BANK TREASURERS IN THE LAND OF MAKE-BELIEVE

Amid the backdrop of the Iran War and the associated economic uncertainty and market volatility, the Federal Open Market Committee (FOMC) voted 11 to 1 to maintain its target range for the Federal funds rate at 3.50% to 3.75% and to keep the interest rate it pays on reserves at 3.65%. The committee’s updated dot plot indicates only one 25-basis-point cut before the end of the year, with the next meeting scheduled for late April. Even Fed Governor Miran suggested he had doubts about the appropriate direction of monetary policy. While he has been a dove on rates since his appointment last September, he only voted for a 25-basis-point cut at this meeting, down from his previous votes for 50-basis-point cuts. The FOMC appears inclined to keep the Fed funds rate above 3% over the longer term.

The Fed’s balance sheet increased slightly this month to over $6.6 trillion as it ramped up its System Open Market Account (SOMA) holdings of Treasury Bills. This helped rebuild its reserve deposits to $3.0 trillion from $2.9 trillion at the start of the year, which it considers “abundant “and more than “ample,” as it technically defines the terms. Bank treasurers are responding to the faster pace at which the public is using instant payments by demanding higher reserve deposits. This, in turn, has strained markets like the Treasury repo market, which depends heavily on a plentiful, easily accessible supply of High-Quality Liquid Assets, mainly reserves.

Demand for reserves has driven up short-term interest rates, such as the Secured Overnight Financing Rate (SOFR). This month, the Effective Fed Funds Rate (EFFR) averaged 3.64%, while SOFR averaged 3.67%. This happens even though the EFFR represents an unsecured rate based on an interbank loan with a daily volume of just over $100 billion. Meanwhile, SOFR tracks the rate on Treasury repo, with a daily volume exceeding $3 trillion. The upcoming SEC clearing mandate, launching next year, might increase demand for cash and push SOFR higher.

Bank supervisors released their long-awaited proposal to update regulatory capital, aiming to provide capital relief for both large and regional/community banks. These capital proposals are part of a broad reform of bank supervision underway, extending beyond capital rules. Supervisors are lowering barriers to larger bank mergers, easing nonbank eligibility requirements for acquiring failed banks from the FDIC, and permitting more industrial loan companies and stablecoins. This month, the Kansas City Fed approved Kraken for a limited-purpose payment account. The proposals also include efforts to eliminate and simplify supervision and to address what supervisors believe are outdated or redundant requirements that unnecessarily burden the banking industry and do not contribute to a safe, sound, and efficient banking system.

The capital proposals include the Global Systemically Important Bank capital surcharge and, among other measures, suggest annual adjustments to systemic thresholds based on economic growth and inflation. A second proposal aims to ease capital requirements for trading and market risk, which, along with measures adopted last year for the enhanced Supplementary Leverage Ratio (eSLR), is expected to reduce overall common equity Tier 1 capital requirements by 5%. A third proposal seeks to lower capital requirements for regional and community banks on residential mortgage loans and mortgage-servicing assets to encourage the banking industry to increase investments in mortgage assets.

Earlier this year, President Trump directed the Federal Housing Finance Agency to order Fannie Mae and Freddie Mac to increase their total investment in Agency-guaranteed mortgage-backed securities by up to $200 billion. The two agencies had total assets of nearly $8 trillion at the end of 2025, but their securities portfolios amounted to just $155 billion. The Fed’s amortizing investment in these assets stood at just over $2.0 trillion this month, compared to $2.7 trillion four years ago, just before it began quantitative tightening in July 2022. Mortgage debt outstanding equals nearly $14 trillion.

President Trump also insisted this month that he would not back down from pursuing a criminal investigation of Chair Jay Powell over the renovations of the Fed’s headquarters in D.C., even after the courts rejected his complaints. As a result, Senator Tom Tillis, chair of the Senate Banking Committee and retiring at the end of the year, refuses to allow a vote on Kevin Warsh’s nomination to succeed as the next Fed chair. Chair Powell, whose term as Fed chair ends this May but whose term as Fed Governor continues until January 2028, insisted this month that he would remain as Fed governor after his term as chair ends, further complicating market expectations for the Fed and the course of monetary policy.

The banking industry’s message to investors remains unchanged: its commercial and consumer customers remain healthy, and it remains optimistic about earnings, profitability, and stable asset quality, despite worrying signs from Nondeposit Financial Institutions (NDFIs). Its only condition is that the war ends soon and energy prices stop rising.

The Bank Treasury Newsletter

Dear Bank Treasury Subscribers,

There is a real place called the Land of Make Believe, which, believe it or not, is located in Hope Township, New Jersey. Head west on Route 80 from the George Washington Bridge, and you'll get there in about an hour, depending on traffic. Many amusement parks across the United States have magical or fanciful names, such as Fantasyland, Dreamland, Storybook Land, and Fairy Tale Land. Still, there is only one Land of Make-Believe. Visiting it is worth it for that reason alone.

And the Land of Make-Believe has every single ride your kids could wish for in their hearts. From a junior-sized roller coaster to a Tilt-A-Whirl, a Drop and Twist, a Tornado, and a Scream Machine 360, yeah! It is like life in the bank treasury world.

He hasn't been there in years, but for some reason—who knows how the brain works—it came to mind while your editor-in-chief was daydreaming (he would say thinking) what to write about this month. Not that he makes things up in this newsletter. Rest assured, the news you read here isn't made-up, although some of it—like the fact that the shape of the yield curve remains notably unbank treasurer-friendly for net interest margins (NIMs)—our readers might wish were just their imagination playing tricks. Remember the part about those rate cuts this year? As a CFO from a regional bank in the Midwest quipped earlier this month at an industry conference,

“In terms of the…margin, look…the forward curve will be wrong. And so that has not played out the way that we would have hoped in terms of steepness in the belly of the curve. Things are still flat there. I think some help on that, some steepness in the curve, would be beneficial for…the banking industry.”

We can only hope. But this month’s theme is about the land of make-believe because bank treasurers may be living in one. You know, some astrophysicists believe—or they call it “theorize”—that the universe is a hologram, a projection from a black hole. That our entire perception of reality isn't real and is all in our minds. Is that what's happening now in the universe bank treasurers inhabit? Food for thought, because it is pretty crazy how much is on their plate these days, and we are not just talking about the war in Iran, although certainly that, too. After all, this cannot be happening. What bank treasurer would have ever thought that Iran would bomb them for buying a Treasury?

Let’s Imagine

What bank treasurer wouldn't want to close their eyes and go back to those halcyon days a year ago, when bank treasurers were still debating the Fed’s 50-basis point and 25-basis point rate cuts from the previous fall? All they were wondering about back then was whether Chair Powell’s actions were an attempt to influence the Presidential elections or a genuine effort to avoid cutting too late, without enough reliable data. Go back a year to when you thought it would be impossible if the FOMC were still keeping Fed funds around 3.50%-3.75% after this month’s meeting.

Who remembers the world before Liberation Day, which is approaching its first anniversary? (Can you believe it has only been a year?) Or a time when bank treasurers didn't worry about the Fed and the future of its independence, or even knew about the 1951 Treasury accord as a topic of polite conversation? So much has happened, so much is happening, and so much they wish or hope will happen—like a little peace and quiet, like returning to boring banking, or some predictability for a change, or wishing it would stop, like persistent inflation, monetary policy uncertainty, and market volatility.

The bank treasury landscape is a scenic tour through uncertainty, characterized by ongoing geopolitical and domestic conflicts, a playing field pitted with unknowns of the known and unknown variety: Russia waging regime change in Ukraine, the US and Israel waging regime change in Iran, and the US administration waging regime change in trade relations with the world. Bank treasurers must hope for a less uncertain future.

Maybe it takes more than hope for them to sleep at night, given the political stalemate and dysfunction people are reading about, with the ongoing partial government shutdown risking chaos for spring break air travel as Exhibit A. Add a Fed chair transition in May, Brent crude oil well over $100 a barrel, changing regulations, and a shifting competitive landscape into the mix. Look, it takes more than grit and determination to see the base case on the horizon. Figuring out how to get from A to B also requires imagination, if not a little magical thinking.

You need to imagine (as bank treasurers would say they assume) that there will be no miscalculations in the ongoing geopolitical games, which could last for who knows how long. Pray that chaos does not lead to catastrophe. Hope that, despite all the talk today about artificial intelligence (A.I.) killing the job market, higher gas prices, persistent high rates at the long end of the yield curve affecting housing and affordability, and volatility in the equity markets, the economy will hold up and consumers will continue spending.

Just maybe, Vice-Chair Miki Bowman’s plan to ease capital requirements for mortgages and the President’s new executive order will help make being a first-time homebuyer great again. You can imagine everything working out while the Fed rescinds enforcement actions left and right. You just must. And, stop watching the news, because as the CEO of a regional bank based in the Midwest told analysts,

“If you weren't watching the news, you'd feel fantastic. Loan growth is good. Pipelines are solid…Clients are reasonably optimistic. Deposit pricing is rational in the Midwest, and credit remains very good.”

Do not imagine that the wave of bank consolidation is out of control, as bank supervisors appear to wave in applications as if they were collectors at a toll gate. No need to worry that if the trend continues, all banks will end up merged into a single, big, beautiful bank, the failure of which would be unimaginable. In reality, that ship sailed long ago.

There is nothing to imagine. It is a reality. The banking industry’s assets are already concentrated in a few institutions, with the four largest U.S. banks controlling 40% of the industry’s $25 trillion in total assets, and the biggest of those four holding 15%. If anything were to go wrong with just one of them, let alone the largest, it would be hard to imagine the remaining 4,300 commercial bank call report filers continuing business as usual. When they failed three years ago, the combined total assets of Silicon Valley Bank, Signature Bank, and First Republic Bank were a fraction of the size of any one of the top four banks, and look at the havoc they caused that required the Fed’s swift intervention, along with the FDIC’s, to save the day.

Living Will and Discount Window Fantasies

Politicians can rail on all they want against too-big-to-fail and demand well-crafted living wills that clearly outline the bank’s plan for an orderly wind-down in case of bankruptcy due to material financial distress or failure. They can argue over whether a single point of entry or multiple points are better for resolution. But theory does not always translate into practice in the fog of war that demands expediency and heroic interventions, even if Miki Bowman is merely questioning the usefulness of living wills at this point.

