Bank executives claim AI reduces headcount and boosts productivity, but FDIC data (Slide 10) shows no decline. Headcount peaked before the Global Financial Crisis at over 2.2 million and has stayed flat at 2.1 million, despite the number of banks halving in 20 years (from 8,680 to 4,336).

M2 Is Growing Despite No Change In Reserves

IORB No Incentive To Hold A Lot Of Reserves

Ideas For Shifting Reserve Demand Curve=$1-2 Tr

Discount Window Loans Are Growing Again

SRP Usage Is Up

Payment System’s Lender of Last Resort Is Unused

Fed Finally Stopped Bleeding Net Interest Income

Currency Growth Back To Trend

Business Credit Conditions Are Excellent

No Sign Yet Of An AI Headcount Cut Dividend