Take the Fed's discount window as another example of wishful thinking, since the Vice Chair for Supervision brought it up this month. You see, theoretically, a bank treasurer should count on the Fed’s discount window in a pinch, and use daylight overdrafts for payments, as technically the Fed is a bank treasurer’s lender of last resort — the guy you call when no one else is willing to answer your call. In the Vice-Chair’s view, borrowing from the discount window is operationally challenging for banks, as each reserve bank administers its own discount window, as she understands it.

“Currently, each of the 12 Reserve Banks has their own rules and processes and an independent ability to make lending decisions—decisions that may vary across Reserve Banks for similarly situated borrowers and similar collateral. This fragmentation creates uncertainty for borrowers, but it can also serve to exacerbate fragilities in the banking system. After years of recognized flaws, we have yet to address these known weaknesses…Some see tension between monetary policy implementation tools and regulatory objectives. In my mind, these goals should be compatible if we are modernizing the discount window to serve as an effective liquidity backstop, instead of a theoretical option.”

But in reality, stigma remains stigma, and borrowing from the Fed’s discount window carries a lot of stigma—so much so that bank treasurers only include it in their contingency funding plans in theory. In principle, if the Fed didn’t have to publish borrowers' names at the window after a two-year delay, that might help reduce the stigma, but in practice, the law is the law. Even if the Dodd-Frank Act was not forcing the Fed’s hand, a resourceful researcher can figure out who is borrowing by tracking changes in the Fed’s balance sheet in the weekly H.4 report.

Fighting the stigma is a losing battle, as New York Fed researchers concluded in a report they republished this month,

“Our results suggest that the persistent stigma…still associated with discount window operations may present a challenge to achieving this objective. Over the past 25 years, the Fed has introduced multiple reforms which have failed to eliminate stigma. Which additional measures could be implemented, and whether they would be successful seem unclear.”

The truth is, if bank treasurers need money in a pinch, they will visit other windows, starting with their FHLB before calling the Fed’s hotline. Yes, technically, the Fed is a lender of last resort; its architects designed it for that purpose. But according to the Federal Reserve Act, Regulation A, the Fed cannot lend to a bank it considers not “generally sound,” at least not on primary credit. Secondary credit may be extended to a troubled bank, but not longer than overnight.

For all the focus on Silicon Valley Bank not testing its lines, it was a goner anyway on March 10th, when it failed. The liquidity it seemed to have with a balance sheet concentrated in U.S. Treasurys and Agency MBS was an illusion, a fantasy, and make-believe. The Fed could not have lent it a dime, even if it were set up properly with pre-positioned collateral. But that reality did not deter Treasury Secretary Scott Bessent, who called for a fresh look at liquidity analysis when he spoke earlier this month,

“SVB, Signature, and First Republic each had substantial holdings of Treasuries and agency MBS. But that liquidity existed only on paper. Collateral was not fully prepositioned. Discount window access was untested. That was in part because the policymakers who had designed the framework were so keenly focused on reducing dependence on the lender of last resort…to mitigate moral hazard. Then reality intervened in March 2023. Now, the conversation is about reducing stigma around the discount window, incentivizing collateral prepositioning, and normalizing routine testing of central bank facilities. The upshot is that we should not treat post-crisis liquidity regulation as somehow sacrosanct. These rules are working drafts, not tablets handed down from the mountain. With the benefit of some distance from the crisis, it is time for a fresh look.”

Bank treasurers don't think they'll ever use the discount window to get a loan. Still, they can easily see that the rise of instant payments and stablecoins threatens their roles by creating disintermediation. They might wonder why their regulators are fine with the public moving money from traditional bank accounts to crypto-fintechs like Kraken, which recently opened an account with the Kansas City Fed. And if they don't want to bank solely with Kraken, now they can transfer money to one of the state-chartered industrial loan companies (ILCs) that the FDIC recently approved, thanks to a loophole in the FDIC Act that was expanded this year, allowing ILCs to provide insured deposit services across state lines.

You have to imagine the possibilities. The possibility that Kevin Warsh might not be confirmed by May, when Chair Powell’s term as chair ends, and that the vice-chair of the Board, Philip Jefferson, could become interim chair. Imagine what would happen if, given the dysfunction in the legislative branch and the outcome of this fall's midterm elections, he were never confirmed. You have to hope that at least everything turns out all right despite the ongoing, never-ending, and eternal chaos, volatility, and exhausting uncertainty that colors the bank treasury landscape.

You have to believe, or at least suspend disbelief, not to worry that, with bank supervisors rolling back capital and liquidity rules, handcuffing their examiners from citing banks for qualitative issues over material ones, killing morale while struggling to recruit new examiners, that they will not end up short-handed the next time there is a crisis that they did not see coming. And yes, our bank treasury subscribers are super stoked about the new approach by their supervisors, as the chairman and CEO of a regional bank based in the northeast said,

“I just couldn't agree more with the approach of trying to focus on the risks that matter…And trying not to divert resources to places that in the scheme of things don't matter, documentation -- you didn't document your model exactly right. So that's been a really positive shift. I think -- I'm not sure it results in us saving money. It results in us actually focusing on places that matter most.”

They are just pleased beyond words, as the CFO of a large regional bank in the Midwest said,

“We're just pleased with the direction regulators are taking. They are more focused on large financial risks. And I think that's to be applauded.”

But change breeds its own risks, like an examiner not flagging something because their boss no longer backs them in a confrontation with management, which can lead to material problems that might have been averted if documentation had been properly filed. You never know. Throw in rate uncertainty into the mix, tariffs which Chair Powell blamed this month for inflation’s persistence above 2%, maybe a dose of higher unemployment, maybe include in the scenario a shocking bankruptcy, a war-related reversal of fortune, or a political surprise, and bank supervisors may have a genuine crisis on their hands. Bank treasurers can only hope, pray, imagine, or believe that the Fed’s monetary policy tools will still be enough to save the day the next time trouble comes knocking on the door of the $500 trillion global financial system.

Hope for the best, right? But as everyone knows, the banking industry isn't into shocks, so bank treasurers need to pay attention. Don’t be surprised, because shocks are usually shocking because no one saw them coming, and black swans are real creatures that live down under. The truth is that surprise results from a failure of imagination, not that what happened was impossible to predict.

You know the scenario planning you all do—base case, adverse, severely adverse? Well, what if one of your scenario planners who works for you came to you a year ago with a scenario that included all the events we see now? Would you have dismissed their scenario as unrealistic, like one of the Fed’s severely adverse scenarios in its stress tests, where the whole world falls off the cliff in the next quarter? But in a world where an endless list of unlikely and unrealistic events keeps happening, maybe what is shocking is just what you failed to imagine and for which you failed to prepare.

Debt Shock and NDFIs

Debt and economic shocks rarely mix well, which is why bank treasurers can't ignore the rising U.S. deficit, which, according to the Congressional Budget Office, will soon engulf the economy. Debt ceiling drama, along with shutdowns and showdowns, doesn't inspire confidence that the current path is sustainable. Federal budget analysts warn that we could face another debt-ceiling crisis by this November. And then what? One thing is for sure. The U.S. cannot fail. It would be shocking if not unimaginable.

And they are getting shocked about more than just the U.S. debt monster. They cannot stop talking about the private credit story, too, otherwise known as NDFIs. The business may finally be getting its comeuppance for muscling in on what has been a traditional bank’s lending territory.

In all fairness to NDFIs, most loans that commercial bankers lost over the years to them probably wouldn't have been made directly anyway, either because they fell outside their credit box or they did not generate enough return for regulated commercial banks, which are subject to strict capital and liquidity requirements and must, at a minimum, cover their cost of equity. NDFIs don't have to worry about Basel when making loans.

But from a bank treasurer’s perspective, lending to NDFIs was an even better deal than lending directly to the ultimate equipment finance and real estate borrower. NDFI loans were a dream come true for both the bank and the NDFI. A win for the bank, which could use the loan business, and a win for the NDFI, which needs a bank loan to achieve the leverage required to generate index-beating returns on the private assets it manages.

And if the NDFI runs into any trouble, no worries was the thinking in bank treasury departments across the country. Aside from the fact that the loans are secured, we are talking about institutions that are super-large, as big or even bigger than the largest banks. If the largest banks are considered TBTF because systemic shockwaves could threaten financial stability, what would happen if one of the big NDFIs ran into trouble? The largest has assets under management that top the combined total assets of the top four banks.

If the collapses of AIG and Lehman during the Global Financial Crisis caused some damage, is it even imaginable that an NDFI today, many times larger, could go bankrupt without any intervention by the Fed? For that matter, talk about the dangers of overconcentration and risk to the economy. Because ten technology companies now account for one-third of the S&P 500's value,and they're selling off this month even though their earnings came in great.

But that supposition may be put to the test. During the good times, NDFIs were thriving, expanding their portfolios, while commercial banks were left to stew and blame regulators for overly strict bank capital and liquidity regulations, regulations they said were unfairly preventing competition, creating an unlevel playing field, and so on. But as experienced bank lenders know, you can't defy gravity and credit cycles forever. It’s during the downturn of a credit cycle, after a rate-hiking phase, when borrowers may be facing structural changes in the economy, that past underwriting assumptions become exposed as overly optimistic in hindsight, and mistakes from better times come back to haunt lenders who dismissed downside risks as unrealistic. As Warren Buffett is fond of saying, “When the tide goes out, you find out who has been swimming naked.” Fraud and bad underwriting get lenders every time.

Who would have expected AI to threaten the businesses that NDFIs lent to a few years ago? Ignoring warning signs, private credit firms increased their leverage to the companies most at risk, worsening their exposure, at the worst time. Because it is never a good time when nervous investors start pulling their money back, and it is never a good look when NDFIs try to staunch the bleeding. A perfect storm—who could have seen that one coming? The lesson is, pay attention. As the president and chief operating officer of a regional bank in the West told analysts.

“The…industry has been gulping down NDFI loans. If you haven't paid attention to that, you really should.”

But hold on, as the CEO and chair of a global bank reminded analysts, the banking industry is not overly invested in the NDFI trade, and for all the worry, what we have today is a series of one-offs.

“We need to get some facts on the table. Private credit's a $1.7 trillion market. We just wiped $1 trillion off crypto, and no one missed a beat…Retail investors are not a major investor in the space yet…I'm more sanguine on private credit. There will be some idiosyncratic risk from folks with weak credit standards, but it's not a systemic issue.”

But hold on. What appears on bank balance sheets is only part of the story. As Fed researchers noted in a report they published last summer, the banking industry has been increasing lines of credit to NDFIs, even if its funded loan balances remain the same. Now imagine this scenario: NDFIs are suddenly forced to draw on these lines during liquidity stress, like right now, when investors are withdrawing their money. Things could get a little risky, right? As the CEO and chair continued, it’s not just one shock that gets you. It’s multiple shocks happening one on top of another.

“Where it gets a little more concerning would be if the Middle East crisis goes on for a long time and you see a convergence of the concerns on AI evaluations, on the disruption risk, into business models from AI, we're seeing it obviously with software as a service (SaaS) software, some of the business services, and private credit all coming together.”

Funded or unfunded, direct or indirect, as the chair and CEO of a large regional bank based in the Northeast told analysts, it all connects. The private credit market is a major innovation for the economy. However, a shock among the NDFIs, especially the largest one, will ripple through the commercial banks, both large and small.

“I have no problem with private credit. When we grew up in the '90s in banking, we couldn't securitize middle-market loans or commercial real estate. The liquidity factor of this is an extraordinary gift and a great innovation in the space…I think the big risk we have today, no matter how you look at it, is that too many of us are looking at the US as if there were more than one financial system. There's just one” everything” that is interconnected. You can't have a bad day in private equity about having some impact on the banking system.”

AI: The Hype and The Reality

Bank treasurers have high hopes for AI. They imagine it speeding up processes, increasing efficiency, aiding decision-making, and maybe even letting them leave for home early. However, they worry it could cost them their jobs someday; they worry that their competitors are using it and that they must keep up; and they suspect that much of its output is just hallucination, but they will not have any way to tell the difference between make-believe and reality.

AI is a mix of knowns and unknowns, opportunities and threats. Fed economists understand it will impact the economy, but exactly how remains unclear. Will it disrupt the workforce and reduce jobs? Or lead to a deflationary trend in prices?

Kevin Warsh and Scott Bessent believe that the technology’s benefits will outweigh its costs, like free trade, a win-win, notwithstanding the old free-trade North American Free Trade Agreement, which politicians like to blame for the loss of factory jobs to Mexico. In their view. AI will boost productivity and reduce costs, thereby justifying easier Fed policy, which will support economic conditions that will lead to more jobs.

White-collar coders will go back to school to learn a trade, such as becoming an electrician, to support the new data centers built to run the technology that took their jobs and to service the HVAC systems that keep the technology from overheating. Who could make up a story like this? But not every economist or would-be Fed chair agrees, as Bill Dudley, former president of the New York Fed, recently opined.

Will AI disrupt the labor market, boost productivity, or perhaps even eliminate mankind someday? Bank treasurers don’t know. The president and CEO of a regional bank in the Midwest knew only one thing: if his bank was going to discover what the technology could do for it, he would need to lead the way, telling analysts at an investor conference this month that AI is,

“… an opportunity and a threat…Early in my career, somebody told me, " What gets attention gets done.” And I think this is one of those times that, from the CEO down, you need to give quite a bit of attention to AI.”

The chairman and CEO of another regional bank based in the Midwest was still trying to figure it out.

“I think we're all trying to figure that out. The Board recently asked me, "Well, how do you see AI affecting the bank in two to three years?” And that's a hard question to have an honest assessment of. I think there are a lot of positive things that come from that. There are probably some things that we're not going to like that are going to come out of that. It's too hard to tell. I mean, like every other institution, we're deploying AI as fast as possible. And I think that -- I think we're trying to figure out how to exactly monetize that. How do we take those savings? If I can create 10% or 20% more savings in your day, are you just a more productive, happier employee? Or is there a way for us to monetize that? I think we're still trying to figure out, can we truly drive revenue off AI investments?”

If nothing else, a bank executive at a large regional bank headquartered on the East Coast believed AI would lead to more loan business.

“We do some data center lending. It's a relatively small part of our book…But we also do equipment finance. We do some renewable energy project finance…as an adjacency to the data centers…HVAC and many other areas intersect with that industry, and we have seen some pickup in business.”

Free Money Out of Thin Air

To make those loans, the bank’s treasurer will need to fund them, and here is one of the most magical things about banking. Bank treasurers create deposits by making loans. The story the general public hears is that banks intermediate between borrowers and savers, gathering deposits and converting them into loans. But that is just a fairy tale. Bank treasurers know that reality is otherwise. As Hugo Rodrıguez Mendiz´abal, a researcher with the International Journal of Central Banking, explained in a September 2020 post,

“In real life, and unlike in traditional banking models, if the loan is approved, my bank does not search for existing deposits to channel them to me. Instead, what my bank does is just create these deposits on the spot, out of thin air, at the stroke of a computer key. This deposit-creation power is the distinguishing characteristic of depository institutions.”

Banking truly feels magical, doesn't it? And when do bank loan departments want to make loans? Usually, when they and their borrowers are optimistic about the future, right? Nobody wants to borrow money today, thinking ruin is just around the corner. And judging by comments from the C-suite of the nation’s banks, there’s a lot of optimism out there.

With the Iran war raging, the chairman and CEO of a global bank could not feel more confident, telling analysts,

“Look…the underlying economy is doing just fine, around the world, and activity is good, business momentum is good, consumer spending was up about 5% in February, here in the States. We're seeing a fiscally responsible consumer as well…On the corporate side, I think particularly here in the States, corporates very much on the front foot…I think, particularly given everything going on in the Middle East, balance sheets are probably the strongest I've seen in my tenure, and they haven't been weak during that tenure…Got some other positive drivers that are coming through. Deregulation is making a difference. We're seeing things getting done faster, more confidence out there, and then we're also going to have the tax bill benefits coming through.”

Things are good, and their customers are tested by challenges like COVID, rate hikes, and tariffs. Also, the typical consumer the banking industry lends to is at the higher end of the economic ladder and is doing well. According to the president and CEO of a regional bank based in the Southeast,

“Despite some recent volatility, customers remain optimistic. Businesses continue to demonstrate really good management of their balance sheets and income statements, good liquidity, and capital…We're seeing continued job growth in our markets…Consumers are generally in pretty good shape. We're seeing more pressure, probably on the lower-income customer…but we don't extend much credit to that customer, so we're not seeing much change in our consumer credit metrics…We also do business in the Midwest, which is, that economy's pretty solid too.”

But the CFO of a regional bank in the Midwest was a bit more cautious, saying only that if he could go back a few weeks, he would feel very optimistic about the future. Remarkably, people and businesses are still holding onto some of the COVID stimulus money they received six years ago.

“If we were talking three weeks ago, I would tell you that we were feeling really good about what we were seeing from a credit perspective…. We think that there are tailwinds helping consumers. With… larger tax refunds…this year, like there is real money hitting people's pockets…Today, we're obviously cautious about what $100 oil could mean…But from a broad, big-picture perspective, the portfolio remains healthy. We're not seeing any broad-based industry weaknesses…And you've seen continued strength post-COVID, with government stimulus retained on both corporate and consumer balance sheets.”

The bank’s loan department provides funds to customers by depositing money into their accounts. There's no need for a bank treasurer to rush to secure funding for the loans; the process is simply two sides of the same coin. In fact, if the payer and payee both banked at the same bank, the bank treasurer would never need to consider funding for the loan. However, once a customer withdraws those deposits from Bank A to pay someone with an account at Bank B, the treasurer at Bank A, who still holds the unpaid loan balance, will need overnight funding to cover the balance. Conversely, the treasurer at Bank B will have a deposit balance in need of an overnight home.

R&T Deposits and StoneCastle Partners, now part of Fiserv, which both sponsor the newsletter, connect the deposits at Bank B back to Bank A. Overall, loans match deposits, and the more loans the banking industry makes, the more deposits it creates. However, at the micro level, Bank A and Bank B face a frictional reality in which it matters which bank holds the money and which holds the loan.

Risk-Free: Real or Imagined

After reviewing their funding situation, bank treasurers will need an appropriate risk-free rate as a benchmark for loan pricing. Economists in their ivory towers believe (they say “theorize”) in the existence of risk-free interest rates, at least in a theoretical sense—a pure short-term interest rate that exists when the economy is at full capacity with stable inflation—economic nirvana. They call this short-term, real, neutral risk-free interest rate R-Star, a rate that is neither too hot nor too cold, neither too tight nor too loose, and neither too stimulative nor too repressive.

A rate that is almost perfect except for the fact that you can't see it. You have to rely on economists to tell you it's there, at least in their minds. Presumably, if R-Star didn't exist, the entire fixed-income system would fall apart. And in fixed-income land, where bank treasurers operate, you have to believe in something.

R-Star doesn’t exist, but SOFR does. Now, SOFR isn’t perfect either. Nothing truly is. But it’s the next best option for pricing a loan and is much better than the London Interbank Offered Rate (LIBOR), which no longer exists. When LIBOR was active, it included both a risk-free rate and an adjustment for interbank credit risk, so it was not a pure risk-free rate. But the volume backing it is SOFR’s greatest appeal.

SOFR is the average rate for tri-party overnight Treasury repo cleared through the Fixed Income Clearing Corporation (FICC). Its daily volume now exceeds $3 trillion, compared to the interbank Fed funds market, which totaled $106 billion last year. Calling the Fed funds market 'interbank' might be a stretch, considering the FHLB’s significant role in it. As of December 2025, commercial banks bought and sold $15 billion of Fed funds. Meanwhile, the FHLBs most recently reported selling $91 billion of Fed funds in the market, mostly to foreign branches and agencies.

SOFR is a tangible, observable risk-free rate, unlike R-Star, which remains theoretical and cannot be directly measured. The main limitation is that SOFR is influenced by real-world frictions, which are clearly visible when a bank treasurer compares the effective Fed funds rate to SOFR. Bank treasurers usually expect that lending their excess cash in the Fed funds market to another bank—without collateral or insurance—should yield a higher return than investing the same funds in Treasury repo, which is considered risk-free despite the credit rating downgrades the U.S. has experienced over the past 15 years.

If the FDIC decides to close a failing bank that has borrowed in the Fed funds market, bank creditors would need to join other uninsured creditors in line. However, SOFR averaged 3.67% over the past 30 days, while Fed funds averaged 3.64%. Near month-end, SOFR has even risen above the top of the Fed’s target range for the Fed funds rate, exceeding 3.75%. As Figure 1 suggests, liquidity conditions in the Treasury repo market might be better than they were last fall, before the Fed began slowly rebuilding its position in Treasurys, buying Bills after it ended Quantitative Tightening.

Regulatory Relief and the Basis Trade

However, such anomalies are how traders generate profits. Essentially, the Treasury basis trade relies on the idea that no two risk-free rates are the same, even when they have the same maturity and are issued by the same entity. Off-the-run Treasurys, which make up 98% of the$31 trillion in total Treasurys, are traded at a lower price than on-the-run, new-issue Treasurys. This price difference rewards buyers for accepting a security with slightly less market liquidity than the closest on-the-run maturity.

The basis trade involves buying an off-the-run, cheaper-to-deliver Treasury while simultaneously selling a futures contract that trades against an on-the-run security, and financing the off-the-run Treasurys in the repo market. (R.J.O. Brien, which Stonex acquired last year and is one of this newsletter’s corporate sponsors, can help you set up and trade futures.) Finally, use the relatively cheap off-the-run Treasury you purchased as collateral in the repo market to finance your cash position until you're ready to deliver it against the futures contract you shorted. This strategy is known as trading the basis.

Recent stress in the repo market, which more cash providers could help ease, has increased upward pressure on SOFR and made trading the basis more difficult. To reduce that stress, bank regulators introduced new rules that exclude trading positions in Treasurys from the calculation of the enhanced Basel 3 Supplementary Leverage Ratio, which large banks say limits their ability to supply more cash in the repo market. It remains to be seen whether these changes will be effective, as the rules only take effect next month. Additionally, they introduced measures specifically designed to lessen the capital burden on the largest banks. By the end of Q4 2025, the banking industry net provided $267 billion in cash to the repo market, which is dominated by money market funds that invest nearly $3 trillion.

Demand for Reserves: It Is All About the Payments

Bank supervisors might not be able to fix all the issues preventing the largest banks from providing more cash to the repo market, rather than leaving their reserve balances at the Fed, even after adjusting capital and liquidity requirements. The reality is that a bank would prefer to keep its excess liquidity at the Fed overnight, which currently pays 3.65%, rather than in the Treasury repo market, which pays more and is, under SOFR arrangements, as riskless an overnight investment as the Fed’s balance sheet. One reason for this is payments—you need reserves to make payments.

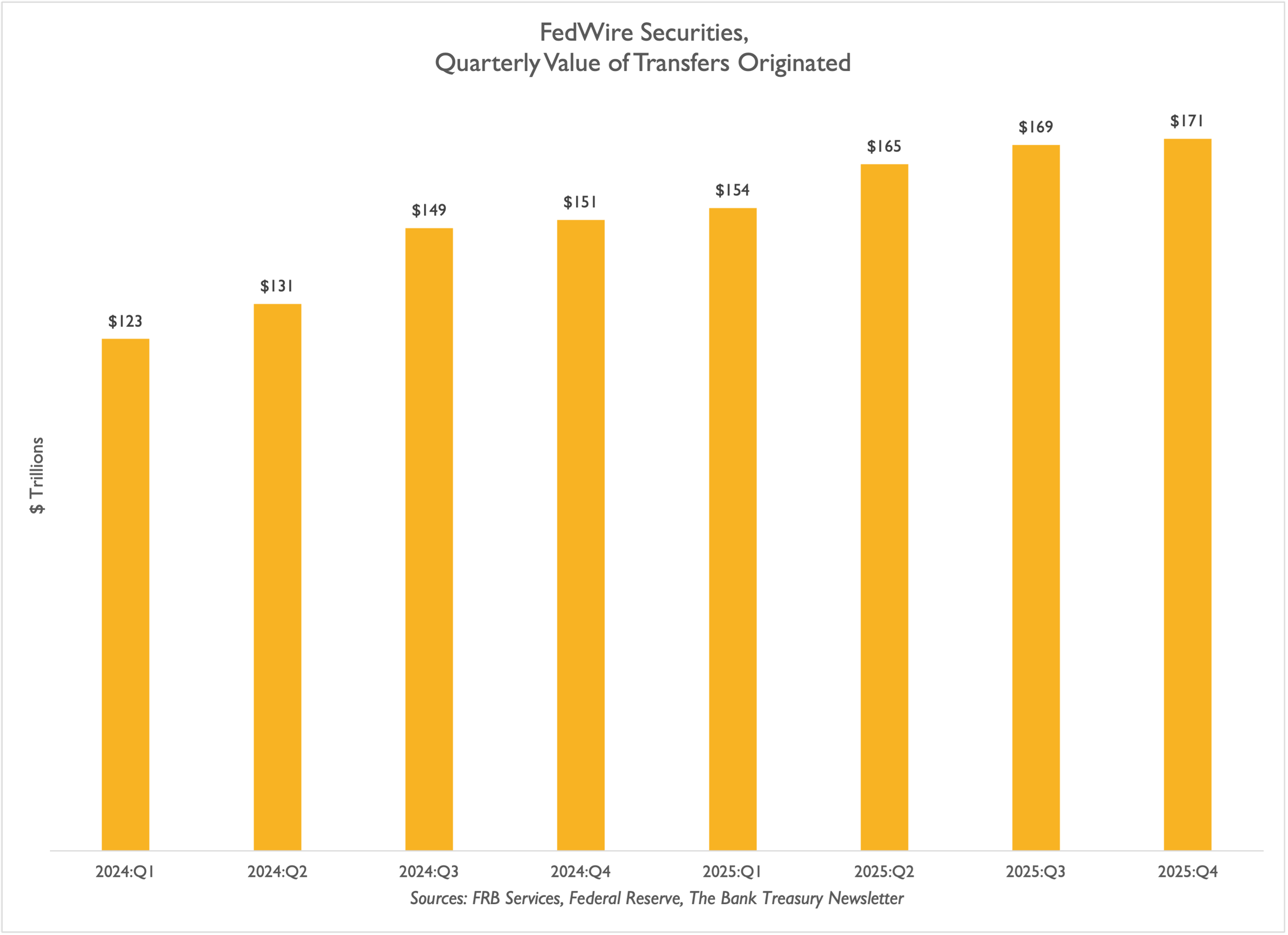

Based on FedWire data, the average daily transfer value was $4.6 trillion last year. Over the year, this amounted to $1.1 quadrillion in payments through FedWire. Meanwhile, reserve balances on the Fed’s balance sheet, which bank treasurers rely on to process these payments, totaled $3.0 trillion, down $0.2 trillion from the previous year. If Kevin Warsh and Scott Bessent are serious about slightly shrinking the Fed’s balance sheet, they will need to address the increasing demand from banks for reserves to manage their payment flows, even without the need to hold a ready source of liquid assets to weather stress scenarios.

It's not just payments over Fedwire that increase bank demand for reserves, but the shift to instant payments, too. In an instant payment environment, where FedNow, tokenized deposits, stablecoins, and other digital payment rails become the dominant means of payment, bank treasurers will likely hold more liquid assets. As researchers at the Central Bank of Brazil discovered, a decade after it allowed them, instant payments turn commercial banks, which can create money from thin air, into narrow banks too afraid to do anything with their cash inflows but leave them overnight at the Fed.

“Economically… depositors benefit from immediate payments, but this convenience inadvertently implies a loss in banks’ autonomy in managing the timing of their payment flows. As our model shows, the reduced capacity to delay and net payments leaves banks more exposed to the volatility of payment shocks, which induces them to hold a larger proportion of liquid asset buffers and a smaller fraction of illiquid assets.”

The researchers went a step further, concluding that banks in instant payment worlds also take more credit risk on the assets they keep outside their liquidity buffers.

“The inability to delay payments increases banks’ demand for holding liquid assets over transforming illiquid ones, lowers their profitability per unit equity, and exacerbates their risk-taking incentives. Our findings bear important financial stability implications in light of the global surge in adopting instant payment systems, e.g., FedNow in the US.”

Ultimately, instant payments will weaken the stability of low-cost, core deposits, which means bankers must intensify efforts to expand relationship banking, as explained by the CEO of a regional bank in the Southeast.

“I think over time, you're going to see a shift in how digital tokenized deposits…things like that… affect the industry…You're going to see an upward drift in deposit cost that drives towards more wholesale-type funding levels. Given that, it's incumbent upon us and everybody else to do the other things that I've talked about to drive profitability by building relationships and making sure that you have broad, deep relationships, and that you're not in any way, shape, or form a one-trick pony…and stay away from trying to create short-term transactional money.”

Tokenized deposits are fueling the instant payment trend, and their adoption is increasing, according to the chief product officer of a global bank, who told analysts this month.

“We've been in the digital asset space for almost a decade. And…let's say, 8, 9, 10 years ago, it was a curiosity. Clients were asking, "What is this?" Then it moved into, "Well, how is that going to impact my business?" What are the opportunities for us? And now it's really about how it will reshape the financial markets…I'd say that the market and our clients are looking for constant ways to focus on real-time everything, real-time cash, real-time positioning, daily NAVs, more liquidity, transparency, and mobility, and blockchain or distributed ledger technology is right in the heart of all of that.”

Regional bank treasurers are all over digital payments, as the president and chief operating officer from a regional bank based in the west told analysts,

“There's all this talk about stablecoins and programmable tokens…We'll be experimenting with stablecoins and tokenized deposits later this year…You have to be real-time to live in a tokenized deposit, stablecoin world, and we already are real-time.”

Clearing and the Illusion of Safety

The SEC's clearing mandate, which aims to reduce settlement risk in the Treasury cash and repo markets, could either benefit or harm the Treasury basis trade when it takes effect next year. It requires all parties involved in a Treasury security or repo transaction to settle through a central counterparty (CCP), which sets standardized margin and collateral haircut requirements. Until this year, the FICC was the only CCP clearing Treasurys and repos, but now new market entrants like CME have also entered. While the mandate's goal is to reduce risk and uncertainty, it may inadvertently increase market volatility and trading risks.

As a recent Chicago Fed study explained, cross-margin relief is crucial for the basis trade and, by extension, for the stability of the Treasury market. Combining a long position in cash with a short position in futures reduces the trader’s market risk exposure, which the initial margin is meant to cover. The authors estimated that allowing traders to receive credit for the hedge when setting initial margin could cut trading costs by up to 75%. Without this relief, they feared that the new clearing mandate aimed at lowering risks would end up forcing participants out of the market.

Reduced activity in the Treasury market and higher price volatility will complicate collateral valuation in repo transactions. This may discourage cash providers, banks, and money market funds from participating, as they might prefer to hold more cash at the Fed. Such a shift would not support Kevin Warsh and Scott Bessent's view of a smaller Fed balance sheet and fewer reserves in the system. Additionally, it would prolong SOFR remaining above the Fed funds rate.

But reducing initial margin requirements for basis trades also carries risks. As Sarah Breeden, Deputy Governor of the Bank of England, warned last year, it could complicate a CCP’s position if a member goes bankrupt in the middle of a trade involving more than one CCP.

“The CCP that clears the repo is often different from the CCP that clears the future, so if the trader is clearing both legs of the basis trade, they could be paying two sets of initial margin. But in the case of cross-CCP margining, the margin is based on the net risk position across multiple CCPs, assuming that the CCPs will cooperate to manage the position as a single portfolio in the event of default. Should that link between CCPs break down for any reason, including operational ones, an unexpected extra margin could be significant. Such arrangements put a premium on ensuring CCP resilience, including in stress.”

Jenny Jump, Ghost Lake, and the Haunted House

One more reason to visit Land of Make-Believe is its haunted house attraction, located next to Jenny Jump State Park, which features a glacial lake called “Ghost Lake” surrounded by stone cliffs. At the bottom of these cliffs, there’s an old lake house. Locals say the entire area is haunted.

You see, a long time ago, Jenny’s family lived in the lake house. One day, when she was nine, she went to pick some berries at the top of one of the cliffs and was surprised by a Native tribe that she feared would kidnap and kill her. Her father, who saw the danger she was in, called out to her, “Jump, Jenny, jump,” assuming she would land safely in the lake and avoid capture. Unfortunately, she was not much of a jumper and ended up hitting the rocks and then drowning in the lake. On moonlit nights, the locals say you can still hear her father’s faint, whispering cry, “Jump, Jenny, jump.”

The lesson, as bank treasurers know firsthand, is to always be prepared and rehearsed for all emergencies. Exit strategies and contingency funding plans only work if you can execute them during a crisis. Otherwise, as the saying goes, best-laid plans...

The Bank Treasury Newsletter is an independent publication that welcomes comments, suggestions, and constructive criticisms from our readers in lieu of payment. Please refer this letter to members of your staff or your peers who would benefit from receiving it, and if you haven’t yet, subscribe here.

Copyright 2026, The Bank Treasury Newsletter, All Rights Reserved.

Ethan M. Heisler, CFA

Editor-in-Chief

This Month’s Chart Deck

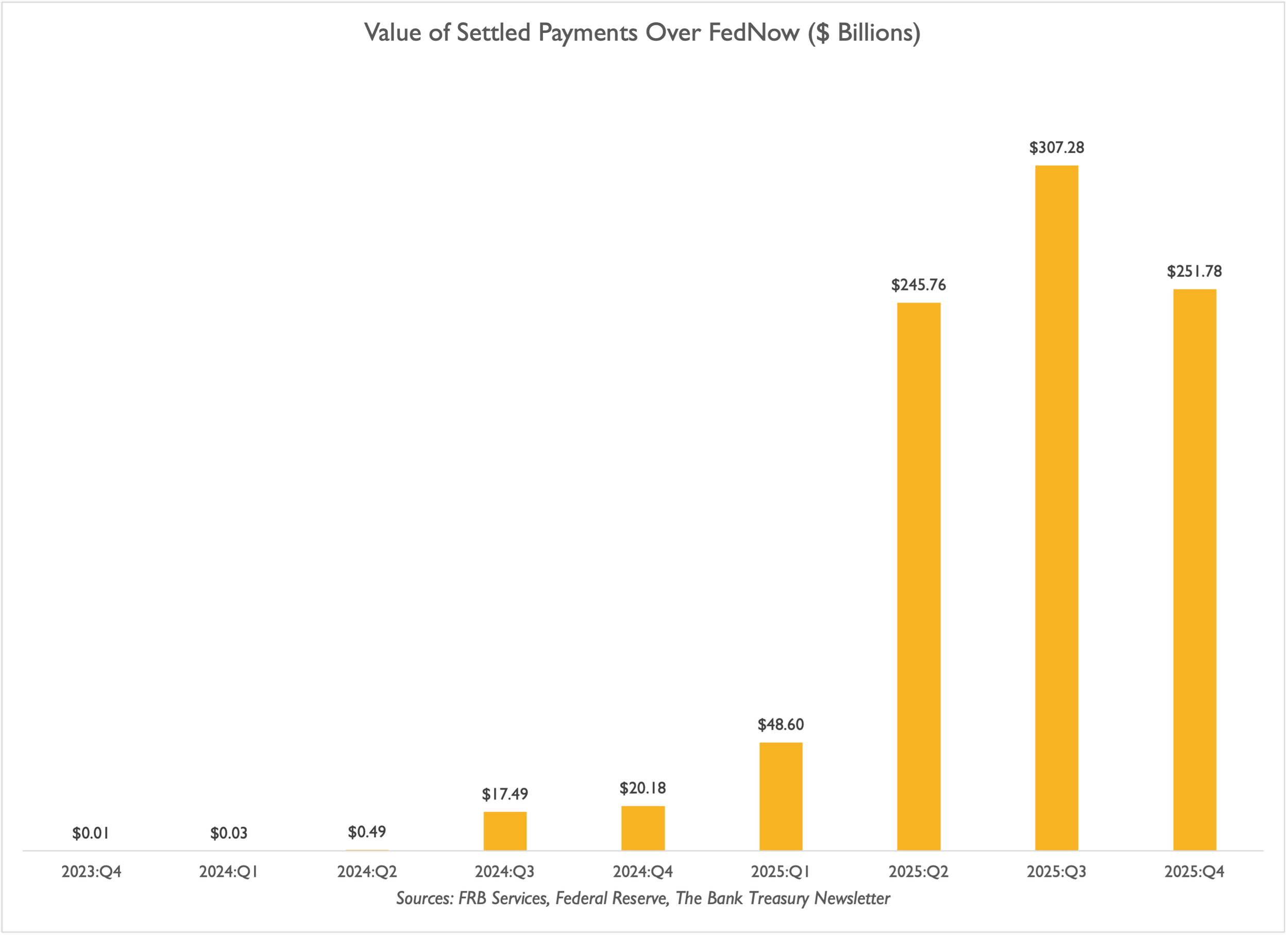

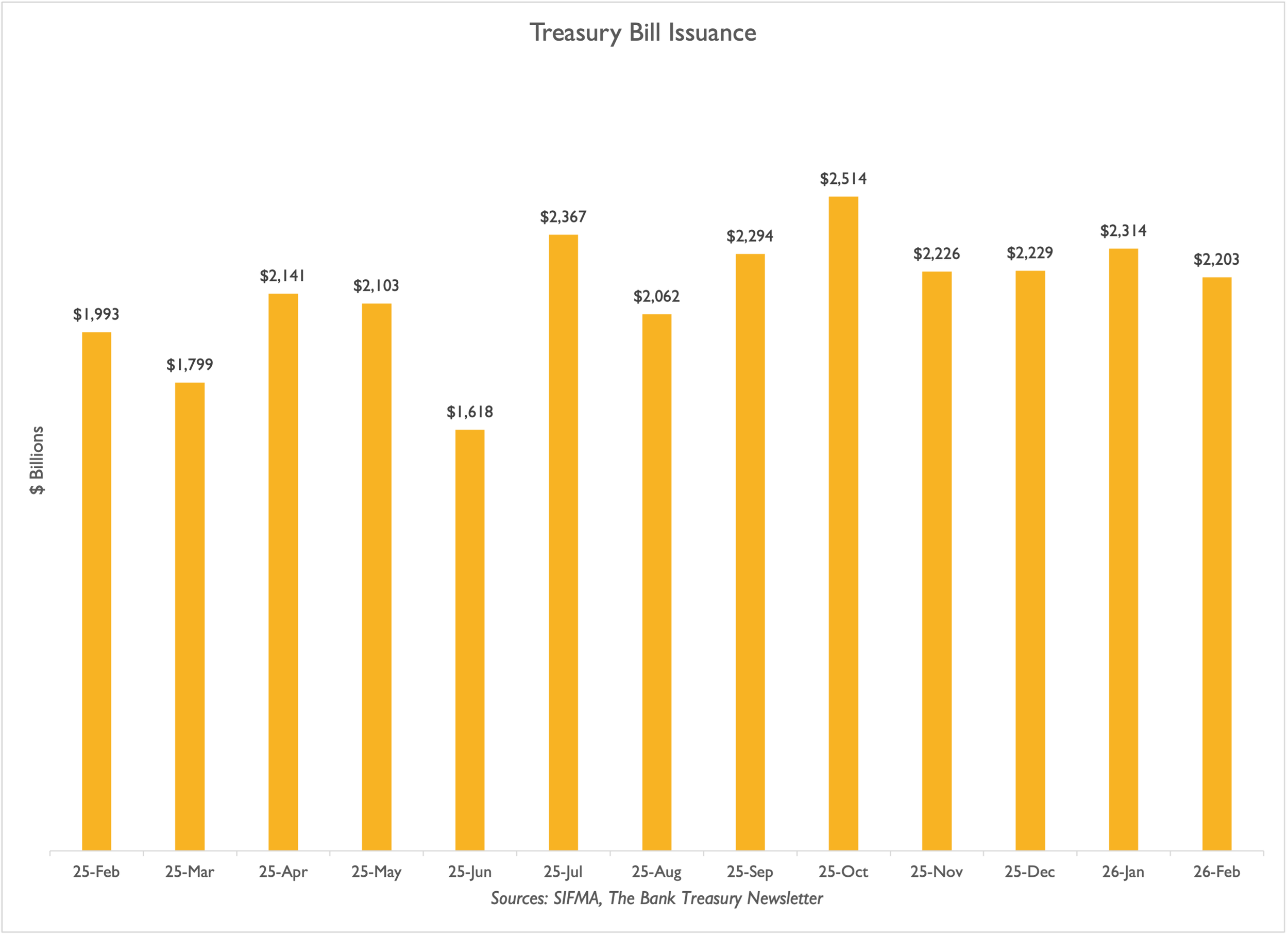

Instant payments are transforming how bank treasurers manage deposits and liquidity. Slide 1 displays a significant rise in FedNow activity over the past two years, which only stabilized last quarter. Despite this, FedNow accounts for only a small share of payments processed through FedWire, which reached $171 trillion last quarter (Slide 2). Meanwhile, the average monthly issuance of Treasury Bills in the past year (Slide 3) exceeded $2 trillion.

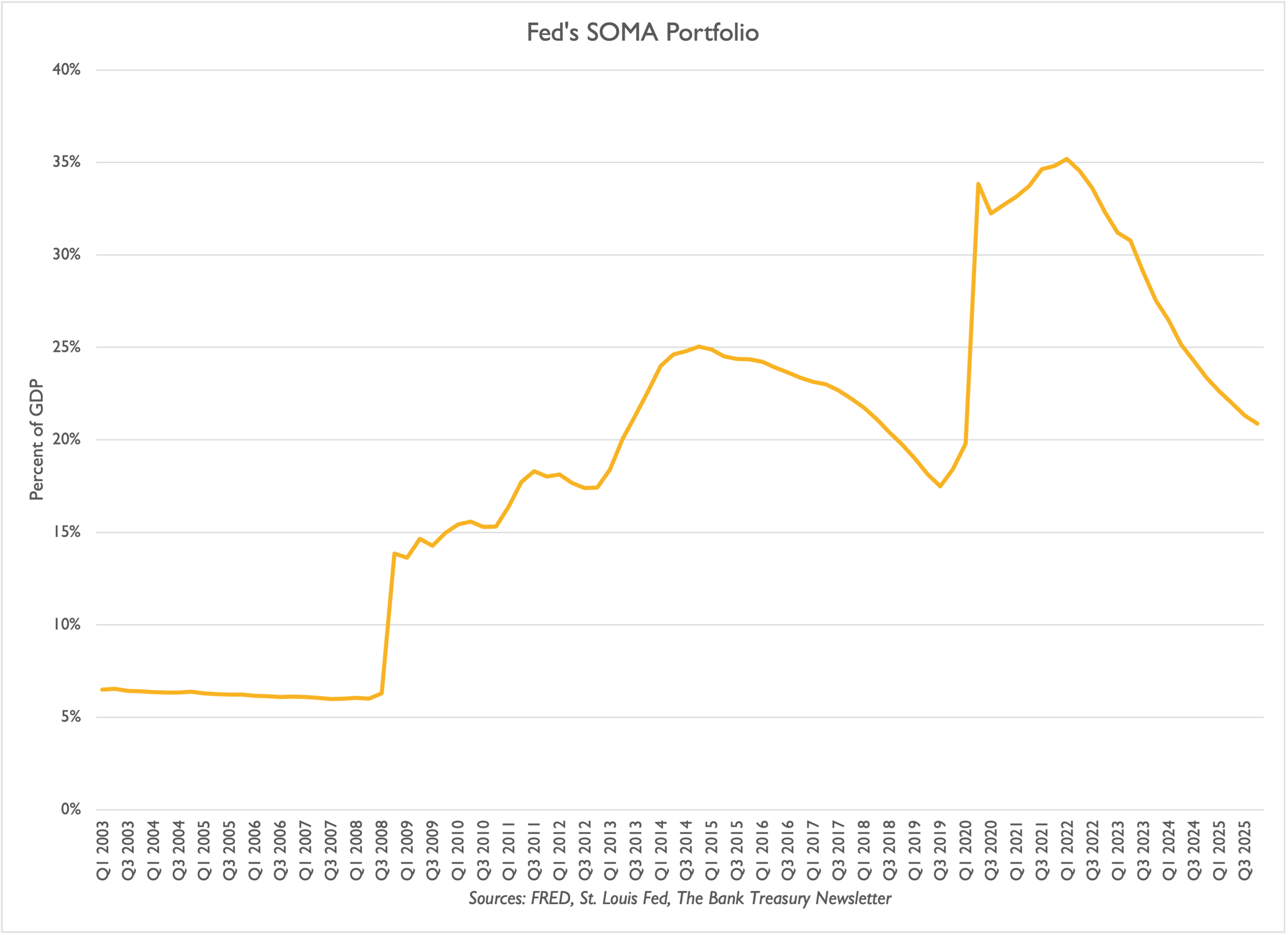

Kevin Warsh, President Trump’s candidate to succeed Jay Powell as Fed Chair when his term concludes this May, advocates for a smaller Fed balance sheet. However, as shown in Slide 4, the Fed’s System Open Market Account (SOMA) has already decreased to 21% of Gross Domestic Product (GDP), approaching its level before COVID and Quantitative Easing 2, which expanded it to a peak of 35% of GDP in 2022.

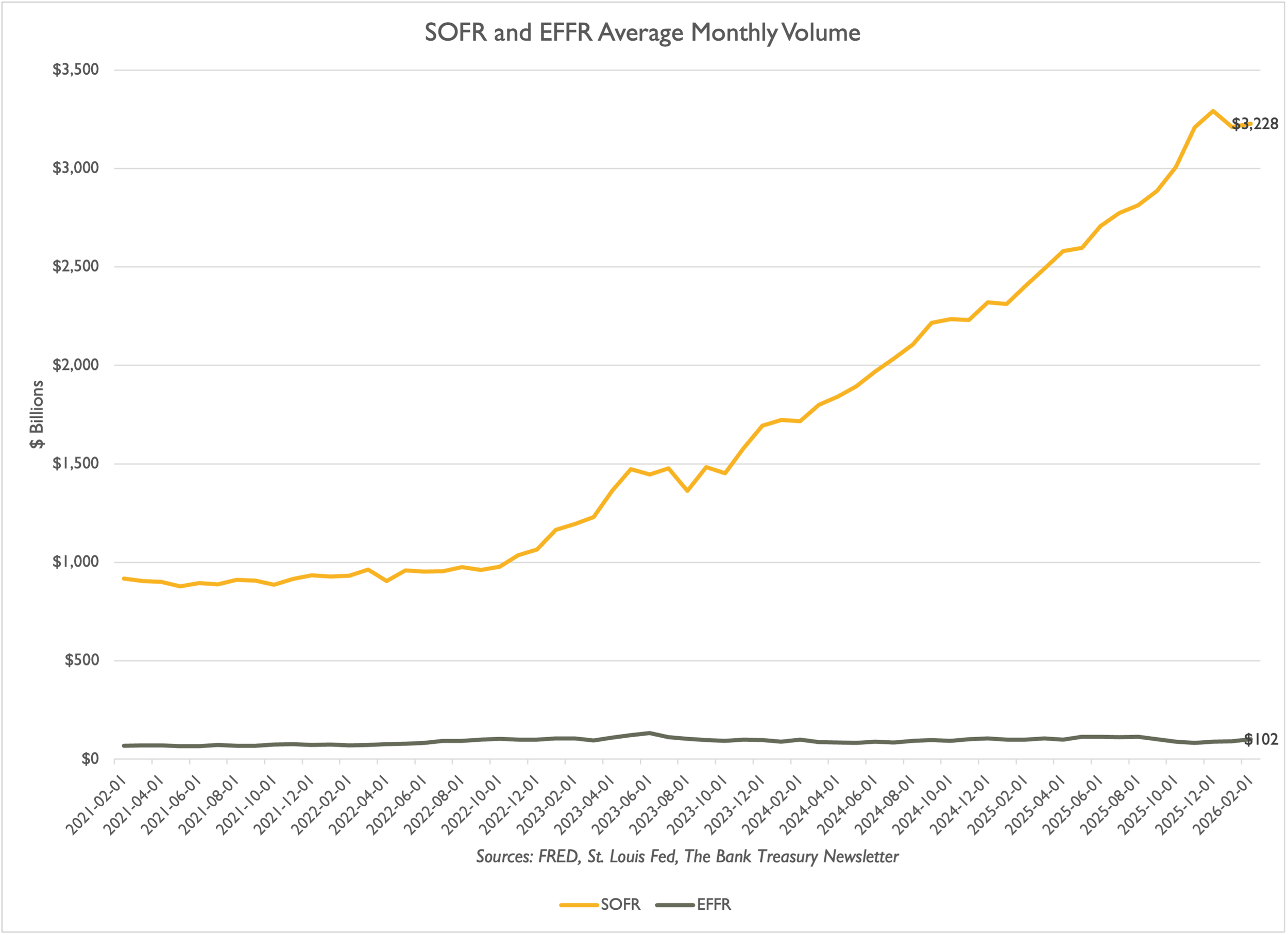

As mentioned in this month’s newsletter, the gap between the Effective Fed Funds Rate (EFFR) and the Secured Overnight Financing Rate (SOFR) remains slightly inverted. Although SOFR is a risk-free rate and EFFR reflects unsecured interbank credit risk, Slide 5 shows one of SOFR’s key benefits as a benchmark lending rate: its trading volumes are significantly higher than EFFR and have tripled since the administrators discontinued LIBOR at the end of 2021.

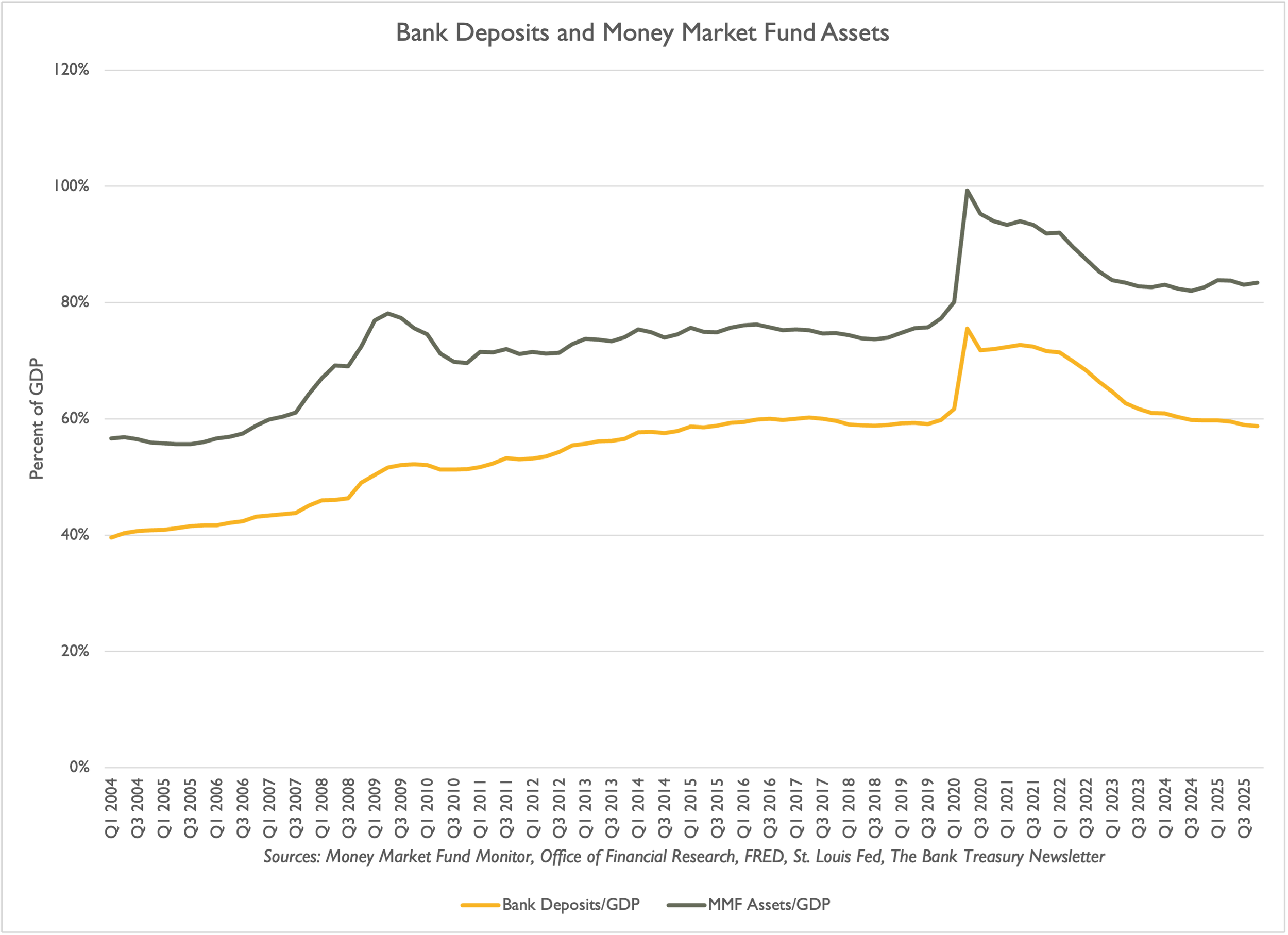

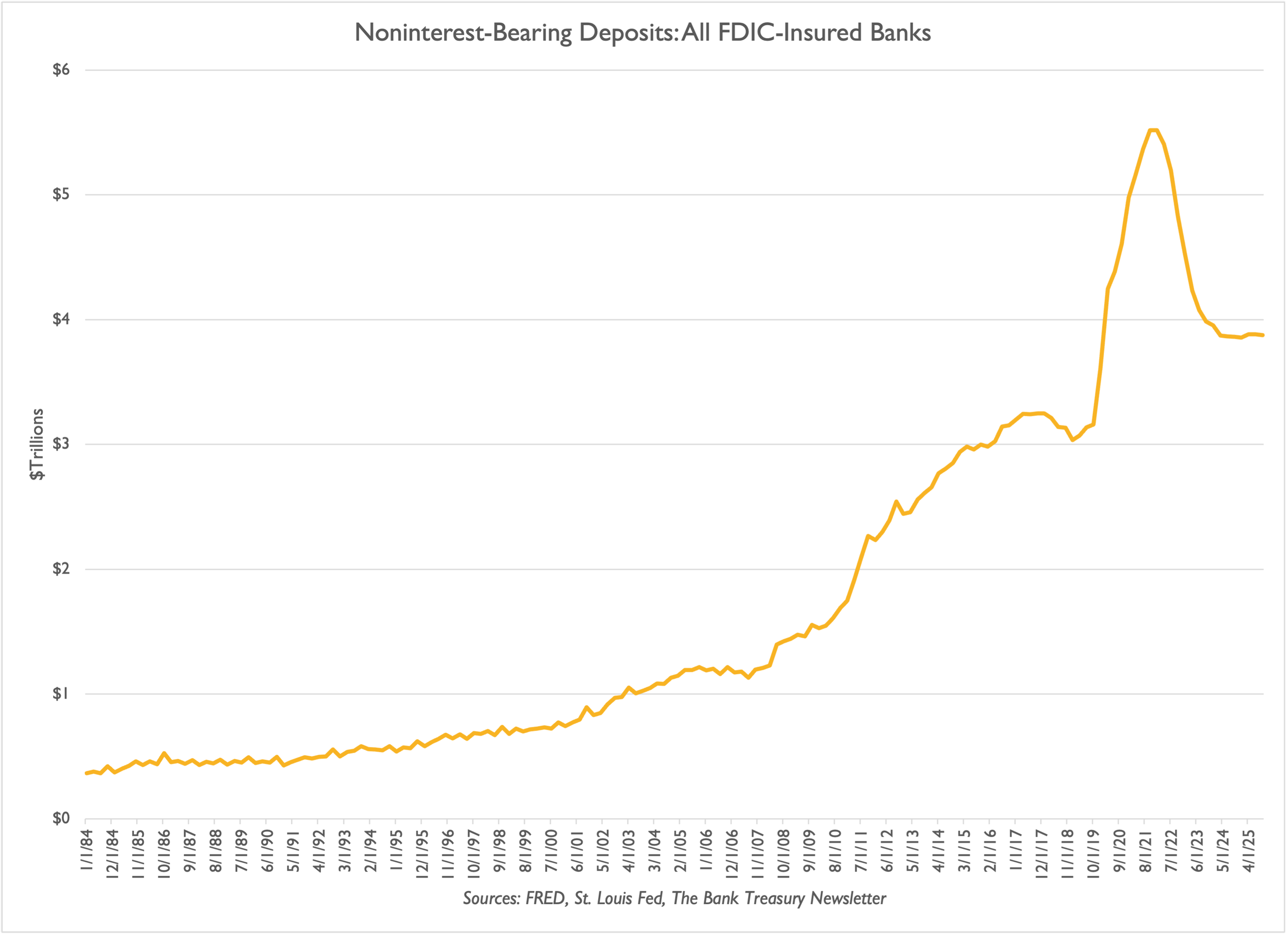

This year, domestic bank deposits hit a record high of over $17 trillion. While money market funds (MMFs) reached only $8 trillion, their growth has accelerated. Slide 6 shows their balances relative to GDP, which together account for more than 80%. Moreover, falling short-term interest rates over the past year have supported the stability of noninterest-bearing deposits, which were just under $4 trillion last quarter (Slide 7).

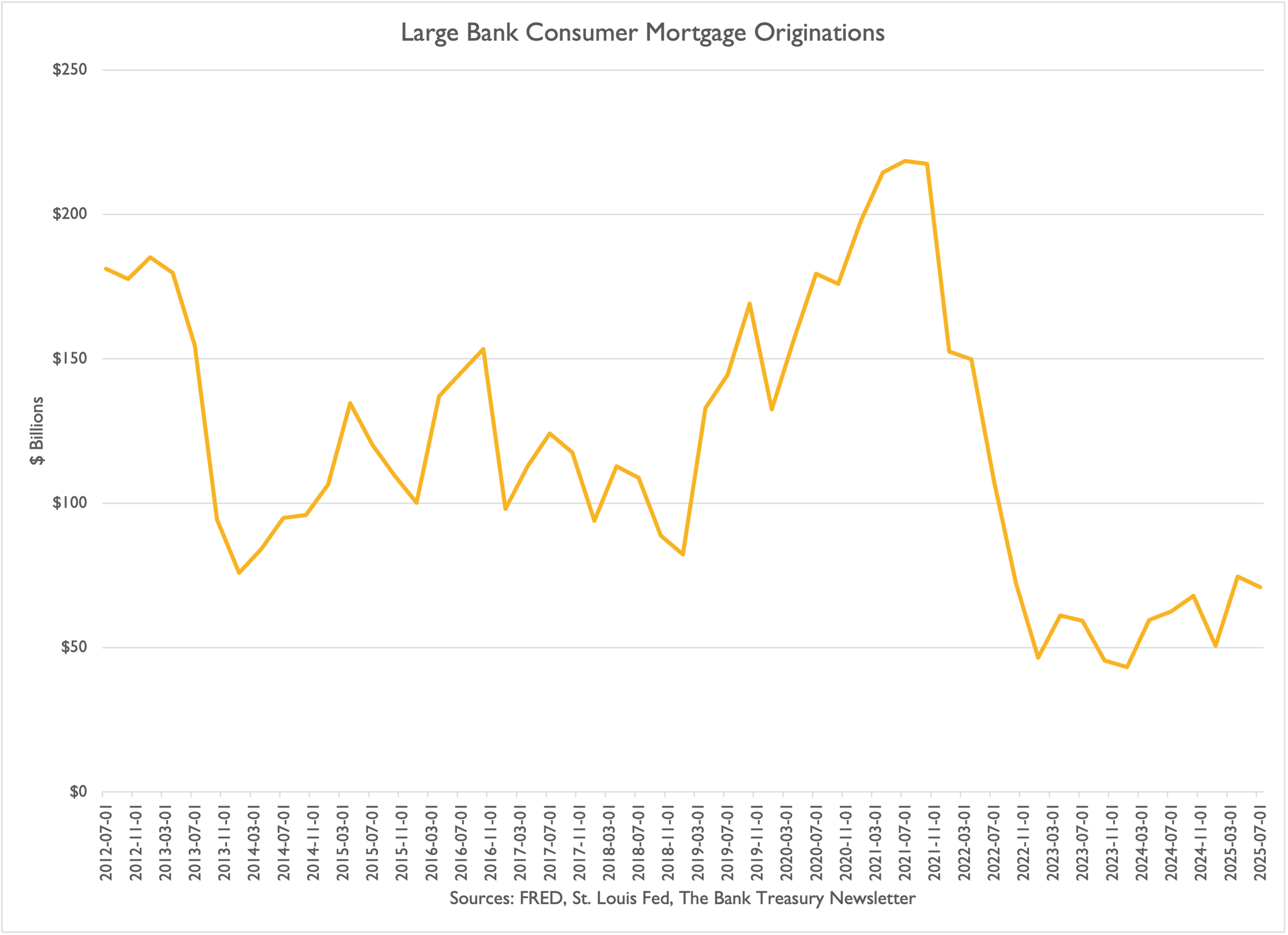

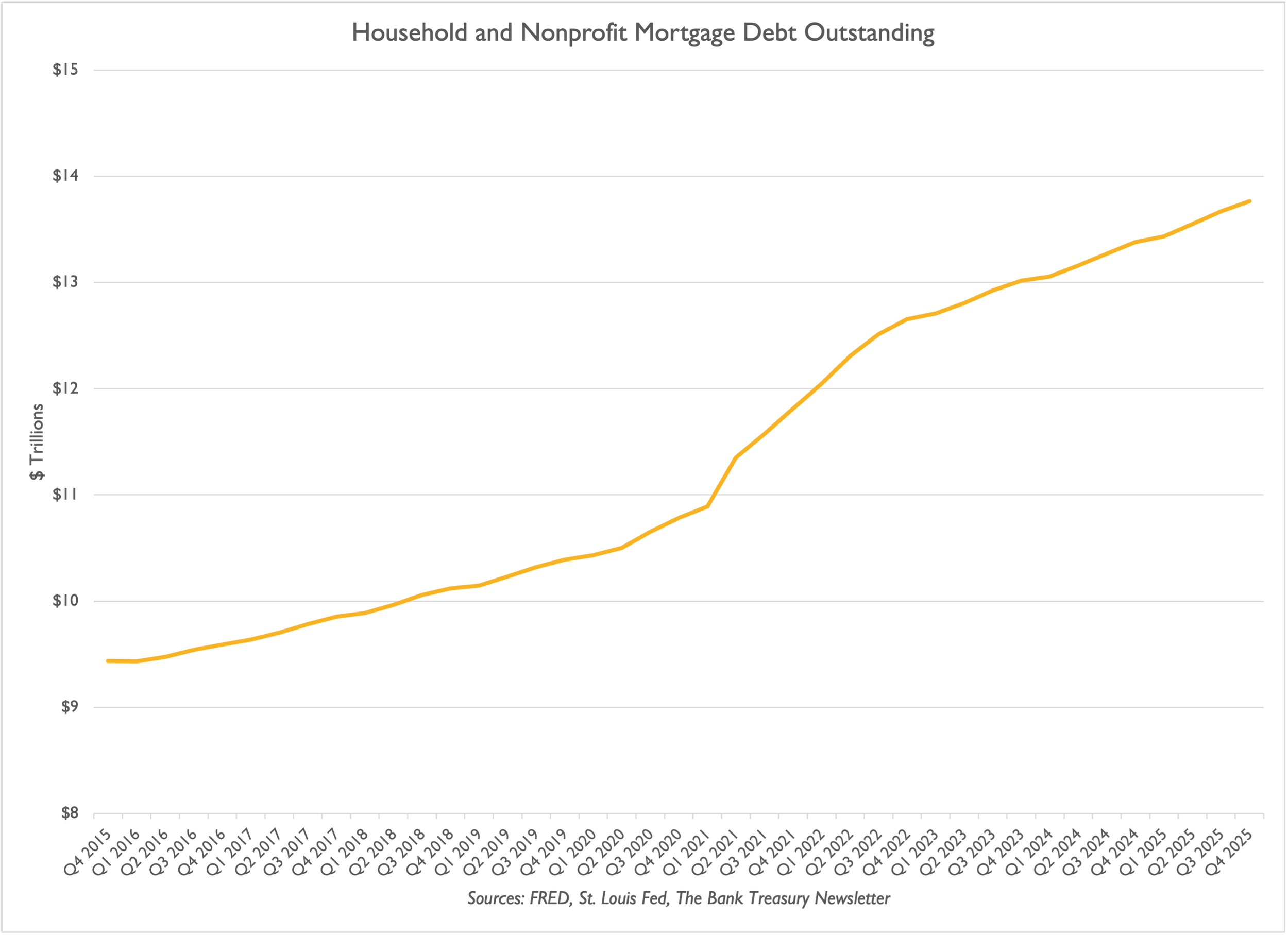

However, lower rates did not significantly help the banking sector regain its home mortgage business, with origination volumes at major banks remaining near a two-decade low (Slide 8). Meanwhile, nonbank lenders are doing better and are the main reason home mortgage debt outstanding approached $14 trillion last quarter (Slide 9).

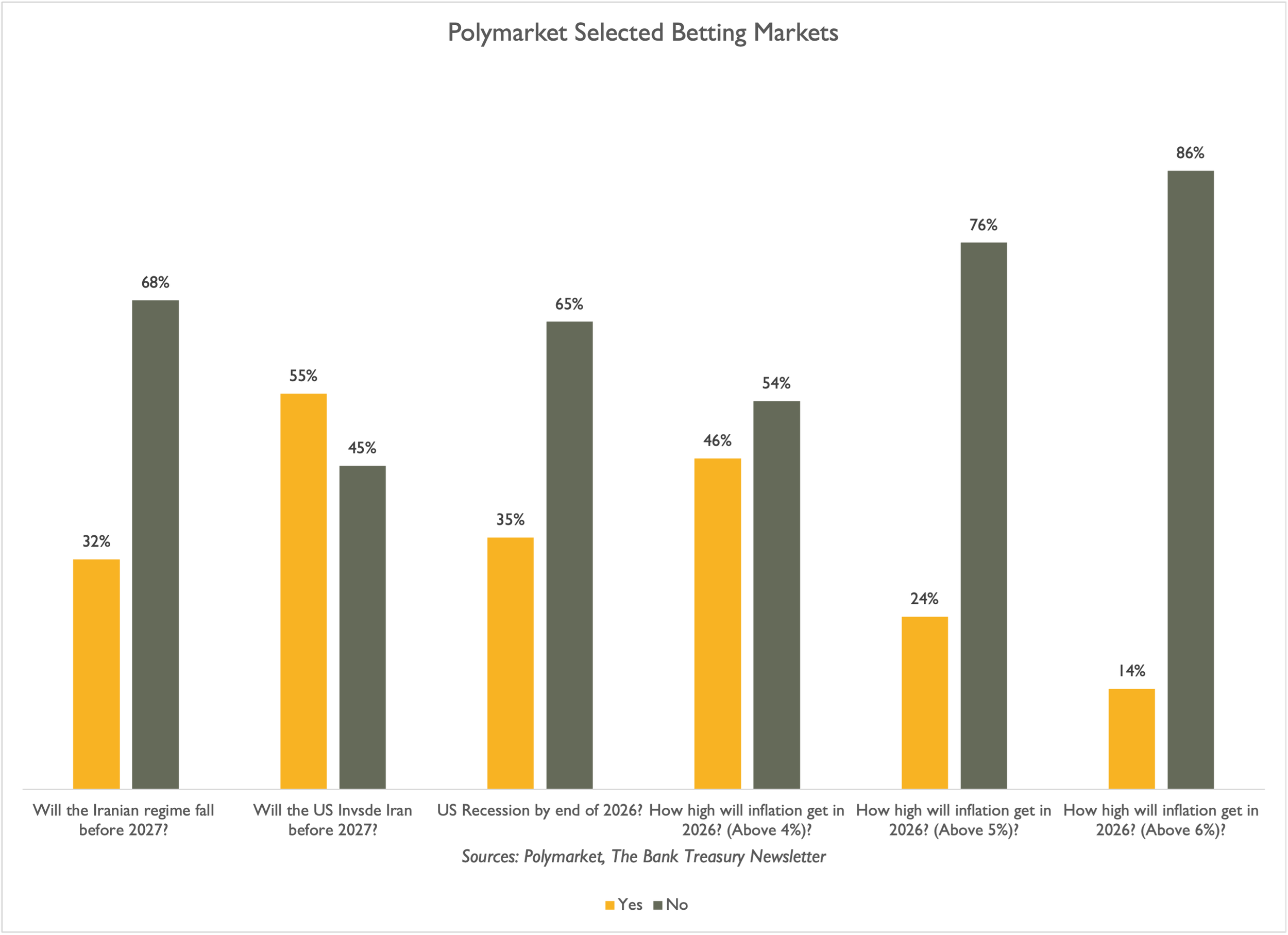

The outcome of the Iran conflict remains highly uncertain, causing significant volatility in financial markets. Polymarket, a platform where the public can wager on current issues—including politics, geopolitics, economics, sports, and entertainment—offers insights into public expectations regarding key questions posed to bank treasurers (Slide 10). According to this platform, the public generally believes that: 1) the Iranian regime will likely remain in power even if the U.S. invades; 2) there probably will be no recession in 2026; and 3) inflation will likely surpass 4% this year.

FedNow Payment Volumes Have Stabilized

FedWire Volumes Edged Higher Last Year

T-Bills Account For 83% of Treasury Issuance

Fed’s SOMA Portfolio Shrinking Relative To GDP

SOFR Volumes Tripled Since LIBOR’s Retirement

MMFs Have Outgrown Deposits Since 2023

Noninterest Deposit Balances Stabilized Last Year

Banks Struggle With Home Mortgage Originations

Non-Banks Driving Home Mortgages

Leading Market Unknowns